Compliments of

Alan Van Zee

Alan Van Zee

President | NMLS #: 297154

Hawaii Mortgage Company, Inc.

Company NMLS #: 232582

Alan Van Zee is one of the top producing Mortgage Originators in the state, originating over $2,000,000,000 to date. He has written and published this weekly newsletter for the past 17 years. It is the most widely read mortgage publication in Hawaii.

Hawaii Mortgage Company, now in our 25th year of providing mortgages to the people of Hawaii, is proud to have a complaint-free history. We make sure our clients are happy!

Mortgage Market News and Insight

For the Weekend of May 24th, 2025

Hawaii’s Most Read Mortgage Publication for 17 Years

Volume 17 – Issue 36

AI Loan Officer?

The largest mortgage lender in the country in 2024 was United Wholesale Mortgage (UWM). They narrowly beat second place Rocket Mortgage by closing 5006 more loans. That’s close! UWM focuses on business generated by independent mortgage brokers. Data from 2024 shows that 65.2% of all residential mortgages originated from sources other than banks.

Part of UWM’s success has been constant reinvestment into technology. Our company no longer brokers loans to UWM. While they do have great technology, my personal experience has been that with all that money dedicated to technology, they cut corners with the people they hire. When an issue came up it was impossible to get a human to address things. That’s why I tell my clients that dealing with the humans at many of these large national lenders is like dealing with minions. They just do their job and don’t have the role or responsibility to make decisions.

Part of UWM’s success has been constant reinvestment into technology. Our company no longer brokers loans to UWM. While they do have great technology, my personal experience has been that with all that money dedicated to technology, they cut corners with the people they hire. When an issue came up it was impossible to get a human to address things. That’s why I tell my clients that dealing with the humans at many of these large national lenders is like dealing with minions. They just do their job and don’t have the role or responsibility to make decisions.

I read a news release this week that UWM is launching an AI assistant to help mortgage brokers become more efficient. After I read what the AI is supposed to do, I wasn’t sure if you, the public, would be happy interfacing with AI. I’d be interested in your thoughts.

UWM calls their system MIA, a virtual loan officer assistant focused on client engagement. MIA can be customized with a brokers’ branding and is designed to make calls, send messages, schedule appointments and collect callback information. MIA also reminds clients about upcoming payments 20 days after their loan closes. It also regularly checks in with past borrowers, notifying them when interest rates drop and they become eligible for refinancing.

How would you feel getting an AI generate call during your mortgage transaction, or a virtual assistant soliciting you months down the road?

I’m not sure why my brain works the way it does but more often than not when I reconnect with a former client I can recall many aspects of their application – such as remembering what they do for a living or that they were helping one of their kids with the loan. One of the parts of my job that has kept me doing this for almost three decades now is human interaction with my clients.

I believe this AI approach minimizes you, the borrower-client, as a commodity. But what do you the consumer want? Do you want to do away with the human interaction of getting a mortgage? For many, maybe human interaction isn’t necessary? Too many feel it all comes down to rate and fees. In my business I look at a mortgage as a tool to meet your financial goals. To do that I need to interact with my clients to determine which mortgage product best fits their needs. I haven’t seen it yet, but maybe the AI is now smart enough to replace me too. I also take pride in personally reviewing the loans of my past clients and analyzing each one to see if they could benefit from current rates. I don’t think having AI do that, then make a call on my behalf, shows the same level of care and respect. At that point for me, it’s an automated sales call.

Here's another way I look at it, and this thought makes me feel old. Prior to us all having a computer in our hands I took great pleasure in receiving birthday wishes from my friends. If they remembered my day with a note or call, it showed that the friend truly cared – cared enough to remember my birthday. Today, your phone will remind you of who to reach out to. It just isn’t the same level caring in my opinion. Getting birthday greetings on Facebook was at first quite an experience. Woohoo, I got 156 wishes one year, I remember. I thought that was something really special. But in reality, the effort was minimal, and although the thought nice, was probably one task of many that social media friend did that day.

