Compliments of

Alan Van Zee

Alan Van Zee

President | NMLS #: 297154

Hawaii Mortgage Company, Inc.

Company NMLS #: 232582

Alan Van Zee is one of the top producing Mortgage Originators in the state, originating over $2,000,000,000 to date. He has written and published this weekly newsletter for the past 18 years. It is the most widely read mortgage, real estate, and finance publication in Hawaii.

Hawaii Mortgage Company, now in our 26th year of providing mortgages to the people of Hawaii, is proud to have a complaint-free history. We make sure our clients are happy!

News and Insight

For the Weekend of April 4th, 2026

Hawaii’s Most Read Mortgage, Real Estate, and Finance Publication for 18 Years

Volume 18 – Issue 27

This isn’t Professional

I got a random call this week from a real estate agent who had lots of questions. The agent is new in the business but not new to buying and selling a home. He is representing a close family friend buying a home on Maui. Being a new real estate agent and not having any lending contacts, he utilized the “in-house” mortgage broker that partners with his real estate company.

His first concern had to do with delays in returning calls and emails. Second, he felt when he asked about specific aspects of his client’s pre-approval, the mortgage representative was overly vague. In fact, when the mortgage representative verbally told the buyers they qualified for the mortgage they were applying for, all he provided was a monthly payment – no rate, no points, no nothing.

That’s why the agent called me. He said he needed my help but couldn’t guarantee the buyers would switch lenders. I was happy to help – regardless of my financial outcome. As a professional, I hate those in my industry that are either bad at their job or deceitful.

That’s why the agent called me. He said he needed my help but couldn’t guarantee the buyers would switch lenders. I was happy to help – regardless of my financial outcome. As a professional, I hate those in my industry that are either bad at their job or deceitful.

I used a reverse payment calculator to determine the rate offered to the buyers based on the payment and loan amount. The result was a rate significantly below the average in the market. To obtain that rate, the borrowers would have to pay about 3-points. The loan amount was large, so the cost of the points was atrocious. We are also in a market where rates are forecast to drop. I would never recommend my clients to pay points when a refinance is 9-12 months down the road.

I told the agent that his situation is no different than a type of call I get at least 5 times per week. The call always starts with “What’s your current rate today?” I then proceed to the virtually automatic reply that “Rates are based on several factors. Let me ask you some questions and I’ll be happy to provide you a rate quote.” After I obtain the purpose of the loan (purchase or refinance), the property value and type, loan amount, and credit score, I offer them the rates to various loan programs.

The reaction is almost always the same: “Oh, I was quoted this lower rate by another lender.”

And I reply with: “With that rate, how many points are they charging you?”

Their response is either: “They never mentioned points” or “What are points?”

As a consumer, YOU need to be in control of your money. No amount of government oversight is going to prevent you from paying more than you should for your mortgage financing. Low rates sound great, but what is it going to cost you? If you don’t understand the terms, ask! You should also get at least 3 quotes. And when obtaining those 3 quotes, the criteria must be the same for each lender you contact, and the quotes need to be obtained on the same day. Rates change daily, sometimes more than once per day. With the war in the Middle East, rates have been more volatile then usual.

One last note on rate quotes. Every mortgage representative, given the information needed, should be able to provide you with a rate quote in under two minutes over the phone. If they require you to furnish information to pull a credit report or tell you they need to do some research and call you back, move on. That’s a lender looking for a way to capture you, not one willing to provide a service. Or they’re incompetent. Either way, that’s not the lender you want to use.

Rule Change is Great News for ADU’s

Often times there’s a disconnect between government zoning, the IRS, and mortgage underwriting rules. What may be allowed under one’s set of rules is not allowed by another. It would be great if they all worked with the same playbook. One of the most unfair underwriting rules that affects too many homeowners looking to qualify for mortgage financing has now finally been fixed.

