Compliments of

Alan Van Zee

Alan Van Zee

President | NMLS #: 297154

Hawaii Mortgage Company, Inc.

Company NMLS #: 232582

Alan Van Zee is one of the top producing Mortgage Originators in the state, originating over $2,000,000,000 to date. He has written and published this weekly newsletter for the past 17 years. It is the most widely read mortgage publication in Hawaii.

Hawaii Mortgage Company, now in our 25th year of providing mortgages to the people of Hawaii, is proud to have a complaint-free history. We make sure our clients are happy!

Mortgage Market News and Insight

For the Weekend of March 29th, 2025

Hawaii’s Most Read Mortgage Publication for 17 Years

Volume 17 – Issue 28

The System No Longer Serves Us

My goal today is to take three unrelated stories and tie them together to show how government, left unchecked, can spiral out of control. While initial intentions were noble, the system has grown to no longer benefit the public it was once intended to help.

What is the CFPB?

The Consumer Financial Protection Bureau (CFPB) was established in the wake of the Great Recession of 2008 to protect consumers against unscrupulous lending practices. Despite the government already having multiple agencies regulating what we in the financial world do, the 2010 Dodd-Frank Financial Reform Act created the CFPB as an added layer of consumer protection. While the CFPB has instituted some good reforms, many of the actions taken by this agency have been overbearing and created barriers to lending when none existed before.

Case #1: Affluent Struggle When Applying for Mortgages

I have been fortunate to have had some very wealthy clients. You may wonder why rich people need mortgages, but that isn’t the point. And while we all wish everyone was treated the same, when dealing with risk, the reality is that rich people are far less risky to lend to than those struggling to get by. Lenders go through lots of rules and regulations to lend money. But in the end, it all comes down to risk. That makes sense. But what if the government mandated how a lender evaluates risk?

One of the first regulations the CFPB implemented was the concept of “Ability to Repay”. On the surface the reasoning seems sound – prove you can pay back what you borrow, or you don’t get the loan. But is that really the best method of evaluating risk?

Why are rich people having issues when applying for a mortgage? Because the system we are required to use mandates all applicants to “prove” they can pay back what they borrow. Rich people may not show a lot of income due to tax loopholes or complex investment streams. Their income is generally more complicated than looking at pay stubs and liabilities on a credit report.

Bob the Retiree

Bob came to me to refinance his north shore Oahu home. The home was easily worth $3-Million dollars. He had a mortgage balance of $300,000. He is 66 years old and has over $1-Million in the bank. Bob decided to hold off on taking his social security because he doesn’t need it. Bob doesn’t show very much income. Do you think refinancing his mortgage is a huge risk? The home is worth ten-times what he owes. He has four-times the mortgage balance sitting in the bank.

Under the current rules of lending, Bob has insufficient income and does not qualify for mortgage financing because he lacks the “ability to repay”.

James the Anesthesiologist

James worked at a hospital on the mainland for 30+ years, making over $500,000 per year. He retired in November. It didn’t take James long to realize he missed what he did for all those years. James got an opportunity last month to come to Hawaii and work as an independent contractor at a local hospital. He’s not an employee. Despite the hospital paying him $45,000 per month, it’s all considered self-employment income, and he hasn’t been self-employed for 2 years. He loves Hawaii and wants to buy a condo here. He found one for $800,000. His plan was to put down $500,000 and finance $300,000.

James has $3-Million in the bank and can pay cash for the condo. That’s not the point. James’ income can’t be used to qualify because he hasn’t been self-employed long enough. Just like Bob the retiree, James lacks the “ability to repay”.

Sidney the Land Baron

Over the years Sid has acquired several hundred rental units across the country. By far, he has the most complicated tax structure I have ever reviewed. His personal tax return alone is 367 pages! Rich people pay accountants $$$ in order help shelter income. Businesses that own other entities. Entities held in family trusts. Again, despite having millions in assets, Sid doesn’t show a lot of income. I have to hand it to his group of CPA’s.

Sid wants to buy a luxury vacation rental on the Big Island for $10-Million and get a mortgage for $2-Million. Do you think Sid is a high risk? Do you think that even if something catastrophic were to happen to him financially he’d jeopardize his $10-Million dollar home? Because of how Sid has structured his income, the CFPB has made it hard for a lender to say yes.