I’d be interested in your feedback. If you do respond, let me know your thoughts, along with your age, and if you plan in the next few years to purchase or refinance. I am asking for additional information to see if age has anything to do with acceptance of AI driven interactions. I will also put greater weight on those that will get another mortgage in the near future. I will not use your responses to solicit you!

Listing Agent Conundrum

You decide to list your house for sale. You’ve done some research and decided to interview 3 real estate agents, one of which you will give the listing to. You met each agent in person and heard what they had to say. How do you choose the right agent?

Let’s back up. What did you do to prepare yourself for the meeting? Other than realizing that going with an agent that’s a friend or a recommendation from a friend may not be the best choice, what else have you done?

Did you look around your home to see what may need to be fixed prior to selling? Every home has little things we never got around to addressing and end up just living with them. Things like cracked and faded paint, a wobbly handrail, a missing electrical faceplate, a dirty driveway, and hundreds of other possible deficiencies.

Did you give your home an honest evaluation if it’s dated and would need someone to come in and spend some money to modernize what’s there?

Did you do some research to get an idea of what your home may sell for, to determine in your mind what you would list the property for?

You’ll hear agents tell you there aren’t a lot of homes available right now. In reality there are many homes listed for sale in Hawaii. The ones that have been listed for a while are like that for one of two reasons. Either the home needs lots of work or the home is priced too high. If you have a clean home that is priced fairly, it will sell quickly.

Too many homeowners wishing to list their home have either an unrealistic idea of their home’s true sale price potential or are unwilling to correct deficiencies that will scare off most potential buyers.

Those people are the listing agent’s conundrum. Agents need listings, and in order to secure the listing, too many agents will go along with what the seller wants. They know that if they tell the homeowner they’re too high on their price expectation, or that they’ll need to spend some money to sell the place, they won’t get the listing. But this approach will almost always end badly for all involved, because the homeowner will always blame their agent if the property sits.

As a homeowner, you should want to hear the frank unvarnished opinions of a professional you are considering hiring. You need to listen to what these professionals say about your home and how it will fare in the current marketplace. If you’ve done your homework, you can ask pointed questions and together come up with not only a competitive listing price but a plan of action to make any necessary repairs prior to listing.

I work with a lot of real estate agents and hear a lot of feedback. They would all prefer the homeowner to come to the listing meeting with some homework done and ready to ask lots of questions. The best part? You’ll end up with less days on the market and a higher price.

And now the week’s economic news…….

The Spending Bill

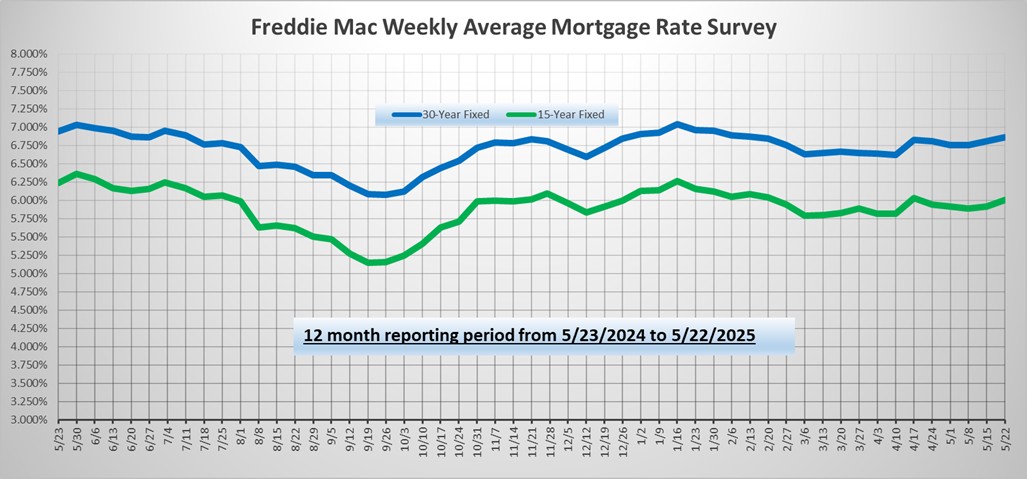

Despite a lack of major economic reports, it was another volatile week for mortgage markets. Investors reacted daily to the latest news about the proposed government spending bill, until tariffs reclaimed the spotlight on Friday. The net result, though, was that mortgage rates ended the week just slightly higher.

