Compliments of

Alan Van Zee

Alan Van Zee

President | NMLS #: 297154

Hawaii Mortgage Company, Inc.

Company NMLS #: 232582

Alan Van Zee is one of the top producing Mortgage Originators in the state, originating over $2,000,000,000 to date. He has written and published this weekly newsletter for the past 18 years. It is the most widely read mortgage, real estate, and finance publication in Hawaii.

Hawaii Mortgage Company, now in our 26th year of providing mortgages to the people of Hawaii, is proud to have a complaint-free history. We make sure our clients are happy!

News and Insight

For the Weekend of November 15th, 2025

Hawaii’s Most Read Mortgage, Real Estate, and Finance Publication for 18 Years

Volume 18 – Issue 10

Affordability

I’ve written extensively that the generations entering the housing market to purchase their first home simply cannot. Home prices have spiked across the country – and it’s no more evident than here in Hawaii. There’s been lots of talk this week about how to make housing more affordable. Let’s dive into the issue and discuss the solutions proposed.

The issue of unaffordable housing is easy to understand and for some reason beyond my pay grade to understand why it can’t be easily fixed. The problem is a lack of entry level homes for new family formations to buy. An entry level home would be in the $300,000 range. I complained openly that here in Hawaii the government and developers think a $700,000 home is affordable – which is plain stupid. Nationally we need 10-million new entry level homes. Developers make more money by building bigger, more expensive homes, so they skip building cheap ones.

Every economic issue follows the rules of supply and demand. The issue of affordable housing is a supply-side issue. The demand for affordable housing is high, yet supply is woefully inadequate. That puts pressure on home prices to continue to rise. If the supply were to increase, especially for entry level homes, that pressure for rising home prices would be reduced.

A lot of the discussion this week failed to address the cycle of real estate ownership. Especially with the proposal for a 50-Year mortgage and the huge blowback it received. None of the smart people I read or heard from this week understand that rarely does someone buy a starter home and live in that home until they die. Typically, a young couple or an unmarried single person will buy a small starter home. As marriage and children come, they logically outgrow that smaller home and need to upgrade. For some, financial success will allow that family to next upgrade to a bigger home in a nicer neighborhood. After the kids have left home, many couples will downsize – usually a condo where the maintenance is taken care of by the HOA.

Right now, with a lack of starter homes, those young family formations can’t get on the homeownership escalator. Without those families already in homes and needing to trade up, the families next on the rung can’t sell their home to buy the next home on their journey. The issues continue for the next steps too. It is all interconnected and it all starts with a lack of starter homes. And if you’re concerned that building all those new starter homes will crash the real estate market due to over-supply, it won’t. Each category of home type – starter, mid-level, luxury, and condo, has their own supply and demand components. Increasing the supply of starter homes will not affect the prices of the other types of homes available for sale.

Until the issue of the lack of supply is addressed, home prices will continue to rise – period.

President Trump’s Director at the Federal Housing and Finance Agency (FHFA) Bill Pulte, has floated some ideas that have drawn some sharp criticism. Frankly I’m shocked that the negative comments came not only from Gen Z, but from seasoned economists. While these proposals don’t address supply issues, which will take some time to cure, FHFA the government agency that runs Fannie Mae and Freddie Mac can’t build homes – they finance them. Their proposals are an attempt to help families today. While some of the proposals I like and some won’t work, I applaud anyone in government that is thinking outside the box.

The 50-Year Mortgage:

This is the proposal that got most of the press this week. Most Gen Z critics slammed the proposal as a government conspiracy to indenture people to owe the government for the rest of their life. 50 years? If someone where to obtain 50-year loan while in their late 20’s, they’d be past their retirement and still owe on their home. Wrong!