Our local government enthusiastically encourages homeowners to build ADU’s (accessory dwelling units) to help ease the housing shortage in the state. The IRS clearly requires you to report the rental income on your tax returns – so they can get a piece of it. Yet for mortgage underwriting rules, applicants are shocked to find out that rental income from any portion of their owner-occupied single-family home can’t be used for qualification.

The single-family home is the vast majority of homes in the state. One lot, one home. An ohana or ADU does not change that designation, as the definition of a 2-unit property is the ability to split the property and sell off one of the units. With an ohana or ADU that is not possible.

The restriction on rental income comes from the long-held rule that income from renting a room in your owner-occupied house doesn’t count. In the eyes of those that made the rules, if a family were to rent out a room it simply was a bonus for them, but rental income for qualification was reserved for multi-unit homes and investment properties.

The good news is that someone at Fannie Mae got the bright idea that ADU’s and ohanas are not rooms in one’s home, but rentals encouraged by local governments. Fannie Mae just released new guidelines that now allow income received from ohanas and ADU to be used when an owner-occupant is applying for mortgage financing.

This is a huge change that will benefit many in our state. Over the years I have had to turn down several homeowners wishing to obtain financing because they couldn’t use the rental income to qualify.

Yes, there are rules and steps needed to use that income, but if you’ve been honest and reported that income on your tax return, in almost all cases you should be allowed to use it to qualify for new mortgage financing. If you have any questions, feel free to contact me or your other favorite mortgage professional.

And now the week’s economic news…….

BLS did it Again

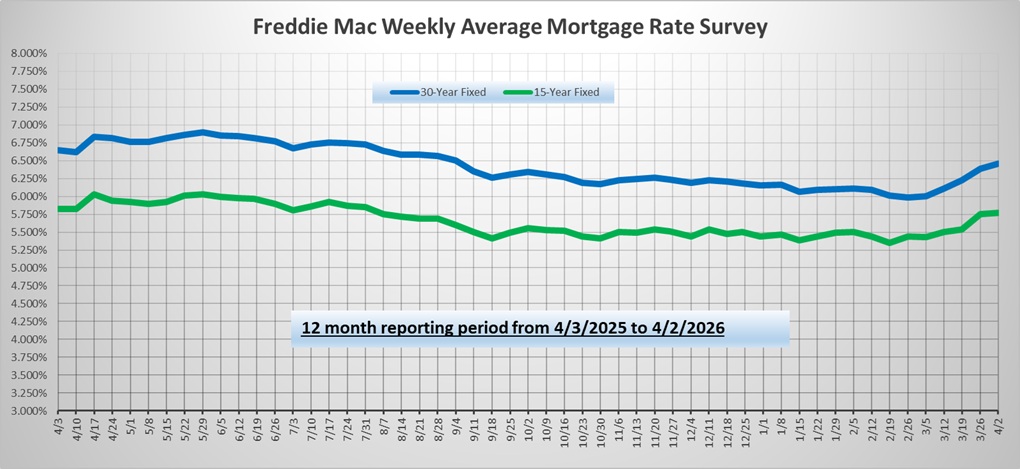

Oil prices continued to drive most of the movement in mortgage markets again this week, and increased optimism for a reduction in hostilities in the Middle East was positive for bonds. However, stronger than expected economic data offset some of the gains, and mortgage rates ended the week only a little lower.

