Compliments of

Alan Van Zee

Alan Van Zee

President | NMLS #: 297154

Hawaii Mortgage Company, Inc.

Company NMLS #: 232582

Alan Van Zee is one of the top producing Mortgage Originators in the state, originating over $2,000,000,000 to date. He has written and published this weekly newsletter for the past 17 years. It is the most widely read mortgage publication in Hawaii.

Hawaii Mortgage Company, now in our 25th year of providing mortgages to the people of Hawaii, is proud to have a complaint-free history. We make sure our clients are happy!

Mortgage Market News and Insight

For the Weekend of April 12th, 2025

Hawaii’s Most Read Mortgage Publication for 17 Years

Volume 17 – Issue 30

Recognize the Problems Early

My client’s purchase transaction closed this week, and he’s now moving into his condo this weekend. I have another client I pre-approved for financing this week, that is spending this weekend looking for his perfect condo to purchase. Each of these clients came to me despite starting the mortgage process with another lender – then switching because they didn’t have a good feeling about the choice they had made.

I love my job of providing mortgage financing because I am not an order taker. Each client that comes to me is unique. Each has quirks about something that needs to be solved in order to qualify. Solving those puzzles are what makes every day at the office different. You make think your situation and documentation are straight forward, but rarely do I come across what we call the “vanilla” client.

I love my job of providing mortgage financing because I am not an order taker. Each client that comes to me is unique. Each has quirks about something that needs to be solved in order to qualify. Solving those puzzles are what makes every day at the office different. You make think your situation and documentation are straight forward, but rarely do I come across what we call the “vanilla” client.

My advice to you today is to demand professionalism, knowledge, excellent and prompt communication, and honesty from your mortgage originator. If you missed the cues and submitted your application to a lender and now have second thoughts about the choice you made, you should talk to another lender ASAP. I’ve had people come to me in tears requesting I take over their financing. Unfortunate for some, they waited too long, and switching lenders would have required the closing date get extended – an option many buyers feel they don’t have.

Today let’s review what instigated my two clients switching from the lender they were working with to working with me and my team. A lesson can be learned.

Johnny “Vanilla”:

As I stated above, I rarely see a truly “vanilla” borrower – excellent credit, verifiable income, all monies sourced, and the condo project had no issues. Yes, Johnny was that rare client. He called me a month ago rate shopping. It wasn’t long into our conversation that Johnny let me know that he was already working with another lender. The reason he was shopping around is that the mortgage representative Johnny was working with was not very responsive to his questions about the process or what rates he could offer. Johnny was surprised that I could give him an accurate rate quote over the phone by just asking a few questions. His current lender had a complete application and documentation, yet couldn’t furnish rate options.

Johnny was referred to this mortgage originator by a friend. I will let you in on a little secret with referrals and salespeople. If a salesperson doesn’t believe they need to compete for your business, they won’t try as hard. Maybe that was the case with this person. Or maybe being evasive when asked questions was his mistaken belief in how to win over clients.

Johnny’s biggest concern was switching lenders and still closing on time. Johnny was 14 days into his 45-day contract, and the lender he didn’t want to work with any longer had already ordered his appraisal.

In one business day we were able to lock in Johnny’s rate and get his appraisal transferred. Johnny’s purchase transaction closed this week – early! He’s thrilled, and so happy he listened to that little voice inside that told him something wasn’t right.

Malcolm “Makes Money”:

Malcolm is the opposite of Johnny. Malcolm’s situation is complicated. He and his wife own a home in the Mid-West. She works here in Hawaii full time. He travels back and forth. Malcolm makes a good return on some very special investment opportunities on the mainland, but in exchange that complicates his tax return significantly.

Malcolm went through two other lenders before finding me on the internet. The first lender told him he could only get him financing if he were willing to put up a large down payment. The second lender asked for tons of documents, then told Malcolm he couldn’t help.

