Compliments of

Alan Van Zee

Alan Van Zee

President | NMLS #: 297154

Hawaii Mortgage Company, Inc.

Company NMLS #: 232582

Alan Van Zee is one of the top producing Mortgage Originators in the state, originating over $2,000,000,000 to date. He has written and published this weekly newsletter for the past 18 years. It is the most widely read mortgage, real estate, and finance publication in Hawaii.

Hawaii Mortgage Company, now in our 26th year of providing mortgages to the people of Hawaii, is proud to have a complaint-free history. We make sure our clients are happy!

News and Insight

For the Weekend of May 2nd, 2026

Hawaii’s Most Read Mortgage, Real Estate, and Finance Publication for 18 Years

Volume 18 – Issue 31

Who Doesn’t Like to Spend?

Spending is different than paying your bills. Spending is the joyful activity of buying things that enrich your life – be it a dinner out, some new clothes, or for those big purchases - getting that new car! Paying your bills is certainly no fun – your mortgage, those credit card bills for that dinner out, the new clothes, and that new car payment. But what if you could use someone else’s money to pay your bills? Today let’s dive into the luxury our state legislature gets to enjoy.

It’s crunch time once again at that “big square building on Beretania” (the capitol) – as Larry Price liked to call it. The big wigs in both the House and Senate are swapping formulas back and forth on how best to spend our money. They enjoy something none of us get experience – spending without using your own money. I could imagine it would be like working for a really rich family where my job was to purchase everything they needed – but using their credit card. What a joy it would be not caring about that bill coming at the end of the month.