The “Ability to Repay” rule was initiated to thwart erroneous the idea that banks want to give out loans to those that can’t afford them, in an effort to somehow steal the property from them later. No lender ever wants to initiate a foreclosure action. It costs the lender time and money. If the property is sold for more than what’s owed, the bank doesn’t get to keep the extra. This rule that hinders good lending needs to go.

Case #2: The CFPB vs Townstone Mortgage

In one of the worst cases of government overreach, the CFPB went after a small Chicago-based mortgage broker over acts of discrimination. The CFPB acted without a single complaint and no proof of any discrimination was ever present.

Where there’s smoke, there’s fire, right? What did Townstone do? The CFPB had two theories to make their case for discrimination.

To CFPB, a disparity automatically equaled discrimination. CFPB targeted Townstone not based on any act of discriminatory conduct, but solely on perceived racial disparities in mortgage application and origination statistics. That disparity? An agency-defined “shortfall” of just 31 applications from “majority-minority” areas, out of 876 total applications in a three-year period.

CFPB used audio mining software to search Townstone’s radio show and podcasts finding that they engaged in political speech critical of the Bureau. They identified 16 minutes out of nearly 79 hours of radio content (.33%) that they deemed “disconcerting” and that “could be interpreted as inappropriate, incorrect, or insensitive.” What was so disconcerting? Talking about local crime, political issues concerning freedom of speech, supporting local law enforcement, and telling people to check out a neighborhood before buying a home. In a survey of black respondents conducted by a consumer testing firm paid for by Townstone to persuade CFPB to break off its unrelenting attack, not one person took offense to Townstone’s radio show. One respondent even said that Townstone’s comments on crime were “reliable and helpful.”

CFPB lawyers wrote in an internal memo that Townstone could be penalized $28,906 per day for four years, a total of $42,202,760 for alleged violations of civil rights law. All for 16 minutes of radio banter that were not racial in nature.

After seven years of fighting for what was right, the owners of Townstone Mortgage could no longer afford to fight an opponent with unlimited resources. Just prior to the 2024 election, they settled with the CFPB for $105,000.

Now in the wake of the current administration’s efforts to dismantle the CFPB, the agency has gone into court to seek dismissal of the case and have the settlement amount returned to Townstone.

The Dreaded DMV

This Friday marked the last day of spring break for my teen, and the day we booked for him to take his road test to obtain his Hawaii Driver’s License. It did not go well, and it had nothing to do with his ability to drive. I was an idiot last month when I received in the mail the renewal notice for our car’s registration. It got misplaced, and out of sight – out of mind, until 10 days ago. I promptly went online and paid – even having a late fee added. We brought all the paperwork with us to the road test appointment: safety check, proof of insurance, and the old registration – plus the receipt of the online renewal. NOPE! Photocopies of any documents are not allowed. I suggested they look at the original email receipt sent by the DMV to my phone, but that got shut down too. We were turned away and forfeited our $8 fee.

I was clearly wrong for not having all original documents, but it got me thinking later of why the DMV is so strict. If we had been stopped by a police officer on the way to the road test and presented the documents in hand, all would have been accepted. The DMV’s rules are very ominous. Check out the requirements if you want to take the test with either a rental car, or use a car registered to a business:

Rental Vehicle – If you are using a rental vehicle for the road test, it must have the original Certificate of Registration, Certificate of Vehicle Inspection, and Hawaii motor vehicle insurance card. The driver’s license applicant must be listed on the rental contract.

Company Vehicle – If you are using a company vehicle for the road test, you will need a letter, on company letterhead, authorizing you to use the company vehicle for the road test that must be signed by an officer or authorized person of the company. The letter must include the applicant’s name, vehicle license plate, make and vehicle identification number and the date that the vehicle will be used for the road test.

I’m trying to understand what the DMV is trying to prevent. I have never rented a car anywhere that keeps original documents in the car. That would be insane. And for using a company car, what are they thinking? Did the road test applicant steal the car from some company?

Before we all lose sight of what was attempting to be accomplished, it was to test if a person has attained the required skills to be issued a driver's license. The good news is that I walked into the Satellite City Hall and got a duplicate registration within minutes. The road test has been rescheduled for next Thursday.

Our country is now arguing over the size of government, including waste, fraud, and inefficiency. I think it would be a great opportunity to examine all aspects of government and reevaluate if each department is serving us, the public, the best ways possible. Too many times, and too many examples exist of government morphing into something unrecognizable to what it was when created.

And now the week’s economic news…….

