Compliments of

Alan Van Zee

Alan Van Zee

President | NMLS #: 297154

Hawaii Mortgage Company, Inc.

Company NMLS #: 232582

Alan Van Zee is one of the top producing Mortgage Originators in the state, originating over $2,000,000,000 to date. He has written and published this weekly newsletter for the past 18 years. It is the most widely read mortgage, real estate, and finance publication in Hawaii.

Hawaii Mortgage Company, now in our 26th year of providing mortgages to the people of Hawaii, is proud to have a complaint-free history. We make sure our clients are happy!

News and Insight

For the Weekend of March 14th, 2026

Hawaii’s Most Read Mortgage, Real Estate, and Finance Publication for 18 Years

Volume 18 – Issue 25

Forever Renter by a Thousand Cuts

For the past several months I’ve brought to light the inability of government to generate affordable homes for the residents of our state. This has resulted in either people leaving Hawaii or settling on being forever renters. But is it all the fault of government? Today we’re going to examine how millennials and Gen-Z are sabotaging their ability to buy a home.

According to the experts, I should be a Baby-Boomer kid. But being born at the very end of that cycle, I feel I’m more of a Gen-X kid. I bring this up because the way “people of my age” grew up is very different than millennials and Gen-Z. If you’re in your 40’s or younger, use today’s newsletter as a wakeup call, versus being talked down to.

You “youngsters” grew up in the age of technology. That age of technology has altered our traditional economy into an economy of convenience. This modern economy has quietly altered the way people spend money - not because of one major purchase, but through hundreds of small conveniences that encourage people to spend in ways previous generations never could. Each purchase may seem minor on its own, but it’s the cumulative effect that has changed everything.

30 years ago, a typical household had very few recurring monthly expenses. You had rent or a mortgage, your utilities, and maybe a car payment. That was about it.

Let’s contrast that to what the typical millennial or Gen-Z spends each month in today’s world. Streaming services, music subscriptions, app memberships, cloud storage plans, premium phone services, grocery delivery, ride sharing, and food delivery platforms. If you start adding up all these little conveniences, you’ll see quickly how much money is going out the door without realizing the impact on your finances. None of these services on their own are large expenditures. Most cost $10-$15 per month. That’s precisely why they are so easy to dismiss.

A 2024 survey from C+R Research found that the average American spends about $273 per month on subscription services alone. Many people underestimate the total because the payments are spread across multiple apps, cards, and billing dates. What feels like a handful of harmless charges can quietly become thousands of dollars over the course of a year.

Our culture has changed dramatically when it comes to food spending. The BLS reported in 2024 that we now spend more money eating out each year than we spend on food to be consumed at home. As a kid, we rarely went out to eat. It was always a special occasion. Today in my house, we get take-out a couple of nights a week – just to give ourselves a break from cooking. But the younger generations eat out at a far greater rate. The proliferation of food delivery platforms has altered the American lifestyle. A dinner that once required driving across town, parking the car, and waiting in line will now show up at your door after a few taps on a phone. Removing effort from spending tends to increase how often people spend. If a purchase requires time and inconvenience, it happens occasionally. If it requires almost no effort at all, it becomes part of the weekly routine.

All I have to do is mention your $6-$8 daily Starbucks coffee, and you know already that’s a silly waste of money. I am shocked by the prices of a local plate lunch these days, and how so many in the trades are spending $20 per day just on lunch alone.

If you were to get serious about owning a home, here are the steps you need to take now – not when you think you’ll want to in a couple of years.

- Collect all your credit card and bank statements for 2 months.

- Analyze them for every payment made for streaming, music, apps, games, etc.

- Cancel them all. There are free versions of everything you’re spending money on.

- Buy an insulated thermos and make coffee at home.

- Take home lunch instead of buying.

- It’s okay to reward yourself once every 2 weeks.

Determine how much you spent for food and drink outside the home each month. Divide that number by 2, as taking food from home will still cost you about 50% of what you were paying to eat out. Add that number to your monthly expenses for the lifestyle items. Your result should be at least $400 per month. Take that combined amount and multiply by 60. If you did your math right, you’ll have $24,000. For a couple, that’s $48,000.