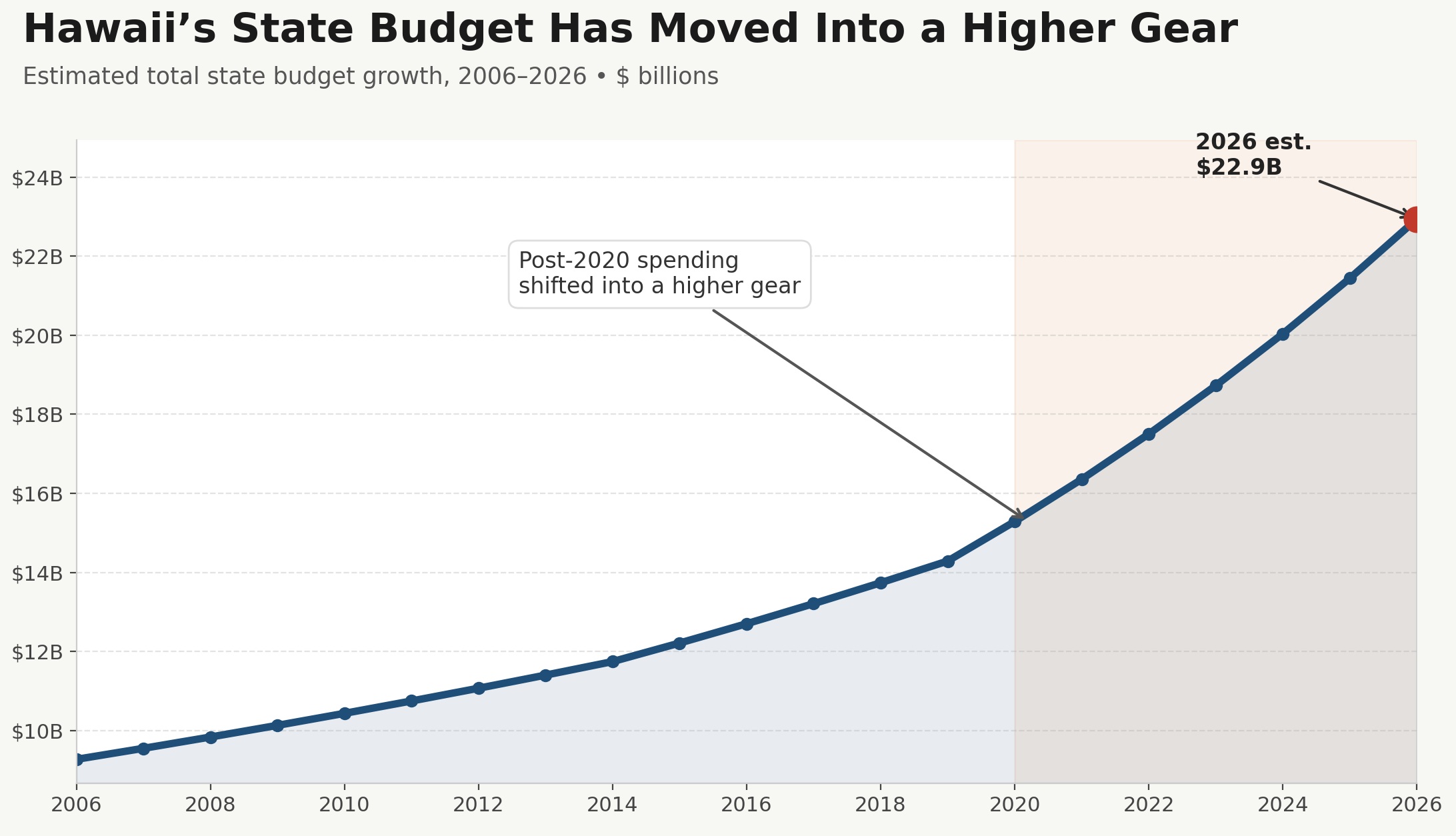

Our legislator’s jobs are kind of like that. They spend on someone else’s account and pay for it through the collection of taxes and fees they decide to impose on us. That is why our state budget looks like this:

I could use the term “they spend like drunken sailors” but for those under 50 that read my newsletter, they might scratch their head over that World War II reference. So, I’ll just point out the obvious, their spending is reckless. In 2020 when covid hit, the world faced an unprecedented global recession. Instead of being fiscally responsible, the spending by those we’ve elected has only accelerated.

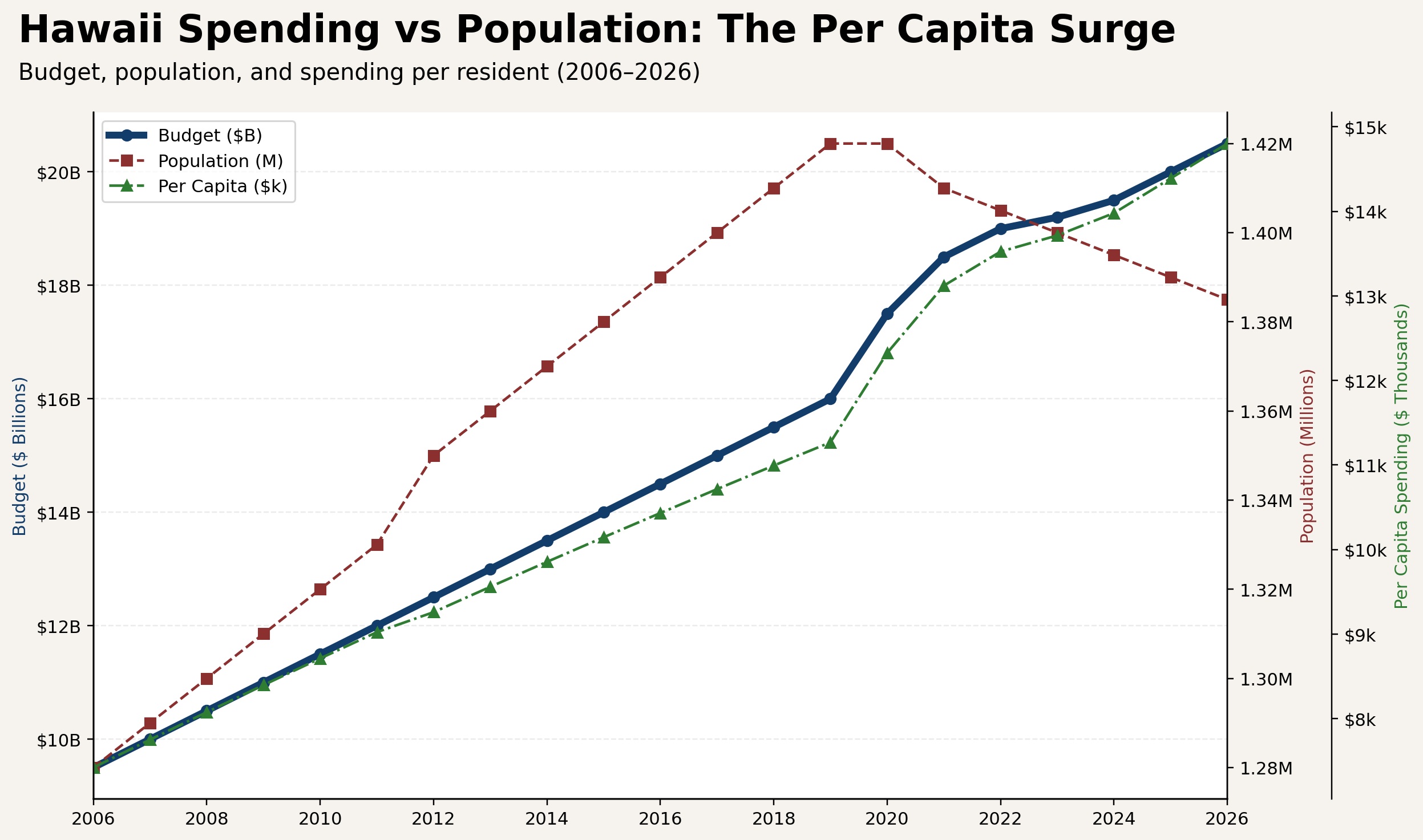

One could claim that our population has been increasing, and therefore the budget needs to increase to meet an ever-growing demand for government services. But if you look at the graph below, our population outpaced government spending until 2020 when covid struck.

