Compliments of

Alan Van Zee

Alan Van Zee

President | NMLS #: 297154

Hawaii Mortgage Company, Inc.

Company NMLS #: 232582

Alan Van Zee is one of the top producing Mortgage Originators in the state, originating over $2,000,000,000 to date. He has written and published this weekly newsletter for the past 18 years. It is the most widely read mortgage, real estate, and finance publication in Hawaii.

Hawaii Mortgage Company, now in our 26th year of providing mortgages to the people of Hawaii, is proud to have a complaint-free history. We make sure our clients are happy!

News and Insight

For the Weekend of April 25th, 2026

Hawaii’s Most Read Mortgage, Real Estate, and Finance Publication for 18 Years

Volume 18 – Issue 30

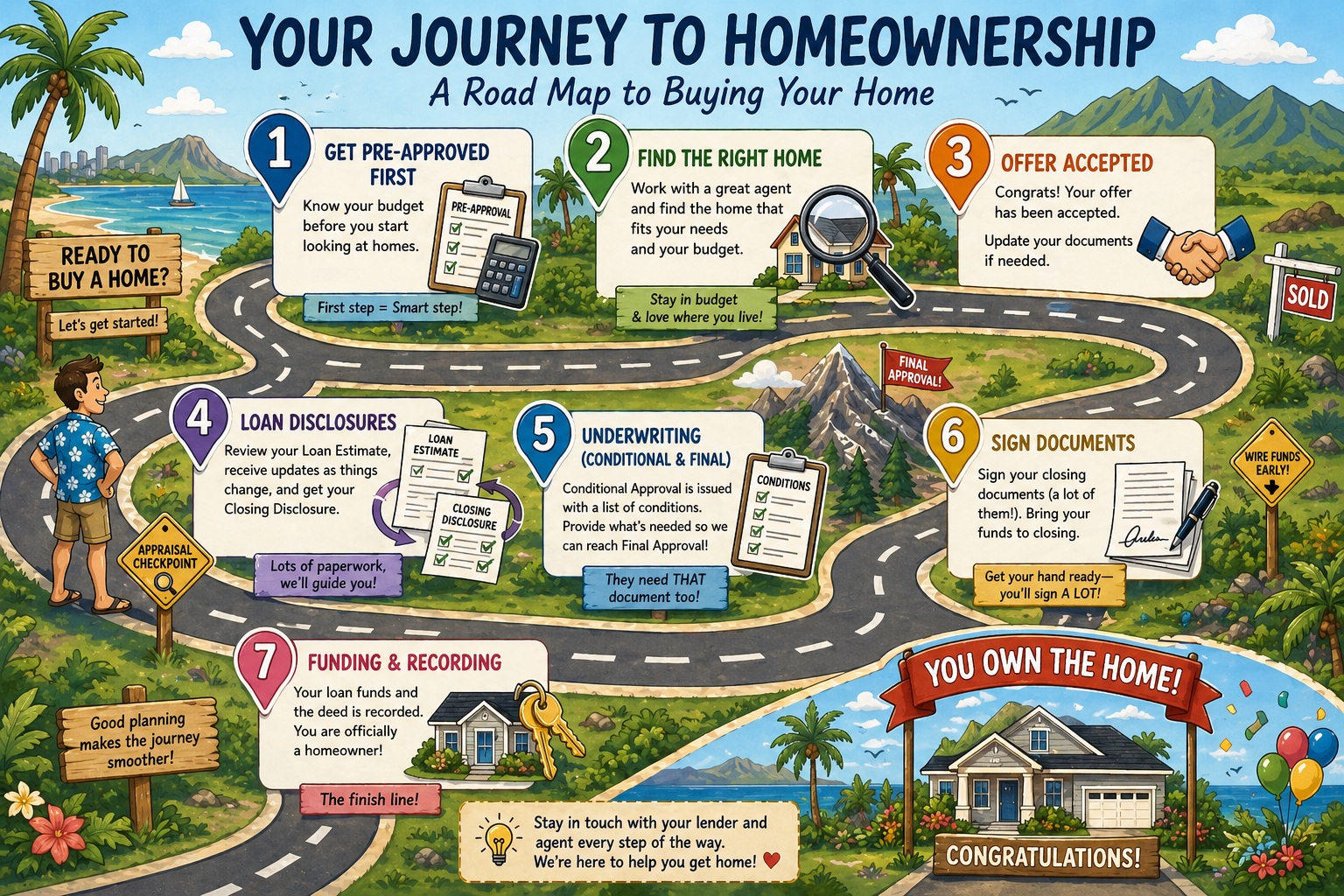

The Steps in Buying a Home

It occurred twice this past week that clients deeply into the process of buying a home were truly unaware of the steps along the way. When should you start looking at properties? When is your loan truly approved? When do you need to come up with the remainder of the money? Today, I’ll provide a simple roadmap you can use when you’re ready to buy a home.

