Compliments of

Alan Van Zee

Alan Van Zee

President | NMLS #: 297154

Hawaii Mortgage Company, Inc.

Company NMLS #: 232582

Alan Van Zee is one of the top producing Mortgage Originators in the state, originating over $2,000,000,000 to date. He has written and published this weekly newsletter for the past 18 years. It is the most widely read mortgage, real estate, and finance publication in Hawaii.

Hawaii Mortgage Company, now in our 26th year of providing mortgages to the people of Hawaii, is proud to have a complaint-free history. We make sure our clients are happy!

News and Insight

For the Weekend of February 14th, 2026

Hawaii’s Most Read Mortgage, Real Estate, and Finance Publication for 18 Years

Volume 18 – Issue 21

A Strategy to Share with You

A great real estate agent on the Big Island referred her client to me. Doris is selling her Kona home she lives in with her two siblings and needed to get pre-approved for mortgage financing to buy another home. I spent over an hour on the phone with Doris to learn her story and how to best address her needs.

First off, Doris and her siblings inherited their current home when their parents passed. I told her how unusual it is to find three grown siblings all living together. Usually, when parents leave the family home to the kids, only one remains in the home – the one taking care of mom and dad until they pass. Then the fighting starts and the home is eventually sold with the proceeds split. But in Doris’ case not only are the three of them living together in the family home, when sold, all three will continue to live together in the new home.

Here’s the financial obstacle I needed to overcome. Doris is a few years away from retirement, and her siblings already are. Doris’ biggest concern was obtaining a new mortgage knowing she would retire and see a major reduction in income. Her initial solution was to take the equity from the sale of the family home and try and find something smaller and less expensive. Her thought was to eliminate the mortgage all together. Sadly, there was nothing in that price range that worked well for three retirees.

I proposed a two-pronged solution for Doris. While Doris continues to work, she is comfortable having a mortgage payment equal to the one she has right now, about $2,000 per month. She qualifies for the mortgage that, combined with the equity from the sale of the family home, will allow her to find that “final” home for her and her siblings. When Doris is ready to retire, she’ll be able to convert her 30-Year mortgage into a reverse mortgage. With the reverse mortgage Doris will have the ability to make payments or not. As her reverse mortgage balance increases, the equity in her home will also increase. That will protect her heirs from dwindling equity.

If you are in your 50’s like Doris, you can utilize this strategy to upgrade to a nicer home and not have to worry about the mortgage payment when you retire. It is important to check with a reverse mortgage specialist first to determine your maximum loan which is based on your age and equity in the property.

Did you know you can also purchase a home using a reverse mortgage? Doris was too young, but if you are 55 or older, a reverse purchase mortgage could be a great option.

And now the week’s economic news…….

Tons of Data

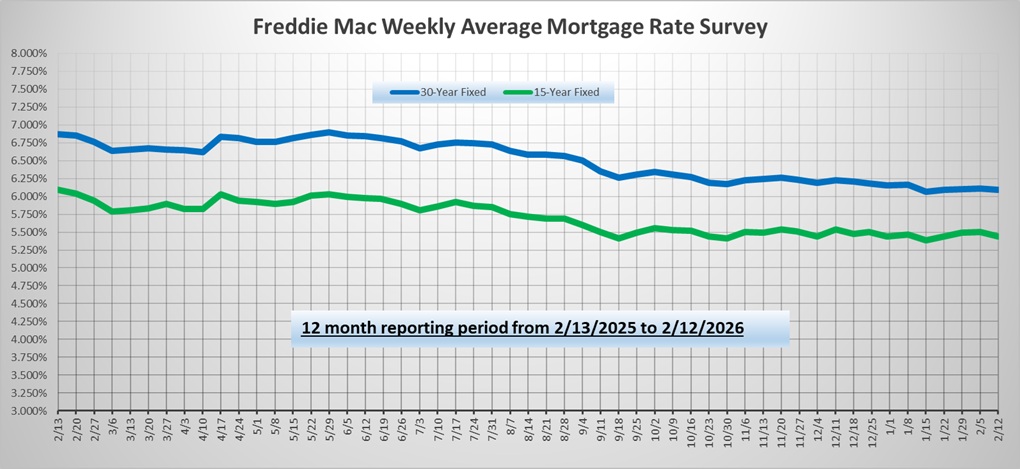

In a week packed with major economic data, weaker than expected inflation and consumer spending data outweighed strong job gains. As a result, mortgage rates ended the week lower.