$48,000 is equal to a 5% down payment on a $960,000 home. 10% on a $480,000 condo.

If you think 5 years is too long to sacrifice without seeing any results and wish you could save even faster, how about getting a cheap reliable car if you need one for work or use public transportation versus the $1,000 per month lifted Tacoma payment you have? That $1,000 per month will add $12,000 per year to your down payment fund. Already have a family and are leasing a Tesla for another $600 per month? Try and get by with one family car to save that payment each month.

If you got really serious, the wait wouldn’t be so long.

$400 per person ($800), plus the truck payment ($1,000), plus the Tesla ($600) is $2,400 per month. In 20 months – less than 2 years, you’ll have your down payment.

For the moms and dads that read my weekly newsletter, pass this along to your kids that tell you every holiday dinner that it’s impossible to buy a home because they just don’t have anything for a down payment.

For you millennials and Gen-Z’s, please take this to heart. All the premium plus apps in the world won’t get you into a home and start building equity. YOU need to prioritize what’s important to YOU. Don’t be a forever renter.

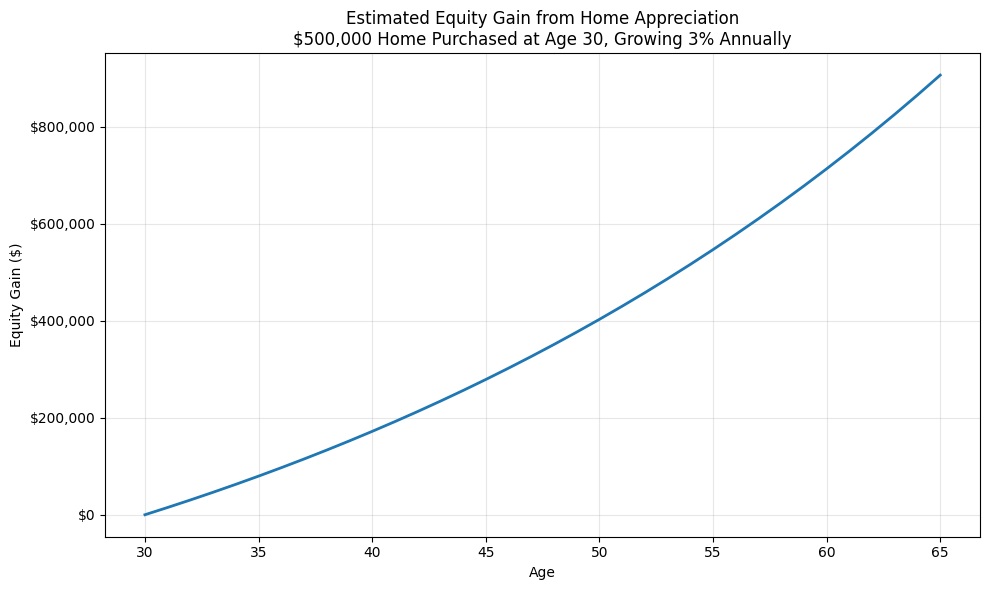

The younger you are when owning your first home, the more years you’ll have for appreciation. Remember, appreciation is based on the entire price of your home – no matter how little you put down. If you were 30 years old when you purchased your first home, and that home cost $500,000 – how much equity would you gain over your lifetime if we used an average of 3% gain per year?

Hopefully you can now understand why renting is the wrong path in life. Buckle down and do what you can to save for that down payment. It will be the best investment into yourself you’ll ever make.

And now the week’s economic news…….

