Compliments of

Alan Van Zee

Alan Van Zee

President | NMLS #: 297154

Hawaii Mortgage Company, Inc.

Company NMLS #: 232582

Alan Van Zee is one of the top producing Mortgage Originators in the state, originating over $2,000,000,000 to date. He has written and published this weekly newsletter for the past 18 years. It is the most widely read mortgage, real estate, and finance publication in Hawaii.

Hawaii Mortgage Company, now in our 26th year of providing mortgages to the people of Hawaii, is proud to have a complaint-free history. We make sure our clients are happy!

News and Insight

For the Weekend of April 11th, 2026

Hawaii’s Most Read Mortgage, Real Estate, and Finance Publication for 18 Years

Volume 18 – Issue 28

A Lesson to be Learned by Everyone

I received an inquiry this week from a client I provided a mortgage for 5 years ago. They got a great rate on that first mortgage and didn’t want to touch it. They did want to access some of the equity in their home and were inquiring about a Home Equity Line of Credit of $100,000.

In the world of Home Equity loans there are two paths. The first path is a great rate and terms – often an introductory rate provided by the big banks in town. The downside? These HELOC departments are the tortoise to the regular mortgage side being the hare. HELOC’s from the local banks take on average 6-8 weeks to complete. I’m not sure why – they just do. The second path is a group of Home Equity products now offered by the big mainland lenders. Their rates are significantly higher, but they can close quickly. I recently closed one for a client in 10 days.

I always look out for the best interest of the client, regardless of whether receiving income or not. I’ve always believed that if you do it right, you’ll always get rewarded. That’s why when my client expressed a need to get the HELOC in place quickly, I suggested they check with their credit union to see how quickly they could turn things for them because I wanted them to get the best rate possible. But I did caution that if anyone suggested they touch their 2.750% fixed rate first mortgage, they call me back first to see if there was any other alternative.

I got a call back within 30 minutes of our initial call. They were stressed that the credit union couldn’t help them quickly either. I have a son going to college this fall and realize some bills come out of nowhere, even if you plan. That’s when I asked if I could inquire what they were going to use the money for. After a pause, they confided that they invested in some type of crypto investment that turned out to be fraudulent and lost a large amount of money. They said the good news is that they were working with a person at the government’s financial crimes division who was successful in helping others recover their losses. They said they needed the funds from the HELOC to act as some type of bond until the government could release the seized funds back to them. They had two weeks to put the funds into a new crypto account.

That’s when my spidey-senses kicked in. This made no sense to me whatsoever. My clients came to me because they trusted me, so I asked them for the correspondence they had from this government representative. Everything they forwarded to me didn’t make sense, so I went digging. It turns out, sadly, my clients were about to be the victims of a second scam. Everything they forwarded to me was fake. Even the website for the government agency this person worked for has a huge banner on their webpage:

This news was devastating to my clients. They felt awful after losing $30,000 in a scam. Their only peace was that the government was there to help them get their funds back. When I presented what I had found to prove this was a second scam, I was first met with skepticism. When my proof finally hit them, the sound on the other end of the phone made me want to cry myself. They then confided that they had already given this second scammer $30,000. They were now out $60,000 in total.

Victims of a scam are the easiest people to scam again because they feel desperate and want to be made whole again. It’s no different than a gambler making unwise bets trying to win back what was already lost. They aren’t thinking clearly and make decisions with emotions versus logic.

The conclusion of the phone call was very somber. But here is how I left it. I told them to feel fortunate today because they called me. Had I been someone just looking to make money on another loan, versus investigating what sounded stressful to me, they would have lost another $90,000. In that context, that day, they did win – by not losing more.

I share this story today not to get a pat on the back, but to expose you to what dangers are out there waiting to steal your hard-earned money. Here’s some simple advice. Please share it with your friends and family.

NEVER conduct financial transactions via text, or texting apps – especially encrypted apps like Signal, Telegraph, or WhatsApp.

ALWAYS verify the person you are in contact with by way of other sources. Conduct an internet search for their office and phone number. Do another search using that person’s name and/or company along with the term SCAN or FRAUD in the search.

REALIZE that the government doesn’t text or use encrypted apps. They will also never ask you to send them funds in cryptocurrency.

And most important, IF IT SOUNDS TO GOOD TO BE TRUE, it most likely isn’t true.

What’s with Adding “S” to the End of Words Hawaii?

I wrote a piece years ago highlighting the incorrect names used for a couple of popular but dangerous places in East Oahu. China Wall and Spitting Cave. Living in Hawaii Kai, not a day goes by that fire rescue is not called out to save another injured swimmer.

The issue is with technology. You see, years ago Google someone tagged these two places in Google as China Walls and Spitting Caves. I can assure you as someone that to this day still enjoys a jump in the ocean at both spots, that there is only one wall and only one cave. These placename areas should not be pluralized. I tried to get Google to update its error, but that was no luck. And since the Google has officially pluralized their names, everyone now uses that erroneous information. So now these spots will I guess forever have the wrong names - except for those that know better.