Inflation Climbs

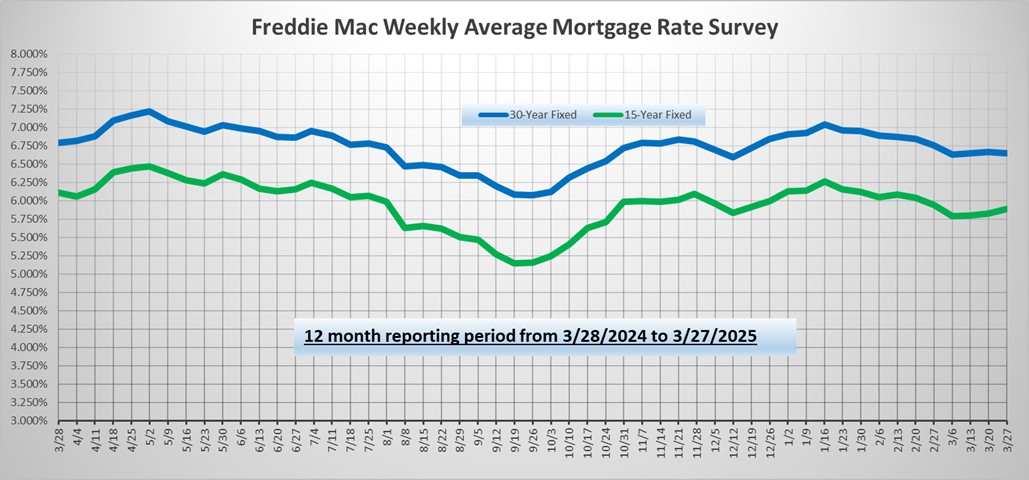

It was a relatively quiet week for mortgage markets. The latest inflation data was a bit stronger than expected. As a result, mortgage rates ended the week slightly higher.