Focus on Oil Prices

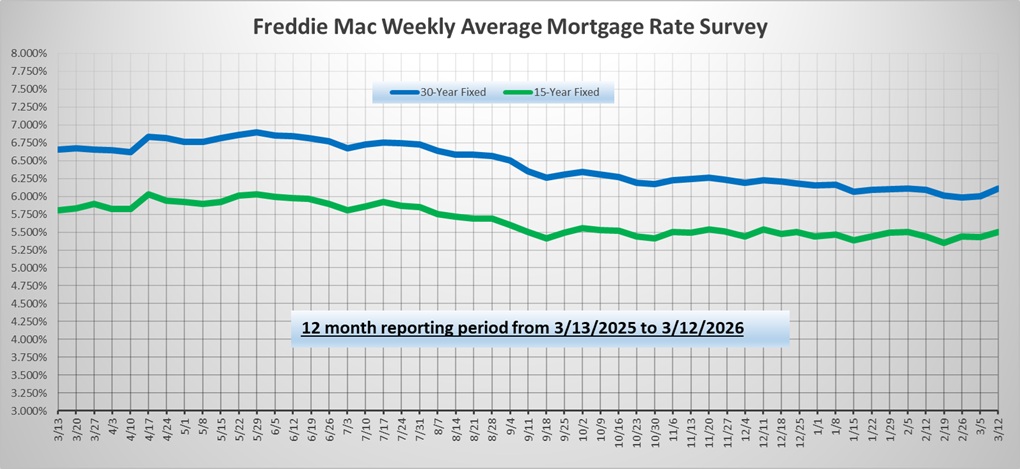

Most of the movement in mortgage rates this week was due to changes in oil prices, which continued to climb. Two major inflation reports matched expectations and caused little reaction. As a result, mortgage rates ended the week higher.

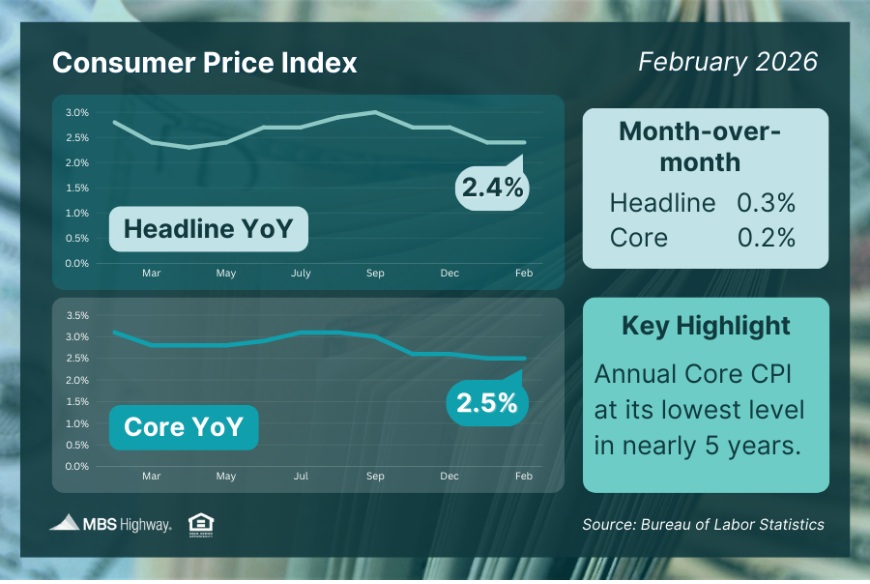

The Consumer Price Index (CPI) is one of the most closely watched inflation indicators released each month. To reduce short-term volatility and get a better sense of the underlying inflation trend, investors look at core CPI, which excludes food and energy. In February, Core CPI was 2.5% higher than a year ago, matching expectations and remaining at the lowest level since 2021.

The Consumer Price Index (CPI) is one of the most closely watched inflation indicators released each month. To reduce short-term volatility and get a better sense of the underlying inflation trend, investors look at core CPI, which excludes food and energy. In February, Core CPI was 2.5% higher than a year ago, matching expectations and remaining at the lowest level since 2021.

Shelter (housing) costs were up 3.0% on an annual basis and continue to be a primary reason why progress in bringing down inflation remains challenging, but this reading has been trending lower in recent months. Within this component, rent rose just 0.1% from January, the smallest monthly increase since January 2021.

