Compliments of

Alan Van Zee

Alan Van Zee

President | NMLS #: 297154

Hawaii Mortgage Company, Inc.

Company NMLS #: 232582

Alan Van Zee is one of the top producing Mortgage Originators in the state, originating over $2,000,000,000 to date. He has written and published this weekly newsletter for the past 18 years. It is the most widely read mortgage, real estate, and finance publication in Hawaii.

Hawaii Mortgage Company, now in our 26th year of providing mortgages to the people of Hawaii, is proud to have a complaint-free history. We make sure our clients are happy!

News and Insight

For the Weekend of May 23rd, 2026

Hawaii’s Most Read Mortgage, Real Estate, and Finance Publication for 18 Years

Volume 18 – Issue 34

HOA Tips and Why You’re Being Ripped Off…

I was speaking this week with a very knowledgeable Hawaii real estate agent and sharing that I lucked upon a YouTube video from a mainland real estate attorney highlighting 4 must-do tasks perspective buyers generally skip when buying a home that is part of a Homeowners Association. The conversation quickly turned to the rip off Hawaii owners face that have an HOA and property management company for their project. Let’s jump into how to avoid problems and why Hawaii owners are being taken advantage of.

HOA Must-do Task #1: Read the project’s CC&R’s prior to making an offer.

The CC&R’s refer to the covenants, conditions, and restrictions the project has placed on all units and enforced by the Homeowners Association (HOA). For condos, a very common restriction prohibits wood flooring and other hard surface flooring due to noise being transmitted to the unit below. They’ll also dictate if you can enclose your lanai or not. In some neighborhoods where single-family homes are part of an association, the CC&R’s may dictate home color, roof material type, and may require you submit plans to an architectural committee before making any changes to the exterior of your home. Some HOA’s dictate the type, height, and number of trees you can have on your property. And many have rules against impacting a neighbor’s view plane. For subdivisions with private roads, there may be a restriction about overnight parking on the street.

Let’s just wrap this up by saying that the CC&R’s will affect how you live in your home. That is why it is so important to read the project’s disclosure forms before you make an offer. You need to know if your lifestyle is compatible with the community. Why before? Because once you put in an offer on a property, you develop an emotional bond. That bond will affect your judgement when reading what you can and can’t do with your own home. You’ve found the place you love and your offer is accepted, but then find out your dream of beautiful hardwood floors is prohibited. Do you cancel or give up your dream? If you found out before the offer, that property would be easier to pass on.

And the advice of reading these documents prior to making an offer and getting into contract is where we have a problem – especially here in Hawaii. The standard Hawaii real estate contract makes provisions for the seller to provide those forms, but only once enjoined into an accepted purchase contract – and not before. It was written that way to save the seller from unnecessary expense of having to order disclosure forms from the association (some charge as much as $500 per set) until a buyer is more than an interested shopper.

And there’s the rip off. Why should an owner in any project or association be required to pay a fee for the documents they have a right to? As an owner, they’ve paid their association fees to maintain and update those documents. Somewhere along the way the associations – and the property management companies they hire to help them; forgot their role is to service the owners. Could you imagine owning a business and asking an employee to generate a report and their response is that you’ll have to pay them extra?

The good news is that not all projects and associations operate this way. Many projects have websites with all the governing documents available. Some may restrict access to owners only, but access to the documents doesn’t require a fee to obtain them. That’s why you should always ask the seller if they have access to their disclosure forms before putting in an offer. It is also a good indicator of how the project is operated too! You can always do an internet search for “(name of project) HOA disclosure forms” to check yourself.

Ripoff #2 has to do with HOA transfer fees. When you sell your home that’s part of an association the buyer will pay somewhere between $350 and $500 for a minion on a computer to update the new buyer’s name and contact information. I’ll repeat what I stated earlier. Don’t these people realize they work on behalf of the owners. I guess they find it appropriate to gouge the new owners right out of the gate.

HOA Must-do Task #2: Analyze the HOA’s Financials.

You don’t need to be an accountant or know the difference between a debit and a credit. The HOA and their professional property management company prepare reports on the finances of the project annually. Here’s a quick suggestion. Look to see how much money they have in their bank accounts. Too much, and the association may be collecting fees from owners and not using them to maintain the project. Too small of a balance may indicate the project’s board is more concerned with keeping the monthly fees low and sacrificing upkeep.

