Compliments of

Alan Van Zee

Alan Van Zee

President | NMLS #: 297154

Hawaii Mortgage Company, Inc.

Company NMLS #: 232582

Alan Van Zee is one of the top producing Mortgage Originators in the state, originating over $2,000,000,000 to date. He has written and published this weekly newsletter for the past 18 years. It is the most widely read mortgage, real estate, and finance publication in Hawaii.

Hawaii Mortgage Company, now in our 26th year of providing mortgages to the people of Hawaii, is proud to have a complaint-free history. We make sure our clients are happy!

News and Insight

For the Weekend of May 9th, 2026

Hawaii’s Most Read Mortgage, Real Estate, and Finance Publication for 18 Years

Volume 18 – Issue 32

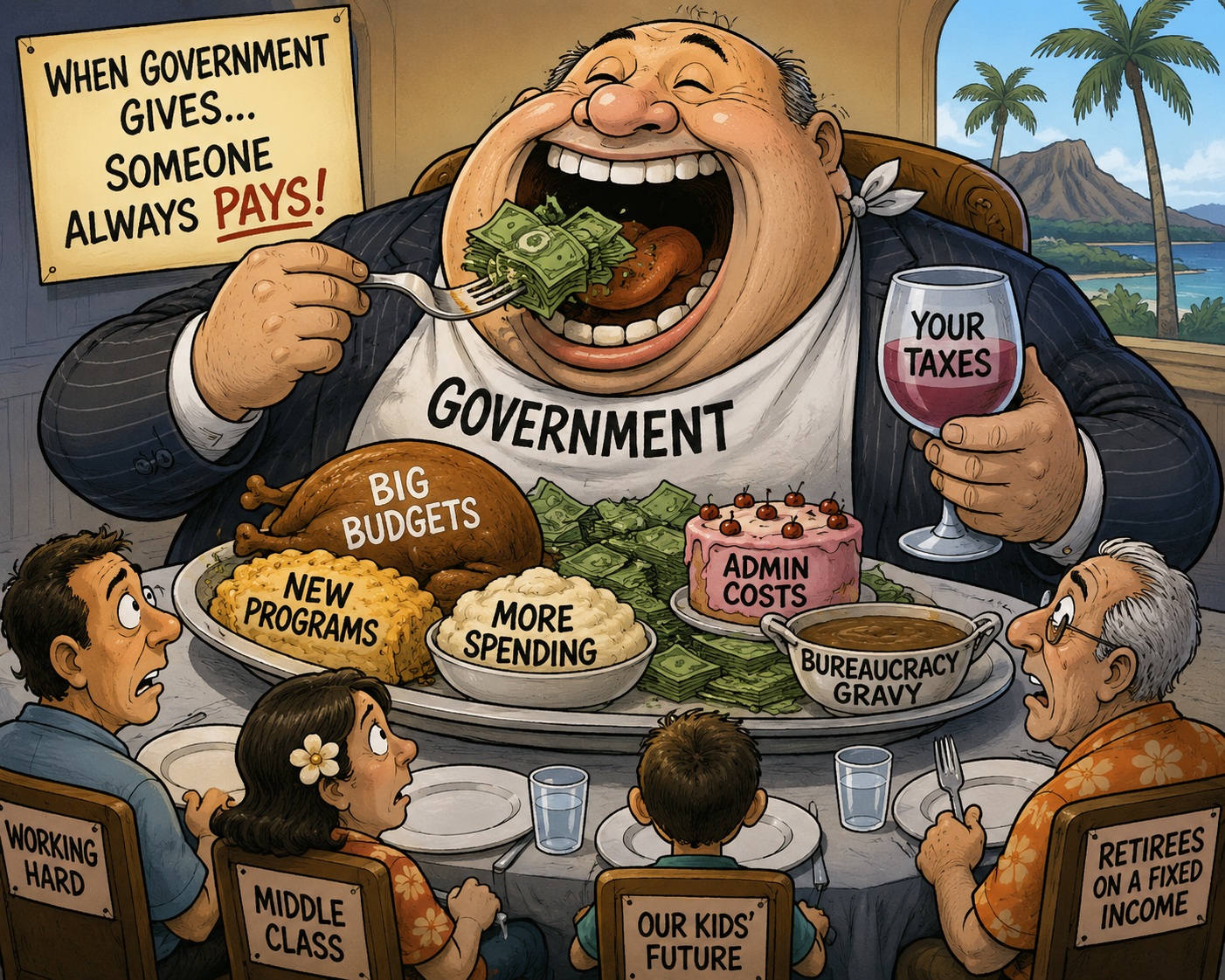

When Government Gives

My son is in the final stages of his senior-year capstone project before graduation. His project centers around affordable housing in Hawaii, or the lack thereof. We were talking about what the government can do to help the situation. That’s when I said to him “If the government gives to one segment of the population, in order to do so, they in turn, must take from another…” That’s what we’ll focus on today.

It’s a concept foreign to many in Hawaii. Our population has been indoctrinated from childhood to adult years that somehow the government will provide programs and assistance to make life better in one of the hardest places in the world to keep your head above water. But where does all that money come from for the programs and services our citizenry is constantly requesting from the government? The short answer is taxes. Hawaii doesn’t have a flat-tax system. The percentage of your income you pay in taxes is based on how much you make. The more you make, the higher percentage you pay. Government has a simple philosophy – the more you make, the more you are able to be taxed. That’s the Robin Hood theory of taking from the rich to give to the poor.

But there are many other ways the government takes from one group to give to another. A great example of this is Maui’s controversial Bill 9, passed last year, that down-zoned 7,000 condos – preventing them from being used for short-term vacation rentals. The clear goal of the legislation was to force non-resident owners to sell their property, having no longer an economic ability to keep it. Bill 9 was a subtle yet blatant way the power of government was used to take from one group and then reward a favored other group.

