Compliments of

Alan Van Zee

Alan Van Zee

President | NMLS #: 297154

Hawaii Mortgage Company, Inc.

Company NMLS #: 232582

Alan Van Zee is one of the top producing Mortgage Originators in the state, originating over $2,000,000,000 to date. He has written and published this weekly newsletter for the past 18 years. It is the most widely read mortgage, real estate, and finance publication in Hawaii.

Hawaii Mortgage Company, now in our 26th year of providing mortgages to the people of Hawaii, is proud to have a complaint-free history. We make sure our clients are happy!

News and Insight

For the Weekend of March 7th, 2026

Hawaii’s Most Read Mortgage, Real Estate, and Finance Publication for 18 Years

Volume 18 – Issue 24

A Foolish Tradeoff?

If you’ve read this newsletter for any amount of time, you’ll know that I have always advocated homeownership as being the greatest way to build wealth for most people. It is with that in mind that I wonder if it is wise for those wishing to get ahead in life to enter into an agreement that will limit the gains they could make in the future to get a deal today.

For real estate, it is true that in most cases, one can rent a comparable home in Hawaii for less than the carrying costs of ownership. So why buy? Because over time, renting gets you nothing. Ownership, on the other hand, provides for an increase in the home’s value - providing a gain in equity. That gain in equity is how more people get ahead financially – more than the stock market by far.

Here’s the simple reason why – it’s called leverage. If one were to buy a home for $500,000 and put 10% down, their capital investment is $50,000. If that home were to appreciate 3% per year, that 3% figure is based on the value of the home, and not your down payment. A 3% gain on that home would result in a gain in appreciation of $15,000 annually. What other way is there for someone to take $50,000 and make $15,000 per year? That’s a 30% return on the initial investment.

It is with this in mind that I am concerned that too many people aren’t aware of the powerful wealth building, buying a home presents. To combat high home prices that prohibit so many local families from buying, the new (actually no so new) trend is to provide lower priced homes in exchange for limiting your gain when you want to sell.

Every new project you hear advertised has a certain number of “affordable” units available. The developers, in exchange for offering some affordable units, get special treatment from the government to make the entire project possible. From the government’s perspective, they are doing a good deed. They are forcing developers to offer units at lower prices, that would otherwise be unattainable for most families.

But the tradeoff for most affordable units being built today are deed restrictions that limit your ability to gain wealth when you sell. These deed restrictions often last 10, 12, or 15 years depending on income level, though some new proposals aim for perpetual restrictions. Projects on county-owned land may have 99-year restrictions.

The restrictions vary, but during the restriction years if the unit is sold, the government may reserve the right to set the maximum sale price. There may also be a clause where the government has first-right to purchase the unit back at your original purchase price. With many of the Kakaako affordable condos, owners are capped at gains of 1% per year.

With these types of restrictions, the ability for residents to lift themselves financially is prohibited. It then begs the question; Why buy in the first place?

They say the road to hell is paved with good intentions. While a low-cost affordable home today may seem like a great opportunity, no one is educating the public if in the long run it is a good deal for their circumstances. Do you forego wealth creation in exchange for a roof over your head? That’s a question only you can answer.

And now the week’s economic news…….

Oil Prices Surge

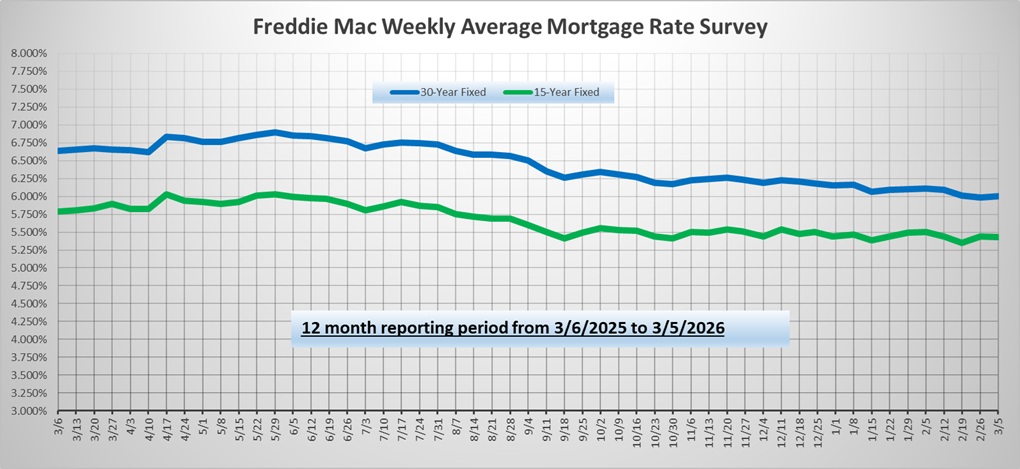

The conflict with Iran outweighed the major economic data this week. Surging oil prices raised the outlook for future inflation, so mortgage rates ended the week higher.

Geopolitical events such as the conflict with Iran affect mortgage rates in multiple ways. The most common reaction is that investors shift assets from risky assets such as stocks to relatively safer assets such as bonds, which is positive for mortgage rates. However, oil prices have risen sharply this week due to the conflict. This increases future inflationary pressures, which is negative. In addition, military spending may increase, and the government may need to issue more bonds to fund the deficit. An increase in supply would cause yields to rise.