There’s also a report on the reserve fund. The reserve fund is money the project collects for future big-ticket repairs like roofs, repaving, and whole-project repainting. Some HOA boards play with the financials and underfund for these down-the-road expensive repairs. They allow themselves to enjoy lower monthly fees now - and leave it to the losers later to pay. That’s how special assessments happen.

HOA Must-do Task #3: The Condition of the Common Areas.

This one is easy, but often overlooked. So much is focused on the individual unit itself, but not enough time on how the project maintains the common elements all owners have a right to use and own a percentage of. Is there a community pool? Does the water look sparking and clear? Barbecue Grills? What condition are they in? Does the project look like it needs painting? Are the driveway and parking in need of resurfacing? Are the walkways clean or need a good pressure washing?

And for townhouse projects, how’s the grass and planting beds? What about perimeter walls and fences?

Take some time to walk through the project. Get a good sense of how well something you’ll own a portion of is being maintained.

HOA Must-do Task #4: Who’s in Charge?

Read the board minutes. Get a sense of the people elected to run the board of directors. The board minutes will list questions and complaints from other owners. Read how the board reacted to the owner and what was done. Ask yourself if that’s how you’d handle things.

Some projects are run “hard core”. Others take a more casual way of doing business. I own a unit in a condo project that has a rule that any car parked in an owner’s stall must be current with both registration and safety check. They have someone go around check each car! Some projects restrict commercial vehicles parking in owners’ parking stalls overnight – even if the vehicle is operated by an owner. The point is that how a project is run may or may not suit how you live.

In conclusion, today’s lessons are about doing your homework and about compatibility. Before you put in an offer, do your homework on the project – not only the unit within the project. The home you want may be nice, but is the project run in a way that you’re compatible with? Don’t judge a potential home by only what’s past the front door. A home tied to an HOA is so much more.

And now the week’s economic news…….