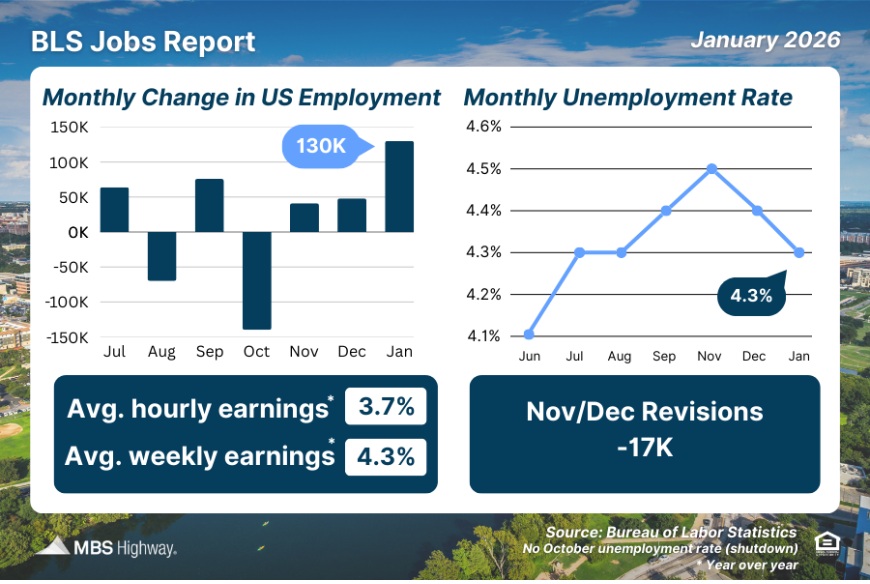

The key Employment report revealed that the economy added 130,000 jobs in January, well above the consensus forecast of 70,000 and the most since April. The unemployment rate unexpectedly fell from 4.4% to 4.3%, the lowest level since August. Average hourly earnings, an indicator of wage growth, were 3.7% higher than a year ago, down from an annual rate of 3.8% last month. This report does not sync up with any of the other reports: ADP showed the private sector at only 22,000 new jobs, while Revelio showed -13,300. The difference between the BLS and the others is that BLS reports Government jobs - which had job losses.

The key Employment report revealed that the economy added 130,000 jobs in January, well above the consensus forecast of 70,000 and the most since April. The unemployment rate unexpectedly fell from 4.4% to 4.3%, the lowest level since August. Average hourly earnings, an indicator of wage growth, were 3.7% higher than a year ago, down from an annual rate of 3.8% last month. This report does not sync up with any of the other reports: ADP showed the private sector at only 22,000 new jobs, while Revelio showed -13,300. The difference between the BLS and the others is that BLS reports Government jobs - which had job losses.

Another reason I believe the BLS figures are not accurate is the BLS’ track record. Look at what they did to their 2025 numbers: The BLS revised the 2025 numbers showing that job growth was revised lower in the full year by 403,000 to only 181,000 job gains. That means they are now saying that on average, we only saw 15,000 jobs created per month last year. Now they claim 130,000 for just January 2026 alone?

