Compliments of

Alan Van Zee

Alan Van Zee

President | NMLS #: 297154

Hawaii Mortgage Company, Inc.

Company NMLS #: 232582

Alan Van Zee is one of the top producing Mortgage Originators in the state, originating over $2,000,000,000 to date. He has written and published this weekly newsletter for the past 18 years. It is the most widely read mortgage, real estate, and finance publication in Hawaii.

Hawaii Mortgage Company, now in our 26th year of providing mortgages to the people of Hawaii, is proud to have a complaint-free history. We make sure our clients are happy!

News and Insight

For the Weekend of April 18th, 2026

Hawaii’s Most Read Mortgage, Real Estate, and Finance Publication for 18 Years

Volume 18 – Issue 29

A Sharp Guy Who Got Confused

I am happy to be a source of knowledge for my clients and newsletter subscribers. Over the years I’ve been a guest lecturer at the UH, an expert witness in civil proceedings, and helped state regulators write the questions for the State’s Mortgage Originator license test. But I am always happy when a long-time reader takes the time to reach out with a concern of theirs.

The emails always start off this way “Alan, I don’t know how I started getting your newsletter, but I’ve been reading it for years. You seem to know what you’re talking about, so maybe you can help me…”

Leonard, who’s 87, wrote to me last week concerning title theft. He owns a mortgage-free home worth $2-million and is worried after seeing the ads on TV that some thief could take his home from him. His suspicions grew stronger when he received a telemarketing call from a company in Florida trying to sell him a program to protect his home from title theft. The person on the phone told him of a recent mortgage that was placed on his home from a local bank here in Hawaii. This news nearly killed Leonard. He had no mortgage debt. He even called the bank in question and asked them about the claim. They assured Leonard that they didn’t place any mortgage lien on his property.

Leonard, who’s 87, wrote to me last week concerning title theft. He owns a mortgage-free home worth $2-million and is worried after seeing the ads on TV that some thief could take his home from him. His suspicions grew stronger when he received a telemarketing call from a company in Florida trying to sell him a program to protect his home from title theft. The person on the phone told him of a recent mortgage that was placed on his home from a local bank here in Hawaii. This news nearly killed Leonard. He had no mortgage debt. He even called the bank in question and asked them about the claim. They assured Leonard that they didn’t place any mortgage lien on his property.

That’s when Leonard reached out to me.

My first step was to access the state’s Bureau of Conveyances to check out Leonard’s home and determine if a lien was really recorded. To my surprise, a local bank had recorded a mortgage against his home. I was able to retrieve the document and examine it. If the document were fraudulent, I am sure the local bank would do all they could to help get the lien removed from Leonard’s home. The document did look legitimate and was notarized by a local notary.

I presented my findings to Leonard. That’s when he had his “oops I forgot moment”. It turns out that a couple of months ago Leonard needed some working capital for a big government job he was awarded. Hey, he’s 87! Leonard is a sharp guy and did not remember at first signing the paperwork I provided him. What I can’t understand is who at his bank told him they didn’t place the lien.

The good news is that Leonard was not the victim of title theft. His story is a good reminder that title fraud is real, and unscrupulous people are out there looking for all kinds of creative ways to steal from you. The more paperwork a thief must navigate to perpetuate their crime, the more likely they’ll move onto an easier mark. Hold your property in trust. Try not to have the property free & clear with $$$ in equity.

The systems we have in place to record legal documents on property were never designed to prevent fraud. Yes, fraud can be reversed, but it takes time and money. Our parents used to say, “An ounce of prevention is worth a pound of cure.” That saying still rings true today.

American Paradise Lost

Chris Arnell is an independent writer who is trying to make a living by writing articles on Substack. If you are unfamiliar with Substack, it is a platform where writers can write, and people interested in what the writer has to say can subscribe for a fee. While all writers hope to get paid subscriptions, many Like Arnell offer a free subscription.

Arnell recently wrote a two-part piece about the downfall of American society. Ironically, what Arnell details is exactly why we are now plagued by situations like title fraud that I wrote about above. I want to share just a small portion of his work, as I hope you’ll be interested enough to read the entire piece and hopefully subscribe.

Something feels different in America, and most people know it long before they try to put it into words.

