Compliments of

Alan Van Zee

Alan Van Zee

President | NMLS #: 297154

Hawaii Mortgage Company, Inc.

Company NMLS #: 232582

Alan Van Zee is one of the top producing Mortgage Originators in the state, originating over $2,000,000,000 to date. He has written and published this weekly newsletter for the past 17 years. It is the most widely read mortgage publication in Hawaii.

Hawaii Mortgage Company, now in our 25th year of providing mortgages to the people of Hawaii, is proud to have a complaint-free history. We make sure our clients are happy!

Mortgage Market News and Insight

For the Weekend of March 22nd, 2025

Hawaii’s Most Read Mortgage Publication for 17 Years

Volume 17 – Issue 27

Moving and Buying a Home Before Starting That New Job

This week let’s look at an issue for anyone moving to Hawaii, or for the growing number of people leaving Hawaii for less expensive options. In the past, a borrower was required to be working in their new location and present pay stubs to close on a home loan. The good news is that there are now options to fix this dilemma.

It has always been an issue for those moving to a new locale to figure out how to avoid renting, instead of finding a place to purchase prior to moving and starting that new job. The first few months

of a move and new employment should not be layered with seeking a home to buy, while still having personal items stored and living in a rental. Today we’ll go over how to accomplish this feat.

The issue in the past was that lenders required a borrower to have started their new job and present pay stubs with a minimum of 30 days of pay prior to closing. I recently had clients that faced this situation wishing to move from Utah to Hawaii. Stewart and Leslie contacted me months before any final decision was made on the move to Hawaii. They wanted to see if they could first find a home they liked and could afford, then start work, all while trying to sell the mainland home they currently lived in. Here’s how we did it.

Pre-Qualification:

Stewart is a talented guy and was looking at several job offers. All were close in pay. Once I knew what his Hawaii income was going to be, I pulled that figure into their application. I presented Stewart and Leslie with various loan program options for qualification, along with the amount they would qualify for. They then started looking at properties that matched what they would qualify for. Once they realized that they could find something here that they liked and could see themselves living in, they asked me to make it happen.

The Job:

Stewart got a job offer from a local business on Oahu. The business formally issued a written offer of employment. The key part of the written offer was that the letter did not contain any stipulations or conditions for employment. The letter clearly listed his income. The letter also provided a start date. And another important distinction – the offer could not come from a company owned by a family member.

With Stewart’s job offer in hand, we were allowed to close his loan using that income. The stipulation being that his start date must happen before the 90th day from the date the purchase transaction closed. In order to get such lenient terms, the borrower(s) are required to have 6 months of the full mortgage payment PITIA (principal, interest, taxes, insurance, and HOA) in reserves. Leslie has a 401(k) that meets that requirement.

The Down Payment:

Stewart and Leslie ran into a funds issue for their down payment. They had always counted on using the equity in their mainland home for their new home here. They spent years paying down the balance on that home and certainly didn’t want a huge mortgage payment as a penalty for moving to Hawaii.

My suggestion was that they get a mortgage with a 5% down payment. They believed their house on the mainland would sell quickly. Once that home sells, they would apply the equity to the new mortgage here.

Here a trick a lot of people are unaware of. It’s called RECASTING.

Recasting is a method of applying a reduction in principal loan that is different than just applying that to the existing balance. Normally when you make additional payments to principal the payment remains the same, but with a lower balance, the remaining number of payments is reduced – you pay the loan off early. Recasting is a process where the reduced principal balance is amortized over the remaining payments. The result is a lower payment, but the number of payments remaining stays the same. Not every lender/servicer allows for recasting, so check first. There is a recasting fee. It’s typically about $350. Also, there’s no requalification, appraisal, or escrow/title fee. The payment reduction is done internally by the mortgage servicer.

Stewart and Leslie bought their new home here. Stewart and Leslie were able to ship their items and fly here move into their home. Stewart then started his new job. They sold their mainland home in just under 60 days. The net equity from that sale was applied to their new loan. That immediately reduced their payments going forward.