The state uses Hotel Room taxes and its latest Green-Fee taxes to take as much as they can from tourists without the majority saying enough and stop coming. That’s clearly taking from one group - but most Hawaii residents don’t mind. They consider these taxes as a toll for visitors to pay to enjoy our islands while on vacation.

But the real target of the government has always been the wealthy. Since there’s significantly less wealthy that those of average means, their concerns are always ignored. While most of the really ambitious ideas have failed to make it into law, our politicians keep trying. They want higher tax rates for those with high incomes, higher property taxes on homes worth more, taking a piece of your estate when you die, and wanting to take a bigger share of your home once you sell.

All these examples lead to a basic principle – government doesn’t create anything; they just take from one group to give to another. I guess the concept works well so long as you’re not in the target group being taxed. What concerns me is our ever-growing state and county budgets. At some point the state will run out of people with money to grab taxes from and are forced to come after those that can least afford it. I see no fiscal constraint by those elected to public office. The governor, state senators and representatives, every county mayor, and the county councils – all they see $$$ and never consider being fiscally responsible.

Have you looked at your property tax assessment recently? As your home increases in value so does your taxes. That’s because the counties never adjust the tax rate. With the unprecedented jump in Hawaii’s real estate values, so has the budgets for the counties. The only time our politicians look to adjust the rate we pay is after a bubble or correction when values drop. Then they look to raise the tax rate to keep their coffers full.

Today’s message is simple – don’t encourage the monster to keep eating. At some point those tasty rich people will have all been devoured, and you’re next for dinner.

And now the week’s economic news…….