Each of these lenders failed their client because of communication. First, neither lender listened closely to Malcolm’s story. If they had, they would have structured the transaction correctly to meet the guidelines of lending. Secondly, again, another communication issue, they didn’t explain in detail what was expected from the client to have success in obtaining loan approval. Malcolm is a busy business guy. Having to go through the mundane tasks of an online application and gathering all that paperwork was too much work for Malcolm. I had a heart-to-heart with Malcolm on what it was going to take to get him is mortgage loan. Once I communicated what he needed to do, and more importantly why he needed to furnish certain items, we got what we needed and issued his pre-approval.

Unfortunately, you can’t pick a lender based on the company or an individual’s reputation alone. Because every client is different, the way that mortgage originator interacts with a client will be different too. You the consumer needs to ask questions – lots of them. That original meeting with the mortgage representative, be it on the phone or in person, should feel like you’re conducting a job interview. If we want your business, we need to earn your business.

Even if you’ve started the process with a lender, you should never feel trapped by that decision you made. At the first sign of issues, you should evaluate the possibility of moving lenders. The worst thing you can do is nothing and eat away the remaining time you have to close. Will switching lenders delay your closing? You will never know until you explore your options.

Don’t feel trapped. And don’t wait until it may be too late to do anything about it.

Kudos to US Rep. Ed Case

This week Representative Ed Case broke from party lines and voted for a measure he felt strongly about. In today’s hyper-partisan Washington, breaking from one’s party for anything is a rarity. The fact that he was willing to take a stand contrary to party leadership is a quality we rarely see these days. In fact, only 4 democrats voted with the republicans on this bill.

What was the bill? Case voted to require proof of citizenship to vote. To me, it’s a no-brainer. With an estimated 30 million (call ‘em what you want – illegals, undocumented, migrants) living in the US, we as citizens should be concerned that only US citizens decide who gets to represent us.

Our other member of congress Representative Jill Tokuda stuck with the party line that the bill would block legitimate qualified voters from exercising their right to vote because many cannot produce proof of citizenship.

If you were born in the US, it would be easy to obtain a copy of your birth certificate from the state you were born in. If you immigrated and are now a US citizen, that achievement is a very proud moment of your life. I guarantee you’ve kept your citizenship papers in a very safe place. No naturalized citizen would ever lose track of that paperwork.

Despite the ease of obtaining documents, politicians like Jill Tokuda insist some people lack the skills to obtain documents and an ID. That type of thinking where you claim a certain socio-economic group cannot accomplish something others can, is referred to as “The soft bigotry of low expectations”. Does Tokuda really believe in her heart that certain groups of people lack the skills to obtain the documents needed to prove citizenship? Really? Or does her party want to make it easy for non-citizens to vote in our elections. Either answer is troubling.

Thank you, Ed Case for standing for your principles.

And now the week’s economic news…….