They notice it in ordinary places. On the road. In stores. In neighborhoods that used to feel predictable. In the way strangers speak to each other, or avoid speaking at all. There is less ease in daily life than there used to be. Less assumption of goodwill. Less confidence that the person standing in front of you was raised with anything close to the same understanding of how to behave.

For years, Americans have been told not to trust that judgment. They have been told that what they are seeing is simply change. The country is evolving. It is becoming more modern, more open, more diverse. Some of that is true. No society stays the same. But change, by itself, explains very little. A country can change and still remain stable. A society can become more varied and still remain functional.

What people are reacting to is not change. It is the breakdown of a common culture that once made everyday life more workable than it is now.

There was a time in this country when many of the most important rules were never written down because they did not have to be. People understood them. You stood in line. You showed basic courtesy in public. You did your job even when you did not feel like doing it. You treated police officers, firefighters, and teachers with a level of respect because they represented order, service, and authority. You tried not to embarrass yourself in public. You tried, in general, to carry yourself like somebody had raised you to live among other people.

If any of the above starts getting the wheels in your head spinning, I encourage you to read both part 1 and part 2. They’re free to read and share. Here’s the direct link to the articles:

https://mrchrisarnell.com/p/american-paradise-lost-part-i

And now the week’s economic news…….

Home Sales Fall

Progress in reaching a deal to end the conflict in the Middle East caused oil prices to decline, which was positive for both stocks and bonds. Other than that, it was a light week for economic data, and the reports caused little reaction.

An inflation report which measures wholesale costs for producers reflected the rise in energy prices during the month. The March Producer Price Index (PPI) was 4.0% higher than a year ago, up sharply from an annual rate of 3.4% the prior month and the highest level since February 2023. Its impact was minor, however, as investors tend to place a lot more weight each month on the Consumer Price Index report, which better reflects overall inflation levels in the economy.

An inflation report which measures wholesale costs for producers reflected the rise in energy prices during the month. The March Producer Price Index (PPI) was 4.0% higher than a year ago, up sharply from an annual rate of 3.4% the prior month and the highest level since February 2023. Its impact was minor, however, as investors tend to place a lot more weight each month on the Consumer Price Index report, which better reflects overall inflation levels in the economy.

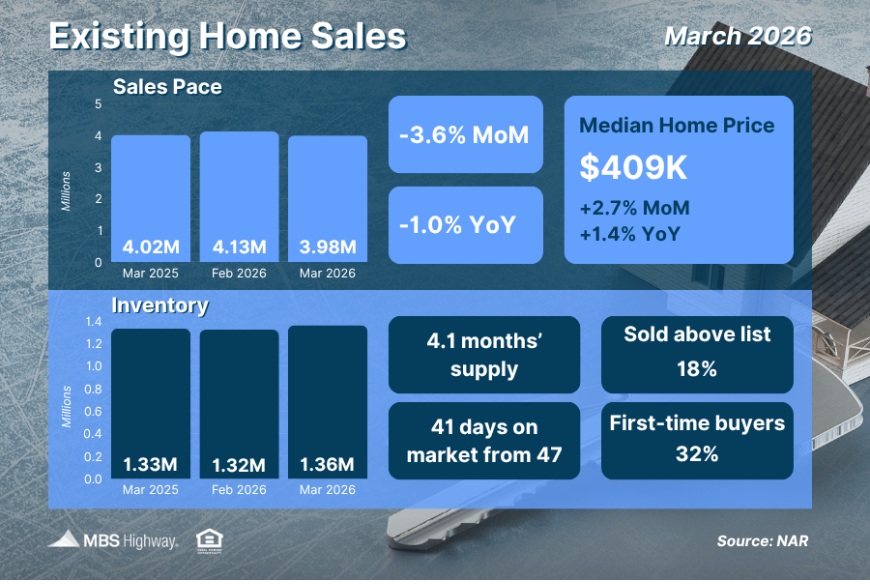

In March, sales of previously owned homes fell 4% from February, below expectations, to the lowest level since June 2025. Existing home sales were down slightly from a year ago. The median price of $408,800 was up just a slim 1% from last year at this time. Inventories remain stuck at low levels, standing at just a 4.1-month supply nationally, just below the 4.6-month supply typical in a balanced market. However, inventories were 2% higher than a year ago. Homes remain on the market for a median time of 41 days, up from 36 days last year at this time. The National Association of Realtors now expects existing home sales to increase just 4% in 2026, down from its previous forecast for an increase of 14%, and it expects new home sales to be flat this year.