I was happy I could make this happen for them. My bonus is that when rates ease some, I’ll help them with their refinance. Clients for life!

Use the story above to make your dream move a reality. If you want more information and questions answered on your specific situation, give me a call.

Quick Thoughts

As I report below in the news section, the Fed this week did decide to start using the money from maturing bonds to buy more US 10-Year Notes. Starting in April the Fed will buy $20-Billion of 10-Year Notes per month. That added demand will help bring down the interest rate for the 10-Year, and in turn mortgage bonds will benefit. If you have no idea what I just wrote, look back at last week’s newsletter on the plans Treasury Secretary Scott Bessent has to bring interest rates down and rejuvenate the housing sector.

On another note, are you concerned about the health of Hawaii’s citizens? I’m not sure if I’m the only one to notice, but despite Hawaii allowing cannabis for medical uses only, I now smell people smoking it everywhere. I’m amazed that even when in my air-conditioned car driving I sometimes encounter what I can best describe as being reminiscent of late nights in my early 20’s at Anna Bananas on Beretania Street. Either we have a large population needing the medical benefits of smoking pot, or we have a growing population of skunks hiding on Oahu. I don’t think pot smelled as pungent a few decades ago. I can’t accept that it’s just me getting older.

And don’t look now, but UH researchers have now focused on Hawaii sinking along with sea level rise. As our islands move on the geologic plate away from the hotspot that created us, our islands are staring to subside – sink. I am sure none of us will be here when Hawaii starts to resemble Venice. The good news is that we already have the canoes.

And now the week’s economic news…….

Favorable Fed Meeting

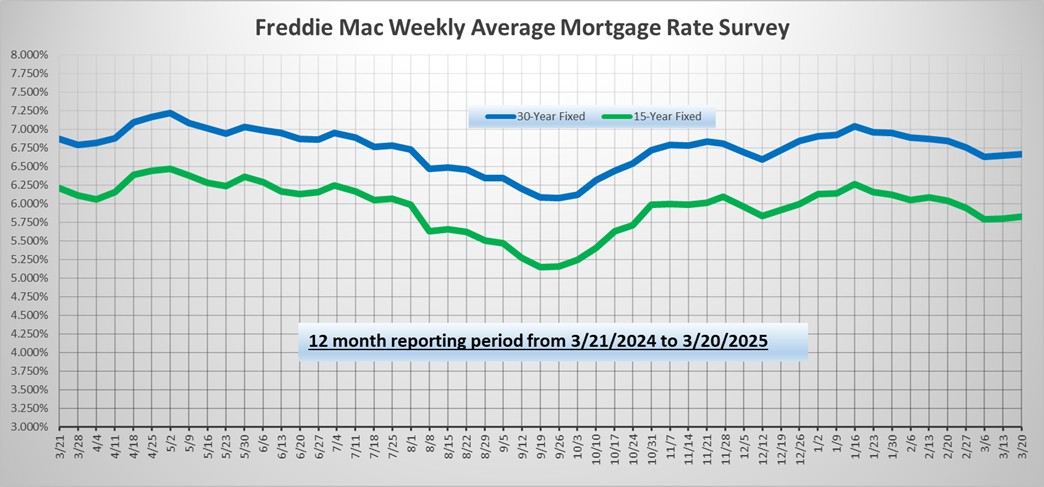

While there were no major surprises, the Fed meeting was modestly favorable for mortgage markets overall. The biggest economic report released this week revealed that consumer spending was close to expectations and had little impact. As a result, mortgage rates ended the week lower.