Inflation Eases

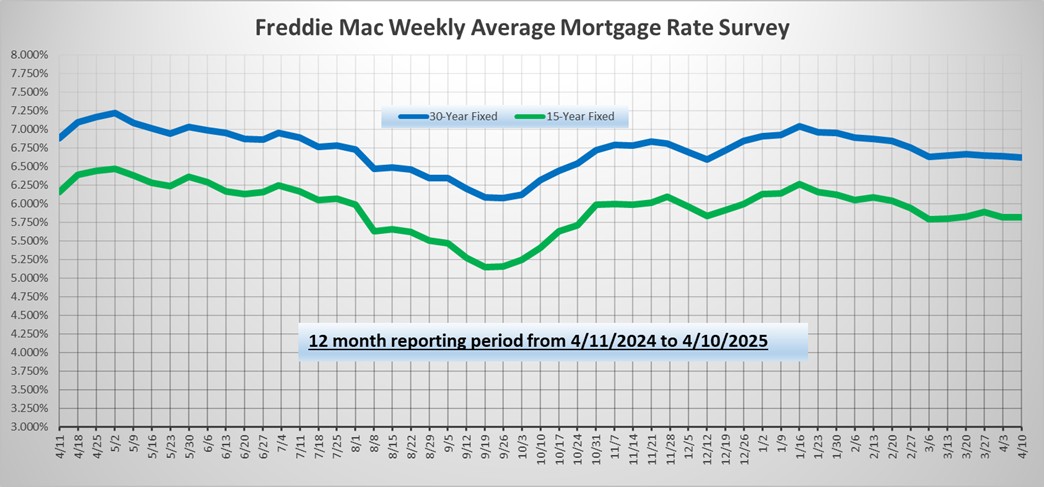

It was a puzzling week for mortgage markets. Tariffs remained the primary focus for investors, and the latest news (see below) was major, but it did not appear to justify a huge selloff in bonds. Beyond that, the most recent inflation data was much lower than expected, a positive for mortgage markets. However, rates ended the week significantly higher.

On Wednesday afternoon, President Trump announced that higher tariffs will be paused for 90 days for most countries, allowing time for negotiations, while tariffs on China will be raised significantly. Bond yields then climbed sharply on Thursday and Friday, although the reasons are not clear. One possibility is that investors are concerned that China may retaliate by selling its holdings of U.S. bonds. Foreign countries own about 15% of U.S. mortgage-backed securities (MBS), and the top two holders are Japan and China, meaning that it is possible. The question, though, is how likely it is to occur. Beyond this, there have been reports that some investment firms have been forced to sell bonds to raise funds to cover margin calls due to recent losses in the stock market. Finally, foreign investors may simply be selling U.S. assets due to the uncertainty, causing the value of the dollar to fall and bond yields to rise.