I’ve also added per capita spending, the amount the government spends per resident. If the increase in our state budget was simply due to an increase in population, the per capita spending line would be flat, but that isn’t the case. In fact, our population has now been decreasing for the past 6 years, yet spending continues to climb.

What infuriates me the most is the end-around ways our state government collects more taxes yet tries to come off as heroes by saving the tax cuts we so graciously got last year. Yes, they did preserve the cuts for most, but they eliminated them for higher earners. The claim “the rich can afford it” is pitting people against each other. And that is no way to govern.

It reminds me of my early days - fresh out of school living in the back of Palolo Valley with roommates. I kept noticing that someone was poaching my food from the refrigerator. When I finally confronted the culprit, he didn’t apologize. Instead, because I was big guy and he was skinny, he said I could afford to give up some of my food for someone who could truly benefit from it.

That’s the attitude our legislators work with. Continue to spend because those better off can afford to give more. You may be okay with this theory, but who gets to set the standard as to who can afford to give more? There’s a bill currently being massaged to increase the conveyance taxes when you sell your home. First off, the conveyance tax was initially a fee added to all real estate transactions to offset the cost of running the Bureau of Conveyances. It was never designed as a source of revenue for other portions of the state budget. One current proposal is to hike the tax from 0.5% to as high as 6%. That’s a 1,100% increase! In one version there’s protections to make sure the “little people” are protected by only affecting homes greater than $2-million dollars. $2-million in Hawaii’s real estate isn’t homes for Zuckerberg, Musk, or Gates. $2-million-dollar homes in Hawaii are family homes in Manoa, long held North Shore family beachfront properties, and many others.

The point is our government is not fiscally responsible. They spend and tax. When was the last time you heard any politician in Hawaii suggest we cut government? With so many people complaining they can’t make it here and are forced to move away, why can’t those we decide to put in office try and make it easier to live here versus harder? If they can’t maybe we need to elect different people.

And now the week’s economic news…….

Steady Fed

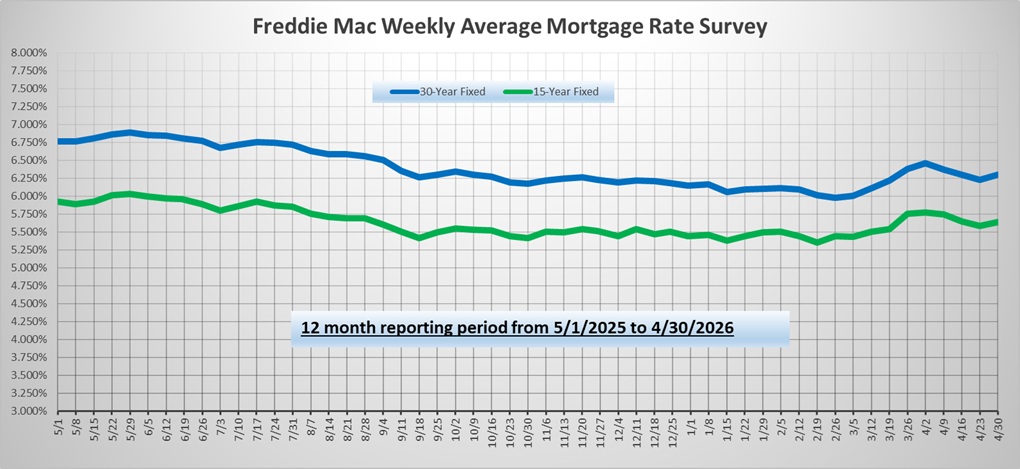

Headlines about the conflict in the Middle East continued to cause volatility for mortgage markets this week. The Fed meeting revealed no significant surprises, and the economic data caused little reaction. Mortgage rates ended the week slightly higher.

As expected, the Fed left the federal funds rate unchanged for the third straight meeting at a range of 3.50 to 3.75%. Most of the attention focused on the unexpectedly large split in the decision. Just eight officials voted in favor of holding the federal funds rate steady, while four dissented, the most since 1992. However, only one official dissented based on a preference for a rate cut. The other three wanted to remove language in the statement which continued to indicate an "easing bias," suggesting that the next policy change would be a cut rather than a hike. Several officials would prefer more neutral guidance. Similarly, investor expectations have shifted in recent months, and they no longer anticipate any reduction in the federal funds rate this year, mostly due to inflationary pressures from higher energy prices.