The focus of investors continues to shift rapidly. Last month, higher tariffs and a trade war appeared likely to slow economic growth, reducing future inflationary pressures, which would be good for mortgage rates. However, easing trade tensions with China and other countries had reduced those worries in recent weeks, and attention turned to the new government spending bill. Investors anticipate that proposed tax cuts could add trillions of dollars to the deficit and boost economic growth, both of which would be negative for mortgage markets. The government finances its deficit by issuing bonds and yields generally must rise to entice investors to purchase larger quantities. The latest abrupt shift for investors took place on Friday morning when President Trump recommended raising tariffs on the European Union to 50% beginning June 1 due to a lack of progress on negotiating trade deals.

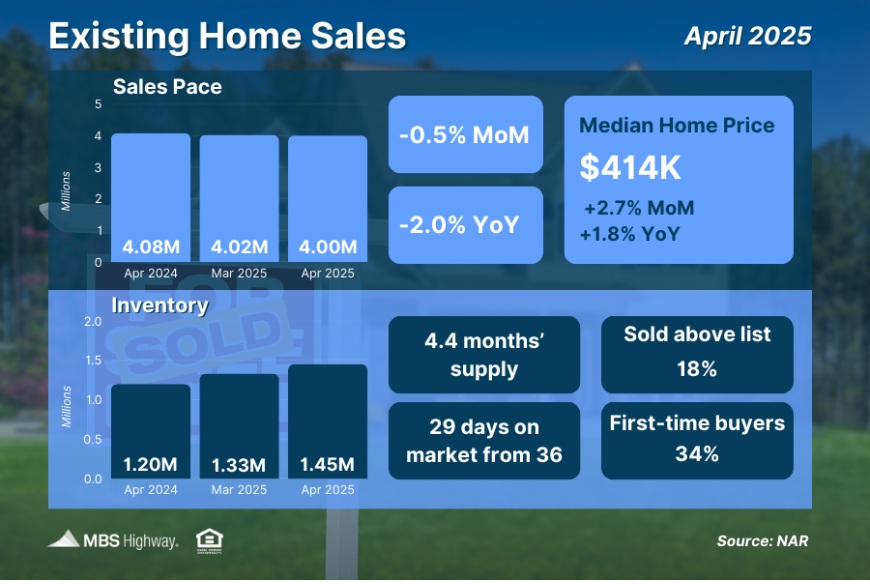

In April, sales of existing homes fell slightly from March, weaker than the consensus forecast, to the slowest pace in April since 2009. The median existing-home price of $414,000 was up 2% from last year at this time, at a record for the month of April. Inventories remain stuck at historically low levels, standing at just a 4.4-month supply nationally, below the 4.6-month supply typical in a balanced market. However, this was the largest level in five years, and inventories were 20% higher than a year ago.

In April, sales of existing homes fell slightly from March, weaker than the consensus forecast, to the slowest pace in April since 2009. The median existing-home price of $414,000 was up 2% from last year at this time, at a record for the month of April. Inventories remain stuck at historically low levels, standing at just a 4.4-month supply nationally, below the 4.6-month supply typical in a balanced market. However, this was the largest level in five years, and inventories were 20% higher than a year ago.