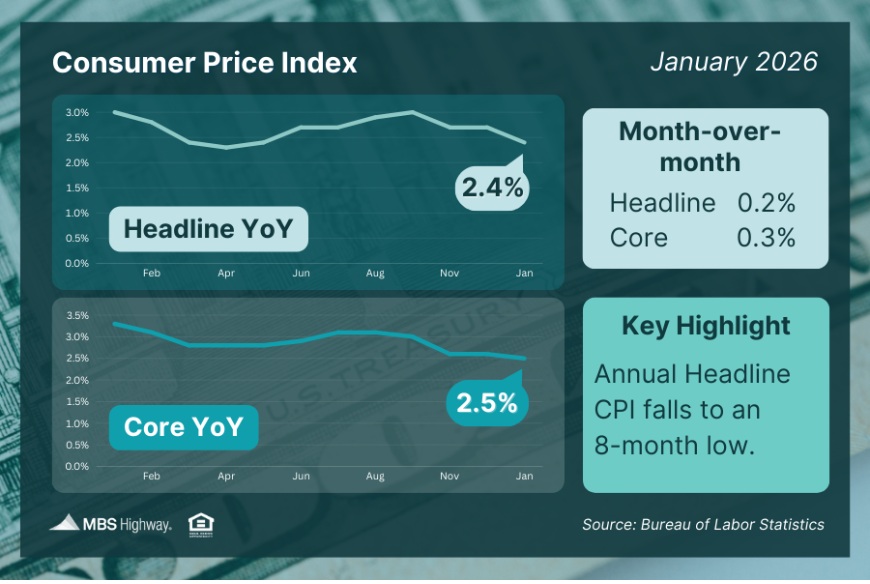

The Consumer Price Index for January showed that headline inflation came in at 0.2% (0.17% exactly). This was cooler than estimates and when annualizing the figure, it is exactly at 2%. Year over year, inflation fell from 2.7% to 2.4%, which is a very nice drop and beneath estimates of 2.5%. The most important core reading, which strips out food and energy prices, rose 0.3% in January. This was in line with estimates. and would have been 0.2% if not for a 6.5% rise in airline fares. The rise may be from a lot of travel with the frigid temperatures being experienced in some of the country, especially the Northeast. Year over year, core inflation declined from 2.6% to 2.5%, which the Bond market liked. The main reason for the decline was well-behaved shelter readings. Shelter rose 0.2% in the month, with Rent and Owners’ Equivalent Rent also rising by 0.2%. Lodging away from home, which measures things like hotels and Airbnb’s, was flat. Shelter fell from 3.2% to 3% year over year, which is a nice deceleration, but still overstating inflation. Real shelter costs are going up around 1% when looking at new and renewal rents, which means that shelter is still overheating core inflation by at least 0.5%. Without it, core inflation would be at the Fed’s target or below. There were not many signs of tariff inflation within this report, which means a lot of the pass-through may be behind us.

The Consumer Price Index for January showed that headline inflation came in at 0.2% (0.17% exactly). This was cooler than estimates and when annualizing the figure, it is exactly at 2%. Year over year, inflation fell from 2.7% to 2.4%, which is a very nice drop and beneath estimates of 2.5%. The most important core reading, which strips out food and energy prices, rose 0.3% in January. This was in line with estimates. and would have been 0.2% if not for a 6.5% rise in airline fares. The rise may be from a lot of travel with the frigid temperatures being experienced in some of the country, especially the Northeast. Year over year, core inflation declined from 2.6% to 2.5%, which the Bond market liked. The main reason for the decline was well-behaved shelter readings. Shelter rose 0.2% in the month, with Rent and Owners’ Equivalent Rent also rising by 0.2%. Lodging away from home, which measures things like hotels and Airbnb’s, was flat. Shelter fell from 3.2% to 3% year over year, which is a nice deceleration, but still overstating inflation. Real shelter costs are going up around 1% when looking at new and renewal rents, which means that shelter is still overheating core inflation by at least 0.5%. Without it, core inflation would be at the Fed’s target or below. There were not many signs of tariff inflation within this report, which means a lot of the pass-through may be behind us.

Consumer spending accounts for over two-thirds of U.S. economic activity, so the monthly Retail Sales report is a key measure of the health of the economy. Delayed by the government shutdown, the most recent data revealed that retail sales in December were flat from November, far below the consensus forecast for an increase of 0.3%. Significant declines were seen in furniture, appliances, and apparel. Due to severe winter weather in January, the results are anticipated to be weak again next month.

The latest report on home sales was disappointing. In January, sales of existing homes declined 8% from December, far below expectations, to the lowest level since December 2023. The median price of $396,800 was up a slim 0.9% from last year at this time but at a record high for the month of January. Inventories remain stuck at low levels, standing at just a 3.7-month supply nationally. However, inventories were 3% higher than a year ago.

Next Week

Looking ahead, investors will continue to monitor comments from Fed officials for hints about future monetary policy. For economic reports, Friday will be the big day. Fourth quarter GDP, Personal Income, and the PCE price index, the inflation indicator favored by the Fed, will be released on Friday. Gross Domestic Product (GDP) is the broadest measure of economic activity. Mortgage markets will be closed on Monday for Presidents Day.

Until next week….

*** Please note that Freddie Mac publishes their weekly rate report on Wednesday mornings from data received Monday and Tuesday.

The graph above is intended to shown rate trends, and not “today’s current rate”. ***

Reviews From Our Past Clients

With every client, we promise to provide you with a comprehensive analysis of your mortgage needs, the best service possible, and the best rates we can find. We make it our mission to have every transaction close with our clients happy with the service we provided. Browse through the hundreds of reviews we’ve received from our clients posted on both Google and Zillow.com, and read what they thought of their experience using Hawaii Mortgage Company.

Google Link:

Hawaii Mortgage Company Review on Google.com

Zillow.com Link:

Hawaii Mortgage Company Reviews on Zillow.com

Our Rate Quote System is Available to You

Our automated rate quoting system is live. Now you can check rates and try different scenarios 24-hours a day. Remember, it’s just a computer. For non-standard rate quotes, such as construction, vacant land, and other specialty programs, you’ll still need to give a call.

Here’s the link: https://www.hawaiimortgage.net/todays-rates/

Do you think all lenders are the same?

There is a difference when you use Hawaii Mortgage Company for your financing. Here’s a short video telling you why:

Broker vs. Banker?

Click the link below to get a quick lesson on why working with a Mortgage Broker will benefit you on your next transaction.