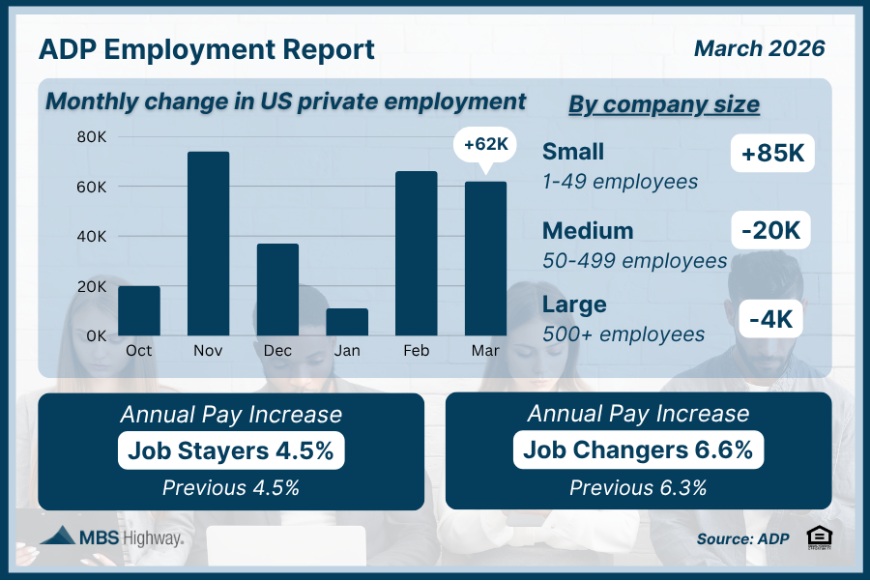

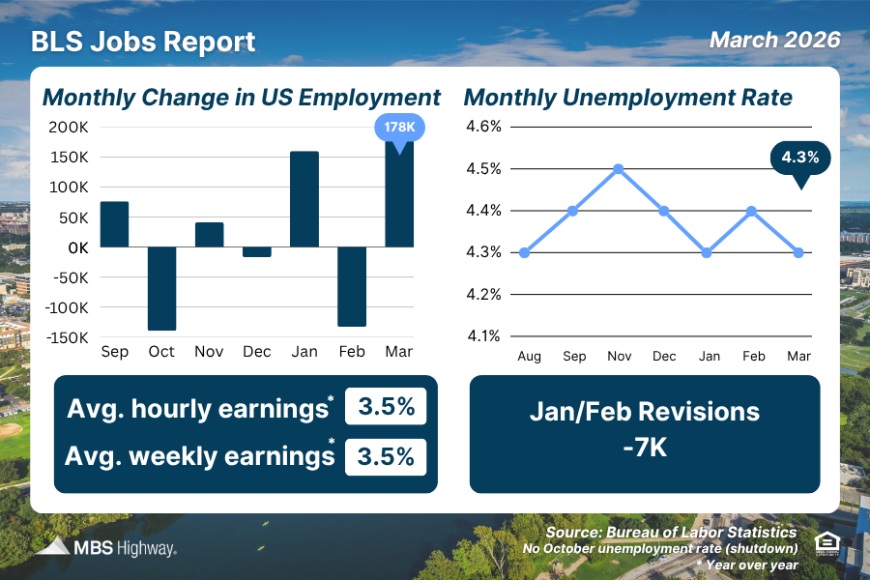

The Bureau of Labor Statistics (BLS) released their Jobs Report for March, showing that there were 178,000 jobs created, which was almost three times as much as estimates of 60,000. This report makes very little sense, especially when compared to ADP and Revelio – private companies, which showed 62,000 and 19,000 jobs created respectively. Additionally, the latter two reports do not include Government jobs. The BLS report said that there were 18,000 jobs lost in that sector. That would mean that the BLS comparatively shows 196,000 jobs created in the private sector, which is very out of touch with the other reports.

The Bureau of Labor Statistics (BLS) released their Jobs Report for March, showing that there were 178,000 jobs created, which was almost three times as much as estimates of 60,000. This report makes very little sense, especially when compared to ADP and Revelio – private companies, which showed 62,000 and 19,000 jobs created respectively. Additionally, the latter two reports do not include Government jobs. The BLS report said that there were 18,000 jobs lost in that sector. That would mean that the BLS comparatively shows 196,000 jobs created in the private sector, which is very out of touch with the other reports.

The BLS report has been extremely volatile. February originally showed 92,000 jobs lost, and that was revised even lower to -133,000. Combined, the two-month gain is 45,000 or roughly 22,000 jobs per month, which is pretty weak.

The BLS report has been extremely volatile. February originally showed 92,000 jobs lost, and that was revised even lower to -133,000. Combined, the two-month gain is 45,000 or roughly 22,000 jobs per month, which is pretty weak.