Then Hawaii got hit by the Kona Lows. Night after night on the local news we learned of the “impacts” each storm brought. “Impact” from a storm is not pluralized. “The impact of the storm was wide and extensive.” “The storm impacted…” No “s” either. It has been like nails on a chalkboard for me.

Okay, I’m weird when it comes to usage of the English language. Maybe because I write to you each week and pride on writing proper English. Maybe I should just calm down and relax by my new backyard pond – compliments of the impacts of the latest storm.

And now the week’s economic news…….

Oil Prices Drop

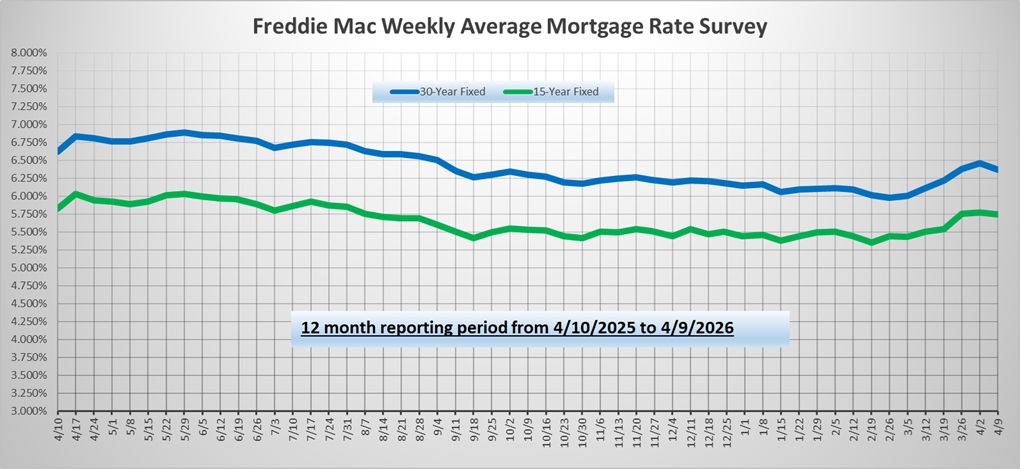

The biggest movement in mortgage markets this week took place after the announcement of a temporary ceasefire in the conflict in the Middle East. Oil prices fell, and mortgage rates followed suit. Two major inflation reports were close to expectations and caused little reaction. As a result, mortgage rates ended the week a bit lower.

News of a two-week ceasefire caused oil prices to decline sharply on Wednesday. This reduced future inflationary pressures, which was positive for mortgage rates. Concerns about the durability of the ceasefire increased later in the week, however, reducing the initial impact of the announcement.

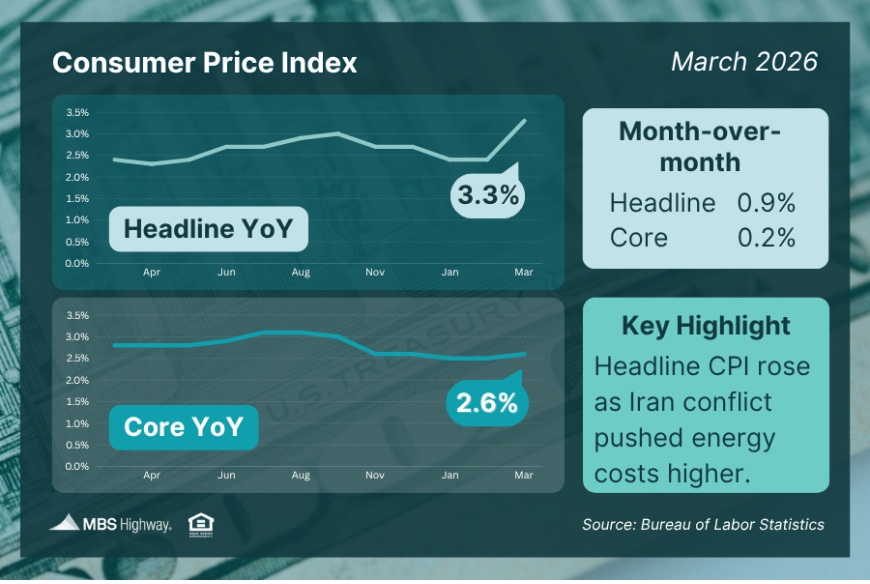

The Consumer Price Index (CPI) is one of the most closely watched inflation indicators released each month, and investors were braced for the effects of the huge rise in oil prices in March. CPI surged a massive 0.9% from February, the largest monthly increase since June 2022, but matching expectations. CPI was 3.3% higher than a year ago, up substantially from an annual rate of 2.4% last month and the highest level since May 2024.