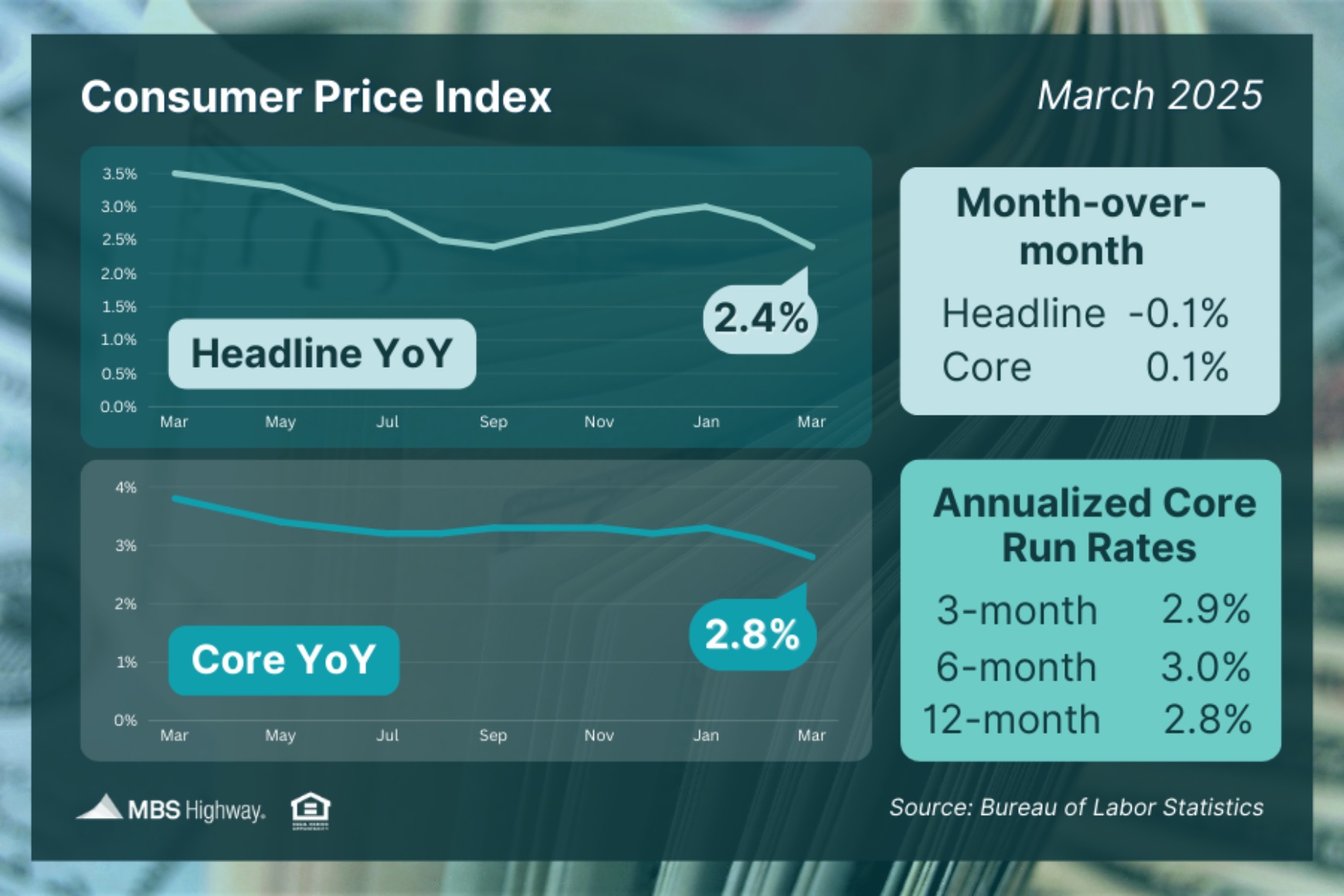

The Consumer Price Index (CPI) is one of the most closely watched inflation indicators released each month. To reduce short-term volatility and get a better sense of the underlying inflation trend, investors look at core CPI, which excludes food and energy. In March, Core CPI was 2.8% higher than a year ago, well below the consensus forecast and the lowest annual rate since March 2021.

The Consumer Price Index (CPI) is one of the most closely watched inflation indicators released each month. To reduce short-term volatility and get a better sense of the underlying inflation trend, investors look at core CPI, which excludes food and energy. In March, Core CPI was 2.8% higher than a year ago, well below the consensus forecast and the lowest annual rate since March 2021.

Although this annual rate is down significantly from a peak of 6.6% in September 2022, and from 3.9% in January of last year, it is still far above the readings around 2.0% seen early in 2021, which is the stated target level of the Fed. Shelter (housing) costs continue to be a primary reason why progress on bringing down inflation remains challenging. However, airline fares, prescription drug costs, and used vehicle prices dropped sharply in March.

Next Week

Investors will continue to look for additional information about tariff policies. For economic reports, Import Prices will come out on Tuesday. Retail Sales will be released on Wednesday. Since consumer spending accounts for over two-thirds of U.S. economic activity, the retail sales data is a key measure of the health of the economy. Housing Starts will come out on Thursday. Mortgage markets will close early on Thursday and will be closed on Friday for Good Friday.

Until next week….

*** Please note that Freddie Mac publishes their weekly rate report on Wednesday mornings from data received Monday and Tuesday.

The graph above is intended to shown rate trends, and not “today’s current rate”. ***

Reviews From Our Past Clients

With every client, we promise to provide you with a comprehensive analysis of your mortgage needs, the best service possible, and the best rates we can find. We make it our mission to have every transaction close with our clients happy with the service we provided. Browse through the hundreds of reviews we’ve received from our clients posted on both Google and Zillow.com, and read what they thought of their experience using Hawaii Mortgage Company.

Google Link:

Hawaii Mortgage Company Review on Google.com

Zillow.com Link:

Hawaii Mortgage Company Reviews on Zillow.com

Our Rate Quote System is Available to You

Our automated rate quoting system is live. Now you can check rates and try different scenarios 24-hours a day. Remember, it’s just a computer. For non-standard rate quotes, such as construction, vacant land, and other specialty programs, you’ll still need to give a call.

Here’s the link: https://www.hawaiimortgage.net/todays-rates/

Do you think all lenders are the same?

There is a difference when you use Hawaii Mortgage Company for your financing. Here’s a short video telling you why:

Broker vs. Banker?

Click the link below to get a quick lesson on why working with a Mortgage Broker will benefit you on your next transaction.