Within the report, Healthcare and Social Assistance added 89,000 jobs, with Healthcare accounting for 79,000 of the job gains. Again, this is not an economically sensitive sector and where the vast majority of job gains have been coming from. About 35,000 of the jobs were the Kaiser Permanente workers that were on strike and came back to work.

There are two surveys within the Jobs report, the Business Survey and the Household Survey. The Business Survey is where the headline job creation number comes from, and the Household Survey is where the unemployment rate comes from.

The Household Survey showed that there were 64,000 jobs lost in March, very different from the headline job figure. But the unemployment rate still declined from 4.4% to 4.3%, but only because the labor force shrunk by almost 400,000. Most of those individuals are still unemployed, but they are no longer being counted because they have stopped looking for work or are marginally attached to the labor force. This is evidenced by the broader unemployment measure, called the U-6, which adds them back. The U6 unemployment report increased from 7.9% to 8%.

The wage figures within the report were also weak. Average hourly earnings rose by only 0.2% and fell year-over-year from 3.8% to 3.5%. The average amount of hours worked per week fell from 34.3 to 34.2. With the weak hourly earnings figure, average weekly earnings (take home pay) decreased by 0.13% in the month. Year-over-year, weekly earnings fell from 4.1% to 3.5%.

Another significant economic report released this week from the Institute of Supply Management (ISM) also exceeded expectations. The ISM national manufacturing sector index was 52.7, above the consensus forecast of 52.0 and the highest level since 2022. Readings above 50 indicate an expansion in the sector and below 50 a contraction. After spending the final ten months of 2025 below 50, the manufacturing sector has surpassed that level for the first three months of this year. While future tariff policies are more uncertain after the Supreme Court ruling in February, the higher tariffs on foreign goods imposed last year may be providing a lift to domestic manufacturing companies.

Consumer spending accounts for over two-thirds of U.S. economic activity, so the monthly Retail Sales report is a key measure of the health of the economy. Delayed by the government shutdown, the most recent data revealed that retail sales in February rose 0.6% from January, which was a little above expectation and the largest monthly increase since July.

Next Week

Looking ahead, attention will remain fixed on the conflict in the Middle East. Investors also will monitor comments from Fed officials about future monetary policy. For economic data, the ISM national services sector index will come out on Monday. After that, two big inflation reports will be released in the same week due to disruptions from the government shutdown. The PCE price index, the inflation indicator favored by the Fed, will come out on Thursday. The Consumer Price Index (CPI), a widely followed monthly inflation indicator that looks at the price changes for a broad range of goods and services, will be released on Friday.

Until next week….

*** Please note that Freddie Mac publishes their weekly rate report on Wednesday mornings from data received Monday and Tuesday.

The graph above is intended to shown rate trends, and not “today’s current rate”. ***

Reviews From Our Past Clients

With every client, we promise to provide you with a comprehensive analysis of your mortgage needs, the best service possible, and the best rates we can find. We make it our mission to have every transaction close with our clients happy with the service we provided. Browse through the hundreds of reviews we’ve received from our clients posted on both Google and Zillow.com, and read what they thought of their experience using Hawaii Mortgage Company.

Google Link:

Hawaii Mortgage Company Review on Google.com

Zillow.com Link:

Hawaii Mortgage Company Reviews on Zillow.com

Our Rate Quote System is Available to You

Our automated rate quoting system is live. Now you can check rates and try different scenarios 24-hours a day. Remember, it’s just a computer. For non-standard rate quotes, such as construction, vacant land, and other specialty programs, you’ll still need to give a call.

Here’s the link: https://www.hawaiimortgage.net/todays-rates/

Do you think all lenders are the same?

There is a difference when you use Hawaii Mortgage Company for your financing. Here’s a short video telling you why:

Broker vs. Banker?

Click the link below to get a quick lesson on why working with a Mortgage Broker will benefit you on your next transaction.