The Consumer Price Index (CPI) is one of the most closely watched inflation indicators released each month, and investors were braced for the effects of the huge rise in oil prices in March. CPI surged a massive 0.9% from February, the largest monthly increase since June 2022, but matching expectations. CPI was 3.3% higher than a year ago, up substantially from an annual rate of 2.4% last month and the highest level since May 2024.

To reduce short-term volatility and get a better sense of the underlying inflation trend, investors look at core CPI, which excludes food and energy. In March, Core CPI was 2.6% higher than a year ago, up from 2.5% last month, but slightly below expectations. Shelter (housing) costs were up 3.0% on an annual basis and continue to be a primary reason why bringing down inflation remains challenging, but this reading has been trending lower in recent months.

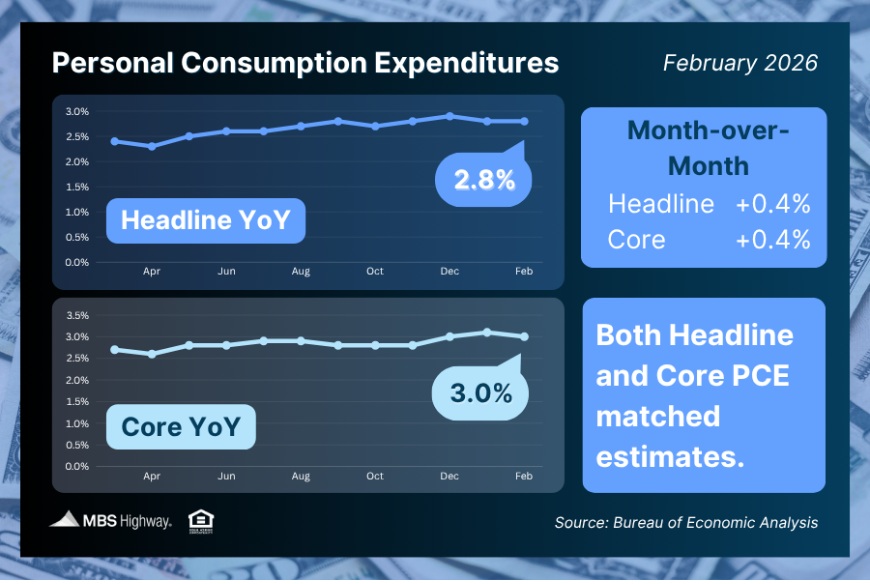

Fed officials keep a close eye on inflation, and the PCE price index is their favored indicator. One of the significant differences with CPI is that PCE places more weight on health care costs and less on shelter. Delayed by the government shutdown, the latest report revealed that Core PCE in February was 3.0% higher than a year ago, down from an annual rate of increase of 3.1% in January and matching the consensus forecast. Progress toward the 2.0% target of the Fed has not been easy, and this desired level has not been achieved since February 2021.

Fed officials keep a close eye on inflation, and the PCE price index is their favored indicator. One of the significant differences with CPI is that PCE places more weight on health care costs and less on shelter. Delayed by the government shutdown, the latest report revealed that Core PCE in February was 3.0% higher than a year ago, down from an annual rate of increase of 3.1% in January and matching the consensus forecast. Progress toward the 2.0% target of the Fed has not been easy, and this desired level has not been achieved since February 2021.

Next Week

Looking ahead, attention will remain fixed on the conflict in the Middle East. Investors also will monitor comments from Fed officials about future monetary policy. For economic data, Existing Home Sales will come out on Monday. The Producer Price Index (PPI), a monthly inflation indicator, will be released on Tuesday. Import Prices will come out on Wednesday.

Until next week….

*** Please note that Freddie Mac publishes their weekly rate report on Wednesday mornings from data received Monday and Tuesday.

The graph above is intended to shown rate trends, and not “today’s current rate”. ***

Reviews From Our Past Clients

With every client, we promise to provide you with a comprehensive analysis of your mortgage needs, the best service possible, and the best rates we can find. We make it our mission to have every transaction close with our clients happy with the service we provided. Browse through the hundreds of reviews we’ve received from our clients posted on both Google and Zillow.com, and read what they thought of their experience using Hawaii Mortgage Company.

Google Link:

Hawaii Mortgage Company Review on Google.com

Zillow.com Link:

Hawaii Mortgage Company Reviews on Zillow.com

Our Rate Quote System is Available to You

Our automated rate quoting system is live. Now you can check rates and try different scenarios 24-hours a day. Remember, it’s just a computer. For non-standard rate quotes, such as construction, vacant land, and other specialty programs, you’ll still need to give a call.

Here’s the link: https://www.hawaiimortgage.net/todays-rates/

Do you think all lenders are the same?

There is a difference when you use Hawaii Mortgage Company for your financing. Here’s a short video telling you why:

Broker vs. Banker?

Click the link below to get a quick lesson on why working with a Mortgage Broker will benefit you on your next transaction.