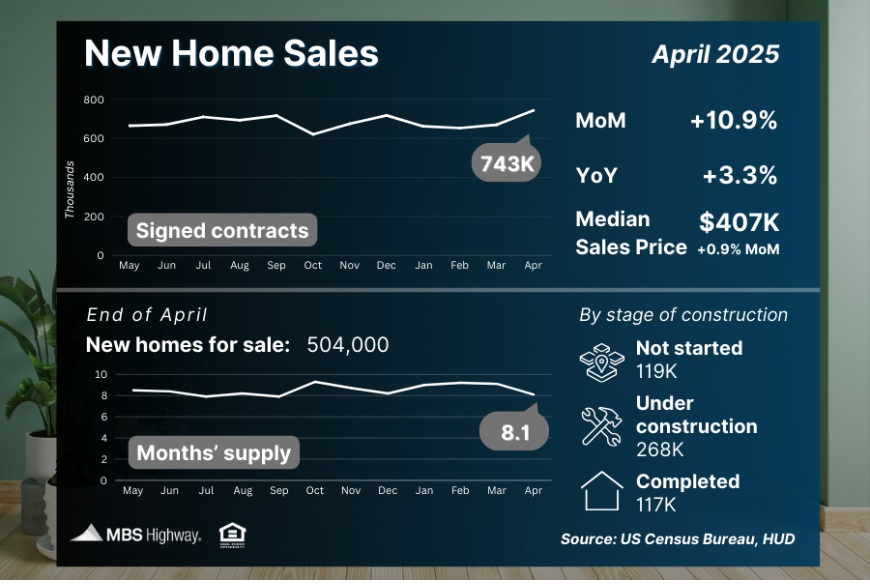

Sales of new homes displayed much better performance in April, rising 11% from March, far above the consensus forecast. New home sales were 3% higher than a year ago. The median new-home price of $407,200 was down 2% from last year at this time. The supply of new homes remains near the highest level since 2007.

Sales of new homes displayed much better performance in April, rising 11% from March, far above the consensus forecast. New home sales were 3% higher than a year ago. The median new-home price of $407,200 was down 2% from last year at this time. The supply of new homes remains near the highest level since 2007.

The latest home building data was in line with expectations. Overall housing starts in April rose 2% from March, while single-family starts sank 2% to the lowest level since July 2024. Single-family building permits, a leading indicator of future construction, dropped 5% from March. A separate survey of home builder sentiment on housing market conditions from the NAHB unexpectedly plunged to the lowest level in 18 months. Builders reported that uncertainty about tariffs and rising costs made it difficult to price their homes.

Next Week

Investors will continue to look for additional information about tariff policies. For economic reports, Consumer Confidence and Durable Orders will come out on Tuesday. Personal Income and the PCE price index, the inflation indicator favored by the Fed, will be released on Friday. Mortgage markets will be closed on Monday for Memorial Day.

Until next week….

*** Please note that Freddie Mac publishes their weekly rate report on Wednesday mornings from data received Monday and Tuesday.

The graph above is intended to shown rate trends, and not “today’s current rate”. ***

Reviews From Our Past Clients

With every client, we promise to provide you with a comprehensive analysis of your mortgage needs, the best service possible, and the best rates we can find. We make it our mission to have every transaction close with our clients happy with the service we provided. Browse through the hundreds of reviews we’ve received from our clients posted on both Google and Zillow.com, and read what they thought of their experience using Hawaii Mortgage Company.

Google Link:

Hawaii Mortgage Company Review on Google.com

Zillow.com Link:

Hawaii Mortgage Company Reviews on Zillow.com

Our Rate Quote System is Available to You

Our automated rate quoting system is live. Now you can check rates and try different scenarios 24-hours a day. Remember, it’s just a computer. For non-standard rate quotes, such as construction, vacant land, and other specialty programs, you’ll still need to give a call.

Here’s the link: https://www.hawaiimortgage.net/todays-rates/

Do you think all lenders are the same?

There is a difference when you use Hawaii Mortgage Company for your financing. Here’s a short video telling you why:

Broker vs. Banker?

Click the link below to get a quick lesson on why working with a Mortgage Broker will benefit you on your next transaction.