Stronger Job Gains

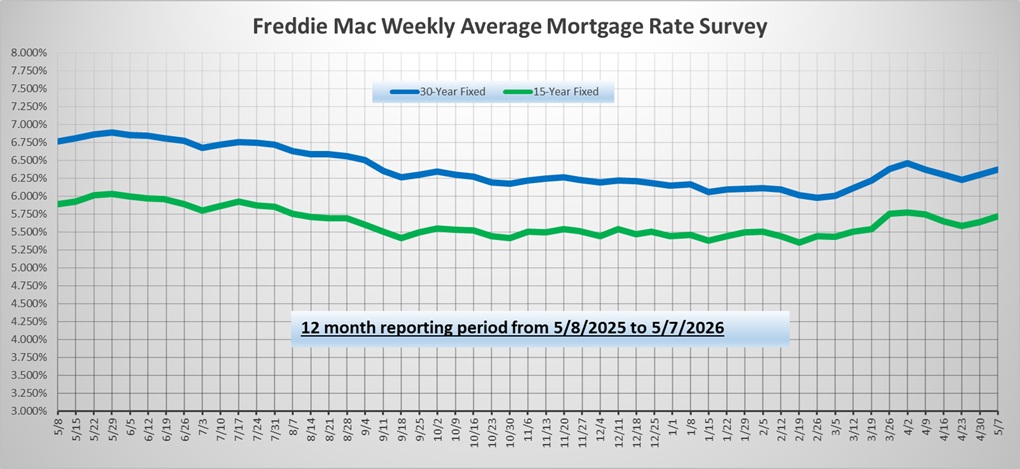

Mortgage markets continued to be volatile this week due to mixed headlines about progress to end the conflict in the Middle East. The major economic data caused little reaction, and mortgage rates ended the week slightly lower.

The conflict with Iran has been unfavorable for mortgage rates for a couple of reasons. Most significantly, oil prices have risen substantially, which greatly increases inflationary pressures. In addition, military spending has gone up, and the government may need to issue more bonds to fund the deficit. An increase in supply would cause yields to rise. However, these negative effects could be partially offset if higher energy prices lead to a reduction in global economic growth, which typically lowers the outlook for future inflation.

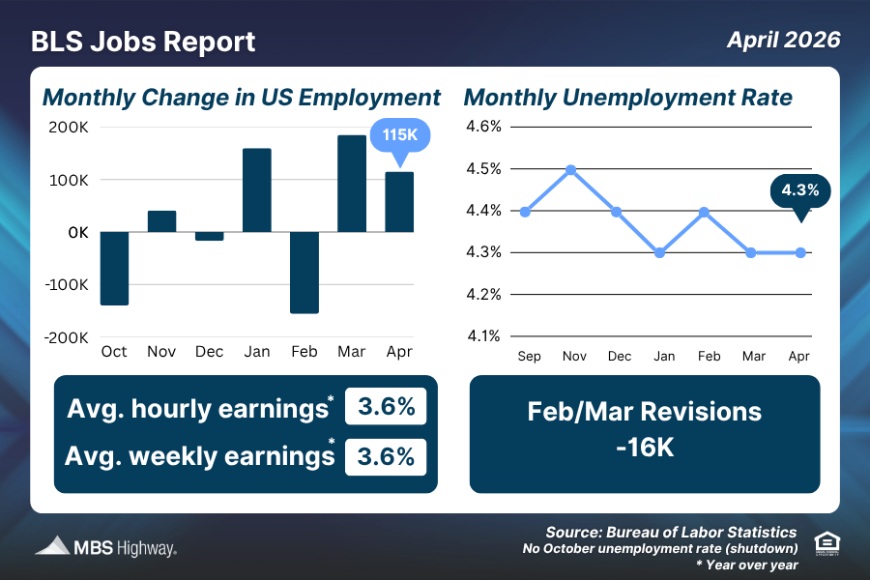

The Bureau of Labor Statistics (BLS) released their Jobs Report for April, showing that there were 115,000 jobs created, which was stronger than estimates of 62,000. Even though the headline was a beat, the internals were somewhat weak, and the BLS has lost credibility.

The Bureau of Labor Statistics (BLS) released their Jobs Report for April, showing that there were 115,000 jobs created, which was stronger than estimates of 62,000. Even though the headline was a beat, the internals were somewhat weak, and the BLS has lost credibility.

