Compliments of

Alan Van Zee

Alan Van Zee

President | NMLS #: 297154

Hawaii Mortgage Company, Inc.

Company NMLS #: 232582

Alan Van Zee is one of the top producing Mortgage Originators in the state, originating over $2,000,000,000 to date. He has written and published this weekly newsletter for the past 17 years. It is the most widely read mortgage, real estate, and finance publication in Hawaii.

Hawaii Mortgage Company, now in our 25th year of providing mortgages to the people of Hawaii, is proud to have a complaint-free history. We make sure our clients are happy!

Mortgage Market News and Insight

For the Weekend of July 12th, 2025

Hawaii’s Most Read Mortgage, Real Estate, and Finance Publication for 17 Years

Volume 17 – Issue 42

Builder Beware

As the cost of real estate continues to rise, I have received significantly more inquiries about buying vacant land and construction than at any other time in my almost 30 years of mortgage financing. The preconception is there’s a premium placed on homes already constructed. Plus, building your own place could not only save you money, but you’d enjoy a home built to your specific needs and wants.

Those were the thoughts Jerry and Alicia had when they came to me nearly two years ago. They had just purchased a lot on the Big Island and wanted to get financing for an innovative bamboo kit home manufactured overseas and shipped to Hawaii for a local contractor to assemble. The kits were reasonably priced, even with shipping, but soon they found issues that took them in a different direction. Needing financing to cover the cost of construction, lenders were not too receptive of a foreign-produced bamboo home. The big issue had to do with bonding. A completion bond is a policy the lenders require to be in place in case the contractor fails to complete your project. The bonding company will then jump in and finish your project. It’s the only way the lenders are assured your home will get finished. None of the bonding companies on any of the lenders’ approved lists were willing to issue a bond.

Those were the thoughts Jerry and Alicia had when they came to me nearly two years ago. They had just purchased a lot on the Big Island and wanted to get financing for an innovative bamboo kit home manufactured overseas and shipped to Hawaii for a local contractor to assemble. The kits were reasonably priced, even with shipping, but soon they found issues that took them in a different direction. Needing financing to cover the cost of construction, lenders were not too receptive of a foreign-produced bamboo home. The big issue had to do with bonding. A completion bond is a policy the lenders require to be in place in case the contractor fails to complete your project. The bonding company will then jump in and finish your project. It’s the only way the lenders are assured your home will get finished. None of the bonding companies on any of the lenders’ approved lists were willing to issue a bond.

Jerry and Alicia switched gears and decided to hire a local architect to design a small home that met their needs. As we are all aware nowadays, the permitting process takes forever. Once the plans were approved, Jerry and Alicia found a contractor they liked and were eager to start building. Everyone in the transaction was great to work with. Unfortunately, because of the snail’s pace in the permitting process, it was now 18 months since my first phone call with my clients. We received the signed construction contract along with Jerry and Alicia’s updated income and asset documentation. We had everything for a smooth lending portion of the process.

Jerry and Alicia have great credit and more than sufficient income. We preapproved them for their mortgage loan long before they ever engaged the architect. The one variable we could not anticipate was the astronomical rise in costs for building in relation to the market value of homes in the area they wanted to build in. Jerry and Alica paid cash for their lot in 2023. But when the contract came back to build, the total project costs exceeded what other comparable homes in the area were selling for – new. The total cost for land and building came to $650,000. Newly built homes in the area are selling in the low to mid $500,000 range.

Why would anyone want to venture into a stressful proposition to end up losing $100,000 or more at the end? That’s what Jerry and Alicia faced. With their income and resources, they could easily complete the project, but it would be a money loser from the get-go. Who in their right mind would do that?

I told Jerry what I thought. My advice was to sell the lot that already had a survey done along with the plans and permit. Together, this would be attractive to a buyer who would most likely have family and friends help build versus the cost of having a licensed general contractor complete the home. Selling the lot, plans, and permit would allow Jerry and Alicia to decouple themselves from this property and focus on their ultimate goal – owning a home in Hawaii. Plus, buying something already constructed, brand new, and ready for occupancy, will end up saving them over $100,000 in the process.

I cannot convey how difficult a conversation I had with Jerry and Alicia when that appraisal came back with the comps basically blowing up their dream. But after pondering the circumstances a little, I conveyed some very positive news. I believe it would have been far worse to proceed with building this home and not knowing until completion that the home’s market value was less than what they spent to acquire and build it. In fact, knowing what they know now, they will not only be able to get into a new home months ahead of their current timetable, but in the end, save 6-figures. To me, that’s really good news.

Learn from Jerry and Alicia. If you think building from scratch is your ticket to economical housing in Hawaii, think again. With the astronomical prices of labor and materials, building may end up costing you more. Do your research. See what homes are going for where you want to build. Make some calls to contractors and see what they are charging on a price per square foot basis. Do the math and see which way you’ll come out better. The answer will be different depending on location and the size of the home you wish to build. Your research may shock you.