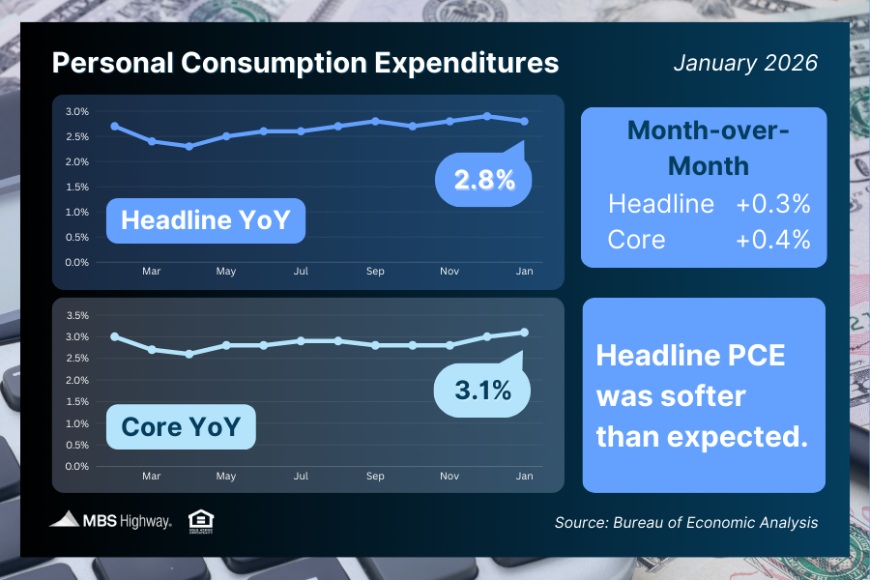

Fed officials keep a close eye on inflation, and the PCE price index is their favored indicator. One of the significant differences with CPI is that PCE places more weight on health care costs and less on shelter. Delayed by the government shutdown, the latest report revealed that Core PCE in January was 3.1% higher than a year ago, up from an annual rate of increase of 3.0% in December and matching the consensus forecast. This was the highest reading since March 2024. Progress toward the 2.0% target of the Fed has not been easy, and this desired level has not been achieved since February 2021.

Fed officials keep a close eye on inflation, and the PCE price index is their favored indicator. One of the significant differences with CPI is that PCE places more weight on health care costs and less on shelter. Delayed by the government shutdown, the latest report revealed that Core PCE in January was 3.1% higher than a year ago, up from an annual rate of increase of 3.0% in December and matching the consensus forecast. This was the highest reading since March 2024. Progress toward the 2.0% target of the Fed has not been easy, and this desired level has not been achieved since February 2021.

In February, sales of existing homes rose 2% from January, exceeding expectations, but still were down slightly from a year ago. The median price of $398,000 was up just a slim 0.3% from last year at this time. Inventories remain at a 3.8-month supply nationally. However, inventories were 5% higher than a year ago.

Next Week

Looking ahead, attention will remain fixed on the conflict with Iran. Investors also will monitor comments from government officials about tariffs. The next Fed meeting will take place on Wednesday, and no change in the federal funds rate is expected. Investors will be looking for guidance about the impact of higher oil prices on future monetary policy. For economic data, the Producer Price Index (PPI), a monthly inflation indicator, will be released on Wednesday.

Until next week….

*** Please note that Freddie Mac publishes their weekly rate report on Wednesday mornings from data received Monday and Tuesday.

The graph above is intended to shown rate trends, and not “today’s current rate”. ***

Reviews From Our Past Clients

With every client, we promise to provide you with a comprehensive analysis of your mortgage needs, the best service possible, and the best rates we can find. We make it our mission to have every transaction close with our clients happy with the service we provided. Browse through the hundreds of reviews we’ve received from our clients posted on both Google and Zillow.com, and read what they thought of their experience using Hawaii Mortgage Company.

Google Link:

Hawaii Mortgage Company Review on Google.com

Zillow.com Link:

Hawaii Mortgage Company Reviews on Zillow.com

Our Rate Quote System is Available to You

Our automated rate quoting system is live. Now you can check rates and try different scenarios 24-hours a day. Remember, it’s just a computer. For non-standard rate quotes, such as construction, vacant land, and other specialty programs, you’ll still need to give a call.

Here’s the link: https://www.hawaiimortgage.net/todays-rates/

Do you think all lenders are the same?

There is a difference when you use Hawaii Mortgage Company for your financing. Here’s a short video telling you why:

Broker vs. Banker?

Click the link below to get a quick lesson on why working with a Mortgage Broker will benefit you on your next transaction.