No one obtains a mortgage today and makes all their 360 scheduled payments on a 30-year loan. People don’t. The average lifespan of today’s 30-Year mortgage in just under 10 years. People don’t keep their mortgage for the entire life of the loan for various reasons. I noted the cycle of owning real estate earlier. Another reason is the cycle of interest rates. If you refinance to obtain a lower rate, that original loan goes away. Many also choose to tap into the equity they have earned and obtain a cash-out refinance. Again, that original mortgage is paid off and gone.

The idea of a 50-Year Mortgage is to allow for smaller payments and thus qualify for a higher priced home. This financing option does nothing to address the crazy prices of real estate today. The critics talk about the significant increase in total interest paid on a 50-Year mortgage versus a 30-Year mortgage, but again, no one will keep this loan for 50 years!

I feel the 50-Year Mortgage is a great mortgage product to allow first-time homebuyers the opportunity to reduce their monthly payment and qualify for more home. I’ll go one step further. Why not allow first-time homebuyers to utilize interest-only mortgage products? If the plan is to obtain the lowest payment, knowing that original mortgage is not permanent, why not offer it?

Study after study show that the bulk of the equity you earn in the first 10 years of homeownership comes from appreciation – not from paying down your mortgage. Equity gains are important because that family will need the increase in equity when they want to upgrade to a new home later in life.

The Portable Mortgage:

One of the causes of our sluggish real estate sales volume is families feeling locked into their current home because of the significantly lower interest rate mortgage they obtained when rates were at historic lows. This has broken the natural cycle of homeownership with people staying in their current home instead of selling and moving on. Who would want to give up a 2.875% mortgage rate to buy a new home with a mortgage rate just north of 6.000%?

That’s the idea of the portable mortgage. The idea is that you can sell and keep the financing you have in place now to use when buying a new home. When you sell your home, the mortgage you have with the great rate is used as the financing to purchase the new property. Portable mortgages are common in other countries such as Canada.

The issue with the US mortgage market adopting the portable mortgage is how mortgages are funded in the US. We have what’s called a secondary market. The ultimate source of the money you get when obtaining a mortgage is rarely from the lending institution you applied with. Upon funding your transaction, the lender will sell your mortgage that eventually becomes part of a bond offering. Because mortgages are what’s called securitized, it would seem difficult to change the parameters of what the bond buyers purchased.

Remember this point from earlier on in my article: The average mortgage is held for just under 10 years. That’s an important fact for bond traders buying mortgage-backed securities. The interest rate the bond buyers agree to fund your mortgage is based on inflation projections for that average 10-year lifespan of the mortgage. If portable mortgages were to become a reality, and people held those loans for significantly longer periods, bond buyers would need to factor in longer periods of inflation. That would result in higher mortgage rates. Inflation over time erodes the underlying value of a bond. The more inflation there is while holding a bond, the less it is worth.

Again, the solution is to build more entry level homes to purchase - not rentals. Build homes Gen Z can purchase to start building a life and family. But building is not enough. Offering some creative financing would significantly help too.

And now the week’s economic news…….