Digital Credit Cards

A few weeks ago, I wrote about visiting the Costco gas station on empty only to find I had left my wallet at home. If not for the kindness of others that paid for my gas and allowed me to Venmo them the funds, I’m not sure what I would have done. I received some great responses from you, with many suggesting I get out of the 80’s and start using a digital version of my credit cards.

For those that don’t know, a digital version of your credit card lives on your smartphone. You have three choices: Apple Pay, Google Pay, or Samsung Wallet. Each works the same. You enter your credit cards into one of the 3 apps, register them with your credit card company, and you’re set to go. Your phone now substitutes for any merchant or vender that allows you to “tap to pay”. When you want to pay for something you simply open the app, put in a secret code for security reasons, and then “tap” with your phone.

For those that don’t know, a digital version of your credit card lives on your smartphone. You have three choices: Apple Pay, Google Pay, or Samsung Wallet. Each works the same. You enter your credit cards into one of the 3 apps, register them with your credit card company, and you’re set to go. Your phone now substitutes for any merchant or vender that allows you to “tap to pay”. When you want to pay for something you simply open the app, put in a secret code for security reasons, and then “tap” with your phone.

Other than being freed from carrying a wallet, there’s one additional benefit of going digital- ease of replacement. Read on of my stupidity. I’m really embarrassed by this one.

Last week I took my son to LA for training and got a chance to go to a Dodgers game. We bought tickets through StubHub but learned that to enter the stadium we needed to install the MLB Ballpark app on my phone and transfer the tickets to it. Still half asleep, I didn’t notice that I selected a bogus website to download the app from. It all looked legitimate. I should have stopped when the website asked for a credit card. I should have really stopped when the site said there was something wrong with my card and I should use another card. I stopped when that second card “didn’t work” either.

Knowing I had just entered two credit cards into a bogus website, I immediately used the number on the back of each card to get the cards cancelled. Each said the current card was shut off and a replacement would be sent in the mail. Now I was stuck not having the two cards I used the most out of commission until after I got home.

To my surprise, within a few minutes I received a notification on my phone that the two cards stored in my digital wallet had been updated and were ready to be used. Wow!

There’s another type of digital credit card that many of the big companies offer. It is called a virtual card, and it is used to make online purchases. I never utilized this service because I’ve never had my credit card compromised through an online purchase. But when my two credit cards were cancelled, it also impacted almost a dozen merchants that utilized those cards for automatic monthly charges. I pay many bills with automatic payments onto a credit card to gain miles or rewards, then pay the balance off each month.

When I got back to Hawaii, I painstakingly had to update every merchant with a new card number. But this time I set up a virtual card for each merchant. Why? The credit card companies allow you to create an unlimited number of virtual cards. Each has a unique number and security code. Now, if I ever lose my card again, it will not affect any of the virtual cards. Also, if a virtual card number is ever compromised, it can be shut off immediately – without affecting any other transaction.

Here's my advice to you. Step into the 21st century. Utilize a digital credit card and store it in your phone. Second, set up virtual cards for all your online purchases. The process is super ease and will allow for maximum protection against fraud. Yes, even you in the 70+ crowd can accomplish this.

And now the week’s economic news…….

Quiet Week

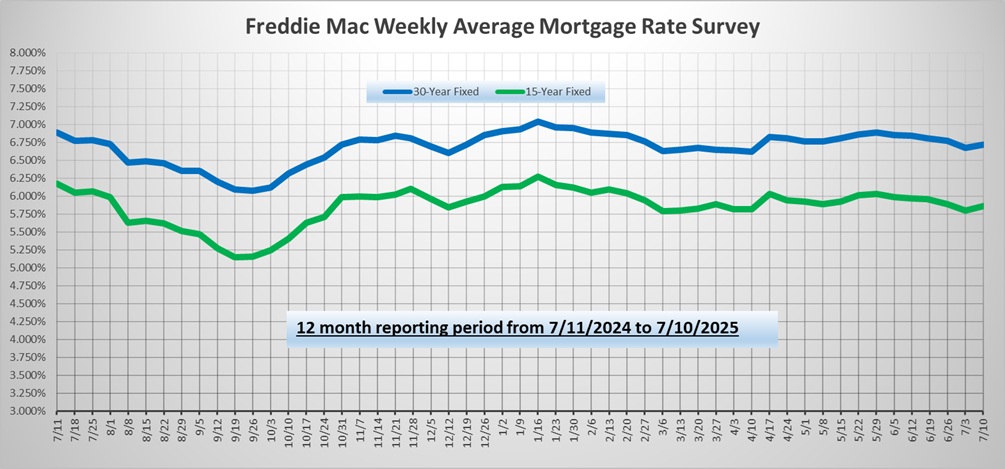

During an extremely light week for economic data, mortgage markets were relatively quiet. Comments from Fed officials and news about tariffs caused little reaction. Mortgage rates ended the week slightly higher.