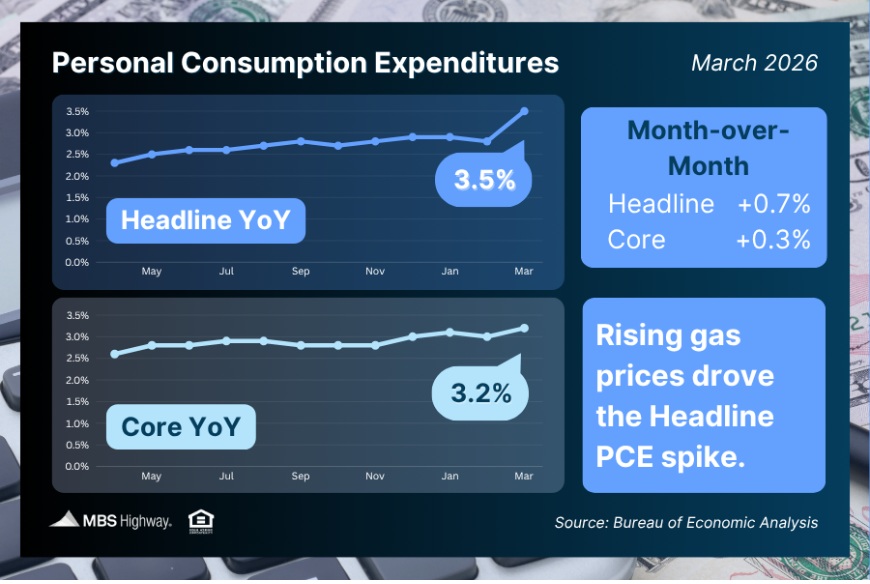

Fed officials keep a close eye on inflation, and the PCE price index is their favored indicator. Core PCE in March was 3.2% higher than a year ago, up from an annual rate of increase of 3.0% in February and the highest level since November 2023. Progress toward the 2.0% target of the Fed has not been easy, and this desired level has not been achieved since February 2021.

Fed officials keep a close eye on inflation, and the PCE price index is their favored indicator. Core PCE in March was 3.2% higher than a year ago, up from an annual rate of increase of 3.0% in February and the highest level since November 2023. Progress toward the 2.0% target of the Fed has not been easy, and this desired level has not been achieved since February 2021.

Gross Domestic Product (GDP) is the broadest measure of economic activity. During the first quarter of 2026, U.S. GDP grew at an annualized rate of 2.0%, up from just 0.5% in the fourth quarter, but a little below the consensus forecast. Strength was seen in business investment, and economists estimate that spending related to Artificial Intelligence accounted for as much as 75% of all growth during the quarter. A rebound in government spending following the shutdown during the fourth quarter also contributed to the higher reading.

The latest home building data revealed mixed results. On the positive side, housing starts in March rose 11% from February, far exceeding expectations, to the highest level since December 2024. However, building permits, a leading indicator of future construction, fell to the lowest level since March 2025.

Next Week

Looking ahead, attention will remain fixed on the conflict in the Middle East. Investors also will monitor comments from Fed officials about future monetary policy. For economic data, New Home Sales, JOLTS, and the ISM national services sector index will come out on Tuesday. The key Employment report will be released on Friday, and these figures on the number of jobs, the unemployment rate, and wage inflation are always closely watched.

Until next week….

*** Please note that Freddie Mac publishes their weekly rate report on Wednesday mornings from data received Monday and Tuesday.

The graph above is intended to shown rate trends, and not “today’s current rate”. ***

Reviews From Our Past Clients

With every client, we promise to provide you with a comprehensive analysis of your mortgage needs, the best service possible, and the best rates we can find. We make it our mission to have every transaction close with our clients happy with the service we provided. Browse through the hundreds of reviews we’ve received from our clients posted on both Google and Zillow.com, and read what they thought of their experience using Hawaii Mortgage Company.

Google Link:

Hawaii Mortgage Company Review on Google.com

Zillow.com Link:

Hawaii Mortgage Company Reviews on Zillow.com

Our Rate Quote System is Available to You

Our automated rate quoting system is live. Now you can check rates and try different scenarios 24-hours a day. Remember, it’s just a computer. For non-standard rate quotes, such as construction, vacant land, and other specialty programs, you’ll still need to give a call.

Here’s the link: https://www.hawaiimortgage.net/todays-rates/

Do you think all lenders are the same?

There is a difference when you use Hawaii Mortgage Company for your financing. Here’s a short video telling you why:

Broker vs. Banker?

Click the link below to get a quick lesson on why working with a Mortgage Broker will benefit you on your next transaction.