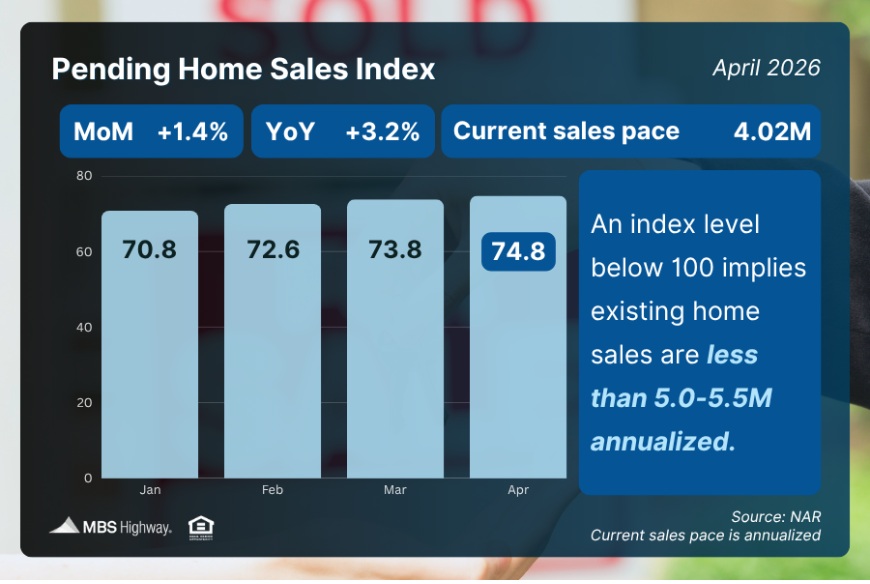

Home Sales Rise

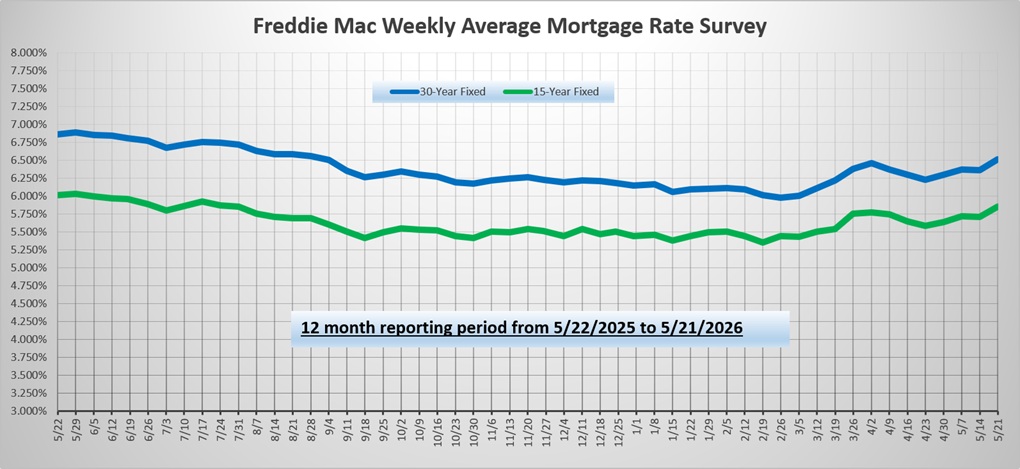

Headlines about progress to end the conflict in the Middle East continued to be the primary driver for mortgage markets, while the economic data caused little reaction. After climbing to their highest levels since July early in the week, mortgage rates reversed and ended slightly lower.

In April, sales of previously owned homes rose slightly from March, close to expectations, and were unchanged from a year ago. The median price of $417,700 was up just a slim 1% from last year at this time. Inventories remain at a near balanced level, standing at just a 4.4-month supply nationally, syncing with a balanced market of 4.6 months. However, inventories were a bit higher than a year ago.

In April, sales of previously owned homes rose slightly from March, close to expectations, and were unchanged from a year ago. The median price of $417,700 was up just a slim 1% from last year at this time. Inventories remain at a near balanced level, standing at just a 4.4-month supply nationally, syncing with a balanced market of 4.6 months. However, inventories were a bit higher than a year ago.

The latest home building data contained mixed news. In April, overall housing starts fell 3% from March, but the consensus forecast was a much larger decline. Multi-family units rose 10% from March to the highest level since May 2023, while single-family starts fell 9%. Single-family building permits, a leading indicator of future construction, dropped 3% from March to the lowest level since August.

A separate survey of home builder sentiment on housing market conditions from the NAHB unexpectedly jumped to 37, well above the consensus forecast of 34. However, it has remained in negative territory below 50 for twenty-five straight months. According to the NAHB, 61% of builders used sales incentives in May and 32% cut prices.

Higher mortgage rates in recent weeks have been negative for overall loan origination activity but have boosted demand for adjustable-rate loans that offer lower rates. According to the Mortgage Bankers Association, applications to refinance dropped slightly from last week but still were 35% higher than one year ago. Purchase applications fell 4% from the prior week and were up 8% from last year at this time. The adjustable-rate mortgage share of total applications rose to nearly 10%, the highest level since October 2025.

Next Week

Looking ahead, attention will remain fixed on the conflict in the Middle East. Investors also will monitor comments from Fed officials about future monetary policy. For economic data, Consumer Confidence will come out on Tuesday. New Home Sales, Personal Income, and the PCE price index, the inflation indicator favored by the Fed, will be released on Thursday. Mortgage markets will be closed on Monday for Memorial Day.

Until next week….

*** Please note that Freddie Mac publishes their weekly rate report on Wednesday mornings from data received Monday and Tuesday.

The graph above is intended to shown rate trends, and not “today’s current rate”. ***

Reviews From Our Past Clients

With every client, we promise to provide you with a comprehensive analysis of your mortgage needs, the best service possible, and the best rates we can find. We make it our mission to have every transaction close with our clients happy with the service we provided. Browse through the hundreds of reviews we’ve received from our clients posted on both Google and Zillow.com, and read what they thought of their experience using Hawaii Mortgage Company.

Google Link:

Hawaii Mortgage Company Review on Google.com

Zillow.com Link:

Hawaii Mortgage Company Reviews on Zillow.com

Our Rate Quote System is Available to You

Our automated rate quoting system is live. Now you can check rates and try different scenarios 24-hours a day. Remember, it’s just a computer. For non-standard rate quotes, such as construction, vacant land, and other specialty programs, you’ll still need to give a call.

Here’s the link: https://www.hawaiimortgage.net/todays-rates/

Do you think all lenders are the same?

There is a difference when you use Hawaii Mortgage Company for your financing. Here’s a short video telling you why:

Broker vs. Banker?

Click the link below to get a quick lesson on why working with a Mortgage Broker will benefit you on your next transaction.