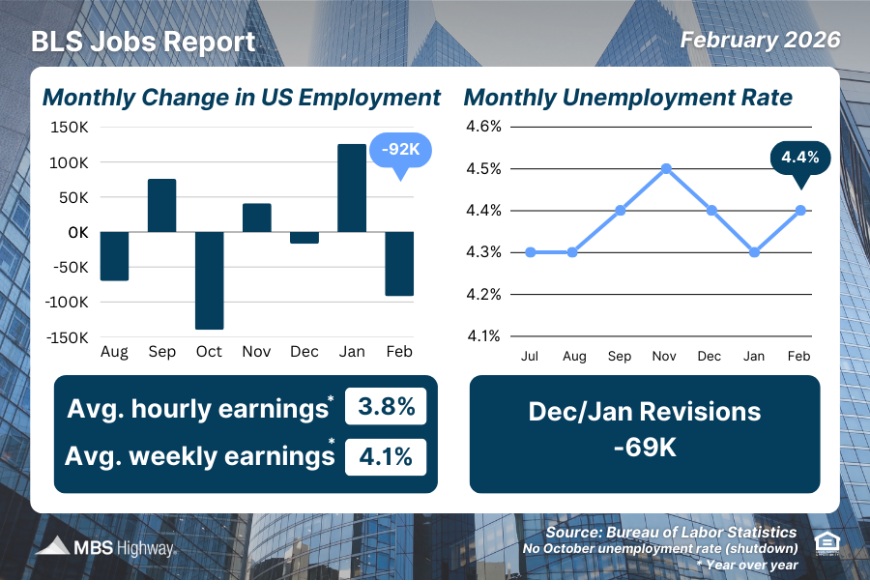

The key Employment report revealed that the economy lost 92,000 jobs in February, far below the consensus forecast for a gain of 50,000. A large strike at a big health care company and severe winter weather contributed to the weakness. The unemployment rate unexpectedly rose from 4.3% to 4.4%. Average hourly earnings, an indicator of wage growth, were 3.8% higher than a year ago, up from an annual rate of 3.7% last month.

The key Employment report revealed that the economy lost 92,000 jobs in February, far below the consensus forecast for a gain of 50,000. A large strike at a big health care company and severe winter weather contributed to the weakness. The unemployment rate unexpectedly rose from 4.3% to 4.4%. Average hourly earnings, an indicator of wage growth, were 3.8% higher than a year ago, up from an annual rate of 3.7% last month.

In contrast to the labor market data, two significant economic reports released this week from the Institute of Supply Management revealed stronger than expected results. The ISM national services sector index jumped to 56.1, far above the consensus forecast of 53.5 and the highest level since July 2022. The ISM national manufacturing sector index was 52.4, above the consensus forecast of 52.0. Readings above 50 indicate an expansion in the sectors and below 50 a contraction. While tariff policies may change after the recent Supreme Court decision, the higher tariffs on foreign goods imposed last look to be providing a lift to domestic manufacturing companies and helping them close the performance gap with services.

Consumer spending accounts for over two-thirds of U.S. economic activity, so the monthly Retail Sales report is a key measure of the health of the economy. Delayed by the government shutdown, the most recent data revealed that retail sales in January fell 0.3% from December, which was close to expectations.

Next Week

Looking ahead, attention will remain fixed on the conflict with Iran. Investors also will monitor comments from government officials about tariffs and from Fed officials for hints about future monetary policy. For economic data, two big inflation reports will be released in the same week due to disruptions from the government shutdown. The Consumer Price Index (CPI), a widely followed monthly inflation indicator that looks at the price changes for a broad range of goods and services, will come out on Wednesday. The PCE price index, the inflation indicator favored by the Fed, will be released on Friday. In addition, Existing Home Sales will come out on Tuesday.

Until next week….

*** Please note that Freddie Mac publishes their weekly rate report on Wednesday mornings from data received Monday and Tuesday.

The graph above is intended to shown rate trends, and not “today’s current rate”. ***

Reviews From Our Past Clients

With every client, we promise to provide you with a comprehensive analysis of your mortgage needs, the best service possible, and the best rates we can find. We make it our mission to have every transaction close with our clients happy with the service we provided. Browse through the hundreds of reviews we’ve received from our clients posted on both Google and Zillow.com, and read what they thought of their experience using Hawaii Mortgage Company.

Google Link:

Hawaii Mortgage Company Review on Google.com

Zillow.com Link:

Hawaii Mortgage Company Reviews on Zillow.com

Our Rate Quote System is Available to You

Our automated rate quoting system is live. Now you can check rates and try different scenarios 24-hours a day. Remember, it’s just a computer. For non-standard rate quotes, such as construction, vacant land, and other specialty programs, you’ll still need to give a call.

Here’s the link: https://www.hawaiimortgage.net/todays-rates/

Do you think all lenders are the same?

There is a difference when you use Hawaii Mortgage Company for your financing. Here’s a short video telling you why:

Broker vs. Banker?

Click the link below to get a quick lesson on why working with a Mortgage Broker will benefit you on your next transaction.