Financing Pre-Approval:

No matter what you think you know about how much you can afford, if it involves any amount of mortgage financing, this is your first step. Don’t look at a single home in any price range until you complete this step.

The pre-approval process is simple. You’ll complete a mortgage application and provide your lender with your income and asset documents. They will review what you’ve provided and let you know how much you can finance; plus let you know which mortgage programs would be the best to meet your financial goals. The pre-approval process is an exercise in math. We calculate your maximum debt-to-income ratio based on the loan program you qualify for.

Why do this before looking at homes? Simple. If you started looking at $700,000 homes and then later found out you could only afford the $600,000 homes, nothing you will find in the lower price range will compare, and you’ll be disappointed. It’s like shopping for a car and starting at the Lexus dealer but your finances can only afford a Toyota. A fully loaded Toyota is a great car – but it is not a Lexus. Don’t make that mistake when buying a home.

Now Go House Hunting:

Once you have your finances in place and your lender has provided you a maximum loan amount, find a great agent to help you find the home of your dreams – or the home that fits your budget. When you find a home to make an offer on, make sure to check with your lender first to make sure there’s nothing about the property you want to buy that may present issues for financing. Condos are tricky with pre-approval loan amounts. HOA fees vary greatly so what you think you qualified for based on what your lender used, may not work for a condo with higher taxes and HOA fees.

Your Offer is Accepted:

Depending on how long the house hunt took, your lender will most likely ask for updated income and asset documents. In mortgage lending, every document has a shelf-life.

Disclosures, Disclosures, Disclosures:

Once your application is submitted to a lender an initial set of disclosures will be issued for you to read and sign. This group of forms is called the Loan Estimate. This initial set of disclosures will outline the maximum fees estimated for your transaction. In many cases the fees are estimated higher than what they’ll eventually be, as lending rules prohibit some fees being raised after disclosure, but they can easily be lowered once the actual amount is known.

At any point in the transaction when the material facts that determine fees would change, a new set of disclosures will be issued. For example, when the appraisal comes in and the value is different than the estimated value, it will trigger a new disclosure. A new disclosure will also be issued if new services are requested. A good example is when a buyer decides before closing to have the property close in their trust. That will incur additional fees and a new disclosure.

When all fees have been verified and all invoices accounted for, the Closing Disclosure will be issued.

Underwriting (Conditional & Final):

Once an underwriter reviews your application, which will include a review of your income, credit, assets, plus the property (appraisal, title report, termite inspection, deed, and survey), they will issue what’s called Condition Loan Approval. Your loan is approved, so long as the list of items (conditions) they list, can be satisfied.

These conditional items commonly include additional pay stubs, updated bank statements, correction of something in the appraisal, proof of liquidation of funds, employment verifications, and receipt of your insurance for the new property. In almost 30 years of providing loans, I have never seen an approval with zero conditions. It simply isn’t possible.

This is also the time in the transaction where the borrower becomes upset with the mortgage processing staff. “Why does the underwriter want that?... I already provided that… Let me help you out right now. It is not a test of will. You either provide it, or don’t obtain financing. Sometimes mistakes are made, but a good mortgage processing staff will jump in long before we ask you for something dumb.

Final Loan Approval is the point where all conditions have been satisfied.

Document Signing and Recordation:

You will sign your giant packet of documents before a notary, either at the escrow/title office, or with a mobile notary – they can come anywhere you’re at! Get your hand ready, as you’ll provide your signature probably 30 times or more. Part of the closing packet is knowing how much money you’ll need to send to the title company. A wire from your bank is the best way. Find out from your bank well before signing how to wire funds to title.

After everything’s signed and the lender confirms nothing was missed, they wire their funds (your loan amount) to the title company. Hawaii requires all funds to be in the title company’s accounts two days prior to closing.

With all funds in, you’ve finally reached recording day – the day your documents are recorded at the Bureau of Conveyances. Once the title company gets confirmation the mortgage and deed were recorded, your home is now officially yours!

I hope this sheds some light on a confusing and drawn-out process. If at any point in the transaction you need clarification, have questions, or have a genuine concern, you should be able to get in touch with your lender with ease. If they’ve gone AWOL, there’s something behind the scenes you should be concerned about.

Buying a home should be one of the best experiences of your life. With the right people in your corner it can be.

And now the week’s economic news…….