Shutdown Ends

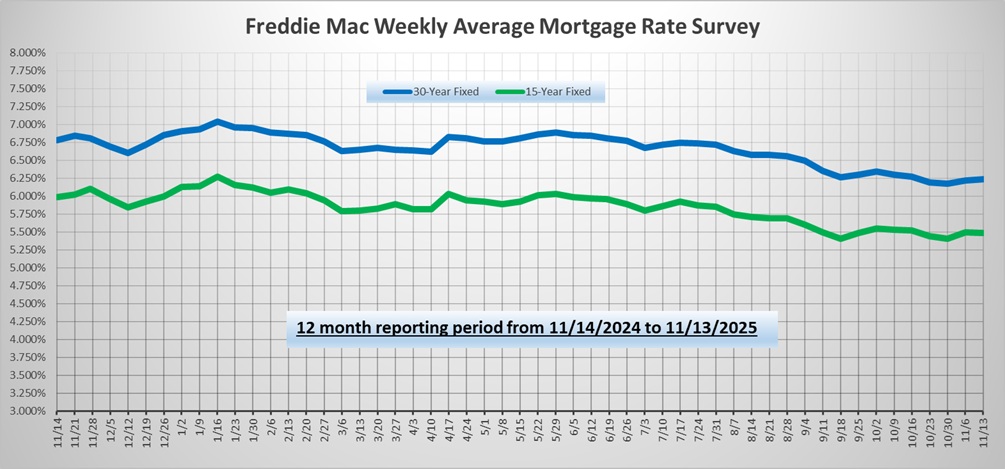

Mortgage markets were relatively quiet over the past week. No major economic data was released, and the end of the government shutdown caused little reaction. As a result, mortgage rates ended the week nearly unchanged.

After a record 43 days, the government shutdown ended on Wednesday. With the exception of one Consumer Price Index inflation report, no government economic data was released during this period. It is expected that government agencies will soon announce the schedule for delayed reports based on how quickly data collection can catch up. A White House official said that missed key labor market and inflation reports for October may never come out. In addition, there may be questions about the accuracy of some of the data for a couple of months.

As difficult as the data blackout period has been for investors, Fed officials have struggled under even more pressure to navigate during the past six weeks. As Chair Powell made clear at the last Fed meeting, officials are divided about how to proceed. Signs of weakness in the labor market support additional loosening of monetary policy, but stubbornly elevated inflation levels since tariffs increased favor holding steady. Attempting to prioritize these conflicting goals is difficult under any circumstances - but doing it while flying blind with extremely limited economic data is extremely challenging, to say the least. As a result, investors are nearly evenly split about whether the Fed will reduce the federal funds rate by another 25 basis points at the next meeting in December.

Investors continue to look for alternative information from private companies. One report receiving attention this week revealed disappointing news about the labor market and the important holiday shopping season. According to Indeed Hiring Lab, retail-related job postings declined 16% in October from last year at this time. This typically reflects the consumer demand anticipated by retailers, which may be depressed this year due to the impact of higher tariffs and the government shutdown. According to several large retailers, another factor behind the reduced hiring needs is that fewer employees are voluntarily quitting their jobs, likely due to greater uncertainty about their prospects of finding better opportunities at another company.

Next Week

Looking ahead, investors will continue to watch for additional information about tariffs and monitor comments from Fed officials for hints about monetary policy later in the year. With the end of the government shutdown, investors will be waiting for the schedule for the release of government economic reports. The detailed minutes from the October 29 Fed meeting will be released on Wednesday. Existing Home Sales will come out on Thursday.

Until next week….

*** Please note that Freddie Mac publishes their weekly rate report on Wednesday mornings from data received Monday and Tuesday.

The graph above is intended to shown rate trends, and not “today’s current rate”. ***

Reviews From Our Past Clients

With every client, we promise to provide you with a comprehensive analysis of your mortgage needs, the best service possible, and the best rates we can find. We make it our mission to have every transaction close with our clients happy with the service we provided. Browse through the hundreds of reviews we’ve received from our clients posted on both Google and Zillow.com, and read what they thought of their experience using Hawaii Mortgage Company.

Google Link:

Hawaii Mortgage Company Review on Google.com

Zillow.com Link:

Hawaii Mortgage Company Reviews on Zillow.com

Our Rate Quote System is Available to You

Our automated rate quoting system is live. Now you can check rates and try different scenarios 24-hours a day. Remember, it’s just a computer. For non-standard rate quotes, such as construction, vacant land, and other specialty programs, you’ll still need to give a call.

Here’s the link: https://www.hawaiimortgage.net/todays-rates/

Do you think all lenders are the same?

There is a difference when you use Hawaii Mortgage Company for your financing. Here’s a short video telling you why:

Broker vs. Banker?

Click the link below to get a quick lesson on why working with a Mortgage Broker will benefit you on your next transaction.