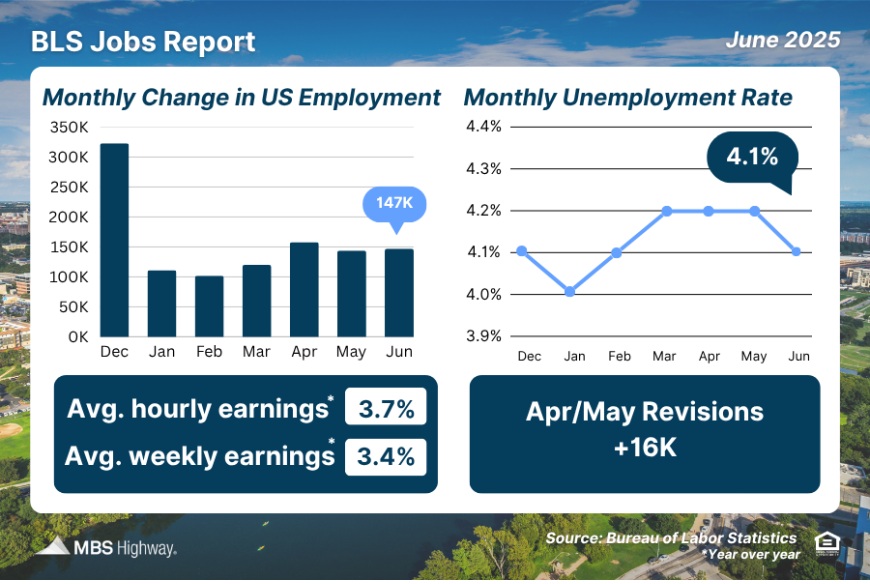

The Department of Labor releases the total number of new claims for unemployment insurance each week. The latest reading was 227,000, down from 233,000 last week and slightly lower than the consensus forecast. Bigger picture, this was far below the inflated figures seen during the early months of the pandemic, and in line with the levels which were typical during 2019. Weekly jobless claims are important because they are one of the timeliest indicators of labor market trends.

The Department of Labor releases the total number of new claims for unemployment insurance each week. The latest reading was 227,000, down from 233,000 last week and slightly lower than the consensus forecast. Bigger picture, this was far below the inflated figures seen during the early months of the pandemic, and in line with the levels which were typical during 2019. Weekly jobless claims are important because they are one of the timeliest indicators of labor market trends.

While the headline figure for jobless claims was consistent with a solid labor market experiencing relatively few layoffs, another major component of the report was a bit more troubling. The reading for continuing jobless claims, which measures the total number of people collecting unemployment insurance each week, rose to the highest level since November 2021. This suggests that it is difficult for people who are out of work to find jobs. In other words, it appears that companies continue to be reluctant to lay off their current employees, but they are slowing their pace of hiring new workers.

The detailed minutes from the June 18 Fed meeting revealed diverging opinions among officials about the outlook for future monetary policy. They generally were in agreement that it likely would be appropriate to reduce the federal funds rate later in the year, but the anticipated timing and magnitude of the cuts varied widely. Officials were split about balancing potential increases in inflation due to tariffs and signs of weakness in the labor market. Most investors currently expect that the next Fed rate cut will take place in September.

Next Week

Investors will continue to look for additional information about tariff policies and monitor comments from Fed officials. For economic reports, the Consumer Price Index (CPI), a widely followed monthly inflation indicator that looks at the price changes for a broad range of goods and services, will come out on Tuesday. The Producer Price Index (PPI), another monthly inflation indicator, will be released on Wednesday. Retail Sales and Import Prices will be released on Thursday. Since consumer spending accounts for over two-thirds of U.S. economic activity, the retail sales data is a key measure of the health of the economy. Housing Starts will come out on Friday.

Until next week….

*** Please note that Freddie Mac publishes their weekly rate report on Wednesday mornings from data received Monday and Tuesday.

The graph above is intended to shown rate trends, and not “today’s current rate”. ***

Reviews From Our Past Clients

With every client, we promise to provide you with a comprehensive analysis of your mortgage needs, the best service possible, and the best rates we can find. We make it our mission to have every transaction close with our clients happy with the service we provided. Browse through the hundreds of reviews we’ve received from our clients posted on both Google and Zillow.com, and read what they thought of their experience using Hawaii Mortgage Company.

Google Link:

Hawaii Mortgage Company Review on Google.com

Zillow.com Link:

Hawaii Mortgage Company Reviews on Zillow.com

Our Rate Quote System is Available to You

Our automated rate quoting system is live. Now you can check rates and try different scenarios 24-hours a day. Remember, it’s just a computer. For non-standard rate quotes, such as construction, vacant land, and other specialty programs, you’ll still need to give a call.

Here’s the link: https://www.hawaiimortgage.net/todays-rates/

Do you think all lenders are the same?

There is a difference when you use Hawaii Mortgage Company for your financing. Here’s a short video telling you why:

Broker vs. Banker?

Click the link below to get a quick lesson on why working with a Mortgage Broker will benefit you on your next transaction.