As expected, the Fed left the federal funds rate unchanged at a target range of 4.25% to 4.50% on Wednesday. The meeting statement made clear that the current level of uncertainty is "unusually elevated," and officials will wait to see the impact of government policy changes to determine adjustments to monetary policy. The "dot plot" projections from Fed officials for future rate cuts were similar to their last set of dot plots released three months ago, with forecasts for two additional 25 basis point rate cuts in 2025 and two more in 2026. In addition, the Fed will slow the reduction in its holdings of Treasuries on its balance sheet, while keeping the same pace for mortgage-backed securities. Officials also raised their outlook for core inflation in 2025, but they still forecast hitting their annual target of 2.0% in 2027. Bond investors were pleased that the rate cuts remain on track despite the higher inflation forecast and that the Fed will retain more bonds each month.

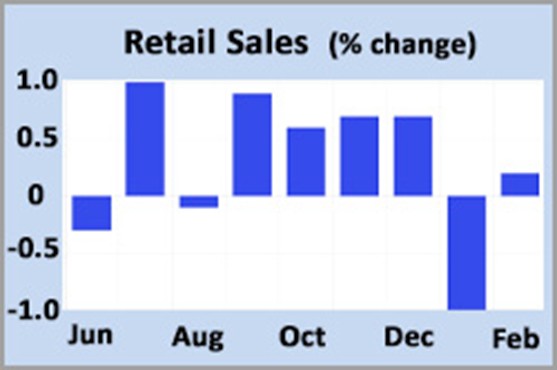

After unexpectedly slowing in January, consumer spending rebounded in February. Retail sales rose 0.2% from January and were 3.1% higher than a year ago. Strength was seen in personal care and online outlets, while bars and restaurants lagged. Going forward, investors are wondering if consumers may scale back on purchases due to uncertainty about the economy and tariffs.

After unexpectedly slowing in January, consumer spending rebounded in February. Retail sales rose 0.2% from January and were 3.1% higher than a year ago. Strength was seen in personal care and online outlets, while bars and restaurants lagged. Going forward, investors are wondering if consumers may scale back on purchases due to uncertainty about the economy and tariffs.

In the past, a monthly report on import prices from the Bureau of Labor Statistics has generally not received much attention, but investors are keeping a closer eye on it now with tariffs in the spotlight. Import Prices in February, expected to be roughly flat from January, instead climbed 0.4%, boosted by higher costs for consumer goods. This is important because import prices are measured before any tariffs are imposed. One big question is whether exporters in other countries will lower their prices to at least partially offset higher tariffs or whether U.S. households and businesses will absorb the costs.

Next Week

Investors will continue to watch for additional information about tariff policies. For economic reports, New Home Sales and Consumer Confidence will come out on Tuesday. Personal Income and the PCE price index, the inflation indicator favored by the Fed, will be released on Friday.

Until next week….

*** Please note that Freddie Mac publishes their weekly rate report on Wednesday mornings from data received Monday and Tuesday.

The graph above is intended to shown rate trends, and not “today’s current rate”. ***

Reviews From Our Past Clients

With every client, we promise to provide you with a comprehensive analysis of your mortgage needs, the best service possible, and the best rates we can find. We make it our mission to have every transaction close with our clients happy with the service we provided. Browse through the hundreds of reviews we’ve received from our clients posted on both Google and Zillow.com, and read what they thought of their experience using Hawaii Mortgage Company.

Google Link:

Hawaii Mortgage Company Review on Google.com

Zillow.com Link:

Hawaii Mortgage Company Reviews on Zillow.com

Our Rate Quote System is Available to You

Our automated rate quoting system is live. Now you can check rates and try different scenarios 24-hours a day. Remember, it’s just a computer. For non-standard rate quotes, such as construction, vacant land, and other specialty programs, you’ll still need to give a call.

Here’s the link: https://www.hawaiimortgage.net/todays-rates/

Do you think all lenders are the same?

There is a difference when you use Hawaii Mortgage Company for your financing. Here’s a short video telling you why:

Broker vs. Banker?

Click the link below to get a quick lesson on why working with a Mortgage Broker will benefit you on your next transaction.