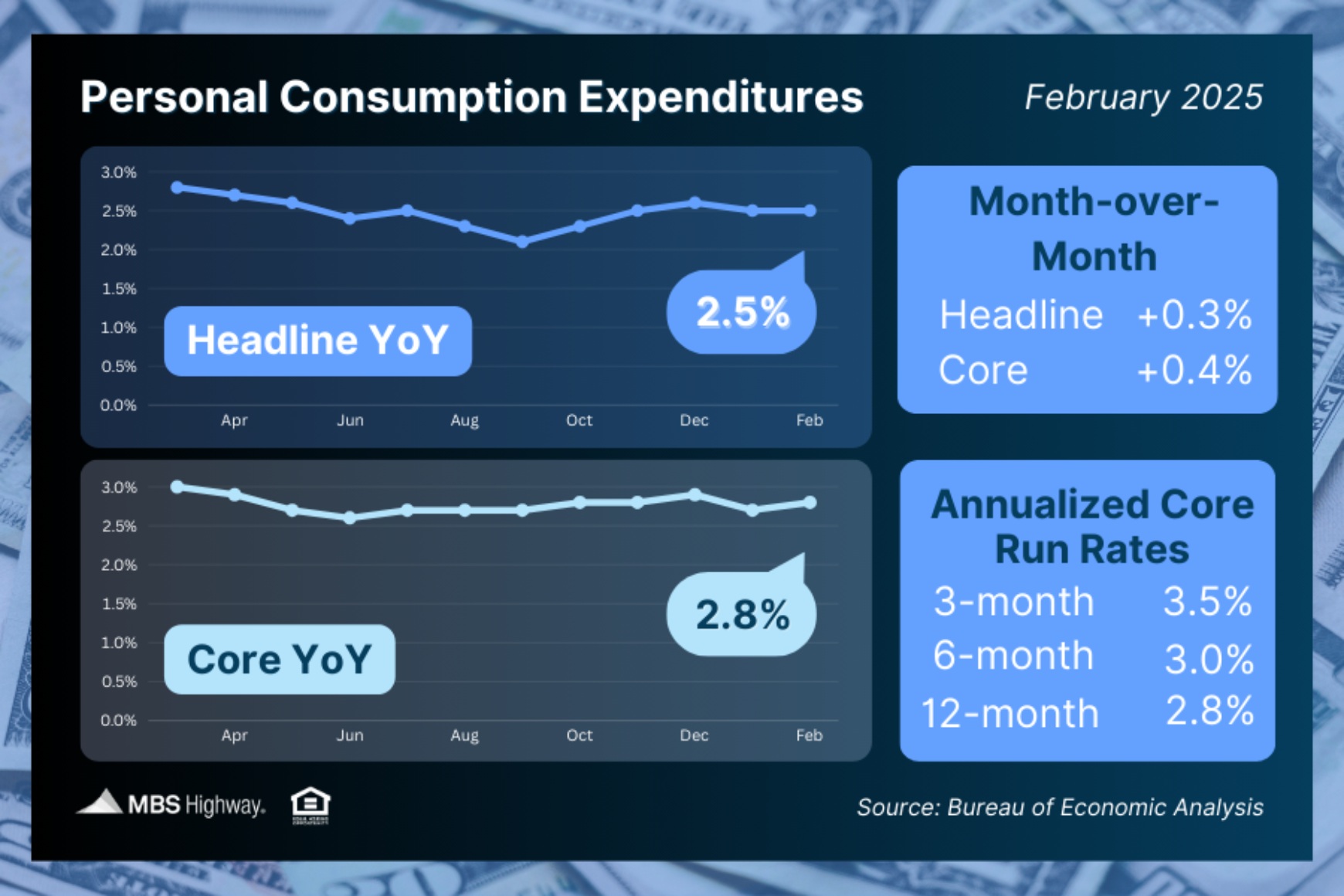

Fed officials keep a close eye on inflation, and the PCE price index is their favored indicator. In February, Core PCE was 2.8% higher than a year ago, slightly above expectations, and up from an annual rate of increase of 2.7% last month. Progress toward the 2.0% target of the Fed has been challenging, and this desired level has not been achieved since February 2021.

Fed officials keep a close eye on inflation, and the PCE price index is their favored indicator. In February, Core PCE was 2.8% higher than a year ago, slightly above expectations, and up from an annual rate of increase of 2.7% last month. Progress toward the 2.0% target of the Fed has been challenging, and this desired level has not been achieved since February 2021.

In February, sales of existing homes rose 4% from January, well above the consensus forecast for a modest decline, but still were a little lower than a year ago. The median existing-home price of $398,400 was up 4% from last year at this time and at a record high for February. Inventories remain stuck at historically low levels, standing at just a 3.5-month supply nationally, far below the 6-month supply typical in a balanced market. However, inventories were 17% higher than a year ago.

After being heavily impacted by unusually bad weather in January, the latest home building data revealed a much larger than expected recovery. Overall housing starts in February jumped 11% from January, with similar gains seen for both single-family and multi-family starts. Less affected by the weather, single-family building permits, a leading indicator of future construction, were nearly flat from January and close to expectations. The supply of new homes available for sale remained near the highest level since 2007. A separate survey of home builder sentiment on housing market conditions from the NAHB unexpectedly dropped sharply to the lowest level in seven months. Builders cited uncertainty about tariffs and rising costs as the primary areas of concern.

Next Week

Investors will continue to look for additional information about tariff policies. For economic reports, the ISM national manufacturing sector index will be released on Tuesday and the services sector index on Thursday. The Trade Deficit also will come out on Thursday. The key Employment report will be released on Friday, and these figures on the number of jobs, the unemployment rate, and wage inflation are always closely watched.

Until next week….

*** Please note that Freddie Mac publishes their weekly rate report on Wednesday mornings from data received Monday and Tuesday.

The graph above is intended to shown rate trends, and not “today’s current rate”. ***

Reviews From Our Past Clients

With every client, we promise to provide you with a comprehensive analysis of your mortgage needs, the best service possible, and the best rates we can find. We make it our mission to have every transaction close with our clients happy with the service we provided. Browse through the hundreds of reviews we’ve received from our clients posted on both Google and Zillow.com, and read what they thought of their experience using Hawaii Mortgage Company.

Google Link:

Hawaii Mortgage Company Review on Google.com

Zillow.com Link:

Hawaii Mortgage Company Reviews on Zillow.com

Our Rate Quote System is Available to You

Our automated rate quoting system is live. Now you can check rates and try different scenarios 24-hours a day. Remember, it’s just a computer. For non-standard rate quotes, such as construction, vacant land, and other specialty programs, you’ll still need to give a call.

Here’s the link: https://www.hawaiimortgage.net/todays-rates/

Do you think all lenders are the same?

There is a difference when you use Hawaii Mortgage Company for your financing. Here’s a short video telling you why:

Broker vs. Banker?

Click the link below to get a quick lesson on why working with a Mortgage Broker will benefit you on your next transaction.