In March, sales of previously owned homes fell 4% from February, below expectations, to the lowest level since June 2025. Existing home sales were down slightly from a year ago. The median price of $408,800 was up just a slim 1% from last year at this time. Inventories remain stuck at low levels, standing at just a 4.1-month supply nationally, just below the 4.6-month supply typical in a balanced market. However, inventories were 2% higher than a year ago. Homes remain on the market for a median time of 41 days, up from 36 days last year at this time. The National Association of Realtors now expects existing home sales to increase just 4% in 2026, down from its previous forecast for an increase of 14%, and it expects new home sales to be flat this year.

A survey of home builder sentiment on housing market conditions from the NAHB unexpectedly fell four points to 34, the lowest level since September 2025. It has remained in negative territory below 50 for twenty-four straight months. According to the NAHB, 60% of builders used sales incentives in April and 36% cut prices. 62% of builders reported that suppliers have increased building material costs due to higher fuel prices.

Next Week

Looking ahead, attention will remain fixed on the conflict in the Middle East. Investors also will monitor comments from Fed officials about future monetary policy. It will be a light week for economic data. The most significant report will be Retail Sales on Tuesday. Since consumer spending accounts for over two-thirds of U.S. economic activity, the retail sales data is a key measure of the health of the economy.

Until next week….

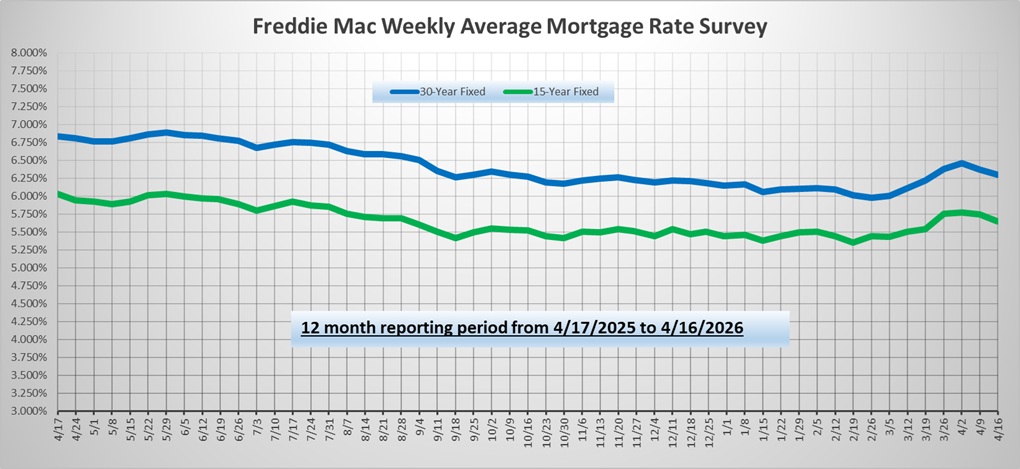

*** Please note that Freddie Mac publishes their weekly rate report on Wednesday mornings from data received Monday and Tuesday.

The graph above is intended to shown rate trends, and not “today’s current rate”. ***

Reviews From Our Past Clients

With every client, we promise to provide you with a comprehensive analysis of your mortgage needs, the best service possible, and the best rates we can find. We make it our mission to have every transaction close with our clients happy with the service we provided. Browse through the hundreds of reviews we’ve received from our clients posted on both Google and Zillow.com, and read what they thought of their experience using Hawaii Mortgage Company.

Google Link:

Hawaii Mortgage Company Review on Google.com

Zillow.com Link:

Hawaii Mortgage Company Reviews on Zillow.com

Our Rate Quote System is Available to You

Our automated rate quoting system is live. Now you can check rates and try different scenarios 24-hours a day. Remember, it’s just a computer. For non-standard rate quotes, such as construction, vacant land, and other specialty programs, you’ll still need to give a call.

Here’s the link: https://www.hawaiimortgage.net/todays-rates/

Do you think all lenders are the same?

There is a difference when you use Hawaii Mortgage Company for your financing. Here’s a short video telling you why:

Broker vs. Banker?

Click the link below to get a quick lesson on why working with a Mortgage Broker will benefit you on your next transaction.