There were some revisions to the previous two months. February was revised even lower from -92,000 originally to -156,000. March was revised slightly higher by 7,000 to 185,000. The two months almost cancel each other out but are so far apart that it just underscores the BLS inconsistencies. The Birth/Death model added 391,000 jobs on a non-seasonally adjusted basis, but revisions from the BLS show that this is significantly overstating job growth. Most of the jobs continue to come from Health Care and Social Assistance, which is a sign of an aging economy, but not necessarily a very strong jobs market.

The Household Survey, where the unemployment rate comes from, had a lot of weakness. There were 226,000 job losses, yet the unemployment rate remained at 4.3%, because 92,000 people left the labor force. The unemployment rate did go up by 0.08%, but on a rounded basis, remained at 4.3%. This is the fourth month in a row that there were job losses within the Household Survey. Since the start of the year, there have been 1.4 million job losses, but the unemployment rate is right where it started the year, at 4.3%. The reason is that 1.5M people have left the labor force. The unemployment rate remains low, but for the wrong reasons.

There are also a lot of people not counted within the quoted U-3 unemployment rate, such as those who are discouraged, marginally attached, or work part time for economic reasons, etc. The U-6 unemployment rate rose from 8% to 8.2% and adds all of those people back into the calculation. The report showed that 424,000 full-time jobs were lost, while 123,000 part-time jobs were gained, not a sign of a strong labor market.

Two other significant economic reports from the Institute of Supply Management remained relatively strong but fell a bit short of expectations. The ISM national services sector index declined to 53.6, below the consensus forecast of 54.0, while the ISM national manufacturing sector index was flat at 52.7, below the consensus forecast of 53.0. Readings above 50 indicate an expansion in the sectors. While tariff policies have been in flux since the Supreme Court decision in February, the higher tariffs on foreign goods put in place last year may be helping domestic manufacturing companies close the performance gap over the last few years with service firms.

Next Week

Looking ahead, attention will remain fixed on the conflict in the Middle East. Investors also will monitor comments from Fed officials about future monetary policy. For economic data, Existing Home Sales will come out on Monday. The Consumer Price Index (CPI), a widely followed monthly inflation indicator that looks at the price changes for a broad range of goods and services, will be released on Tuesday. The Producer Price Index (PPI), another monthly inflation indicator, will come out on Wednesday. Import Prices and Retail Sales will be released on Thursday. Since consumer spending accounts for over two-thirds of U.S. economic activity, the retail sales data is a key measure of the health of the economy.

Until next week….

*** Please note that Freddie Mac publishes their weekly rate report on Wednesday mornings from data received Monday and Tuesday.

The graph above is intended to shown rate trends, and not “today’s current rate”. ***

Reviews From Our Past Clients

With every client, we promise to provide you with a comprehensive analysis of your mortgage needs, the best service possible, and the best rates we can find. We make it our mission to have every transaction close with our clients happy with the service we provided. Browse through the hundreds of reviews we’ve received from our clients posted on both Google and Zillow.com, and read what they thought of their experience using Hawaii Mortgage Company.

Google Link:

Hawaii Mortgage Company Review on Google.com

Zillow.com Link:

Hawaii Mortgage Company Reviews on Zillow.com

Our Rate Quote System is Available to You

Our automated rate quoting system is live. Now you can check rates and try different scenarios 24-hours a day. Remember, it’s just a computer. For non-standard rate quotes, such as construction, vacant land, and other specialty programs, you’ll still need to give a call.

Here’s the link: https://www.hawaiimortgage.net/todays-rates/

Do you think all lenders are the same?

There is a difference when you use Hawaii Mortgage Company for your financing. Here’s a short video telling you why:

Broker vs. Banker?

Click the link below to get a quick lesson on why working with a Mortgage Broker will benefit you on your next transaction.