Consumers Spending Surges

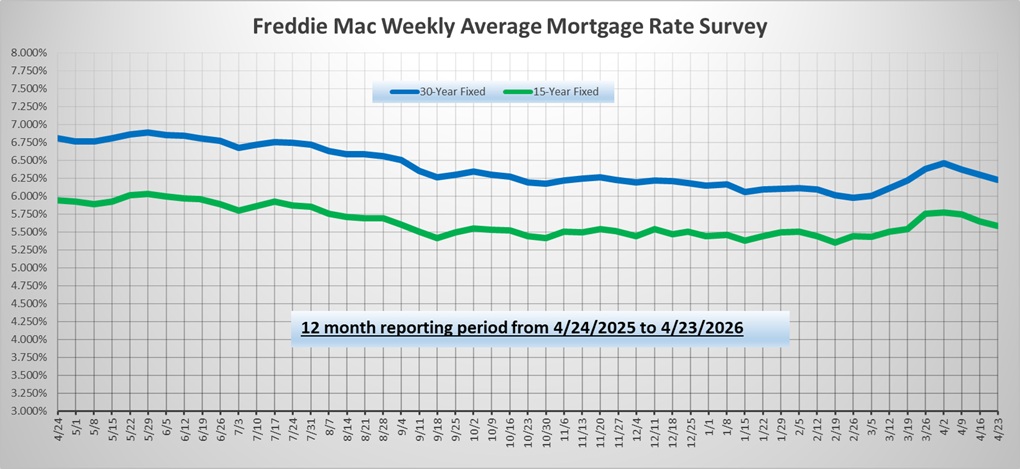

News about negotiations to end the conflict in the Middle East caused volatility for mortgage markets this week. The most significant economic report revealed stronger than expected consumer spending, but its impact was minor. Mortgage rates ended the week flat from last week.

Consumer spending accounts for over two-thirds of U.S. economic activity, so the monthly Retail Sales report is a key measure of the health of the economy. While economists had anticipated that larger than usual tax refunds would provide extra ammunition, they also had to factor in that the enormous rise in gas prices in March might sap some of that strength. As a result, the consensus forecasts spanned a wide range for this report.

Consumer spending accounts for over two-thirds of U.S. economic activity, so the monthly Retail Sales report is a key measure of the health of the economy. While economists had anticipated that larger than usual tax refunds would provide extra ammunition, they also had to factor in that the enormous rise in gas prices in March might sap some of that strength. As a result, the consensus forecasts spanned a wide range for this report.

The actual result was a nice surprise to the upside. Retail sales in March surged 1.7% from February, above the consensus forecast of 1.4% and the largest monthly increase in a year. Even excluding the record rise in sales of gas (which are measured by dollar value), unexpected strength was seen broadly. Nearly every category in the report, from furniture to motor vehicles to electronics, posted gains.

The Department of Labor releases the total number of new claims for unemployment insurance each week. The latest reading was just 210,000, below the consensus forecast. Bigger picture, this was far below the inflated figures seen during the early months of the pandemic, and in line with the levels which were typical during the solid labor market in 2019. Weekly jobless claims are important because they are one of the timeliest indicators of labor market trends. While other recent economic reports suggest that companies may be scaling back on hiring new employees, this report indicates that they remain reluctant to lay off workers.

Lower mortgage rates over the last few weeks have boosted loan origination activity. According to the Mortgage Bankers Association, applications to refinance increased 6% from last week and were a massive 152% higher than one year ago. Purchase applications rose 10% from the prior week and were up 14% from last year at this time.

Next Week

Looking ahead, attention will remain fixed on the conflict in the Middle East. The next Fed meeting will take place on Wednesday, and no change in the federal funds rate is expected. Investors will be looking for guidance about the impact of higher oil prices on future monetary policy. For economic reports, Housing Starts will come out on Wednesday. The PCE price index, the inflation indicator favored by the Fed, will be released on Thursday. First quarter Gross Domestic Product (GDP), the broadest measure of economic activity, also will come out on Thursday. The ISM national manufacturing sector index will be released on Friday.

Until next week….

*** Please note that Freddie Mac publishes their weekly rate report on Wednesday mornings from data received Monday and Tuesday.

The graph above is intended to shown rate trends, and not “today’s current rate”. ***

Reviews From Our Past Clients

With every client, we promise to provide you with a comprehensive analysis of your mortgage needs, the best service possible, and the best rates we can find. We make it our mission to have every transaction close with our clients happy with the service we provided. Browse through the hundreds of reviews we’ve received from our clients posted on both Google and Zillow.com, and read what they thought of their experience using Hawaii Mortgage Company.

Google Link:

Hawaii Mortgage Company Review on Google.com

Zillow.com Link:

Hawaii Mortgage Company Reviews on Zillow.com

Our Rate Quote System is Available to You

Our automated rate quoting system is live. Now you can check rates and try different scenarios 24-hours a day. Remember, it’s just a computer. For non-standard rate quotes, such as construction, vacant land, and other specialty programs, you’ll still need to give a call.

Here’s the link: https://www.hawaiimortgage.net/todays-rates/

Do you think all lenders are the same?

There is a difference when you use Hawaii Mortgage Company for your financing. Here’s a short video telling you why:

Broker vs. Banker?

Click the link below to get a quick lesson on why working with a Mortgage Broker will benefit you on your next transaction.