Compliments of

Alan Van Zee

Alan Van Zee

President | NMLS #: 297154

Hawaii Mortgage Company, Inc.

Company NMLS #: 232582

Alan Van Zee is one of the top producing Mortgage Originators in the state, originating over $2,000,000,000 to date. He has written and published this weekly newsletter for the past 18 years. It is the most widely read mortgage, real estate, and finance publication in Hawaii.

Hawaii Mortgage Company, now in our 26th year of providing mortgages to the people of Hawaii, is proud to have a complaint-free history. We make sure our clients are happy!

News and Insight

For the Weekend of May 16th, 2026

Hawaii’s Most Read Mortgage, Real Estate, and Finance Publication for 18 Years

Volume 18 – Issue 33

Yikes! Retirement is Expensive!

I read the crappy stuff, so you don’t have to. I spend a good chunk of time when not interacting with clients reading to learn how to do what I do better. Some of the stuff I read is good, while others fall short (to be kind). Other articles make good points but contain fatal flaws in how they support their theories.

One such article that was all over the internet this week came from an investment site called MoneyLion. They ranked the 50 states based on how much it costs to retire in each. To no surprise, Hawaii won (?) by being the #1 most expensive place in thew US to retire in.

| 1. Hawaii | 11. Alaska | 21. Vermont | 31. Tennessee | 41. Ohio |

| 2. California | 12. New York | 22. Delaware | 32. Texas | 42. Michigan |

| 3. Massachusetts | 13. Connecticut | 23. Florida | 33. South Carolina | 43. Iowa |

| 4. Washington | 14. Maryland | 24. Wyoming | 34. Illinois | 44. Alabama |

| 5. New Jersey | 15. Idaho | 25. Minnesota | 35. North Dakota | 45. Kentucky |

| 6. Colorado | 16. Montana | 26. North Carolina | 36. Pennsylvania | 46. Oklahoma |

| 7. New Hampshire | 17. Nevada | 27. Georgia | 37. Nebraska | 47. Arkansas |

| 8. Oregon | 18. Maine | 28. Wisconsin | 38. Missouri | 48. Louisiana |

| 9. Rhode Island | 19. Arizona | 29. South Dakota | 39. Indiana | 49. Mississippi |

| 10. Utah | 20. Virginia | 30. New Mexico | 40. Kansas | 50. West Virginia |

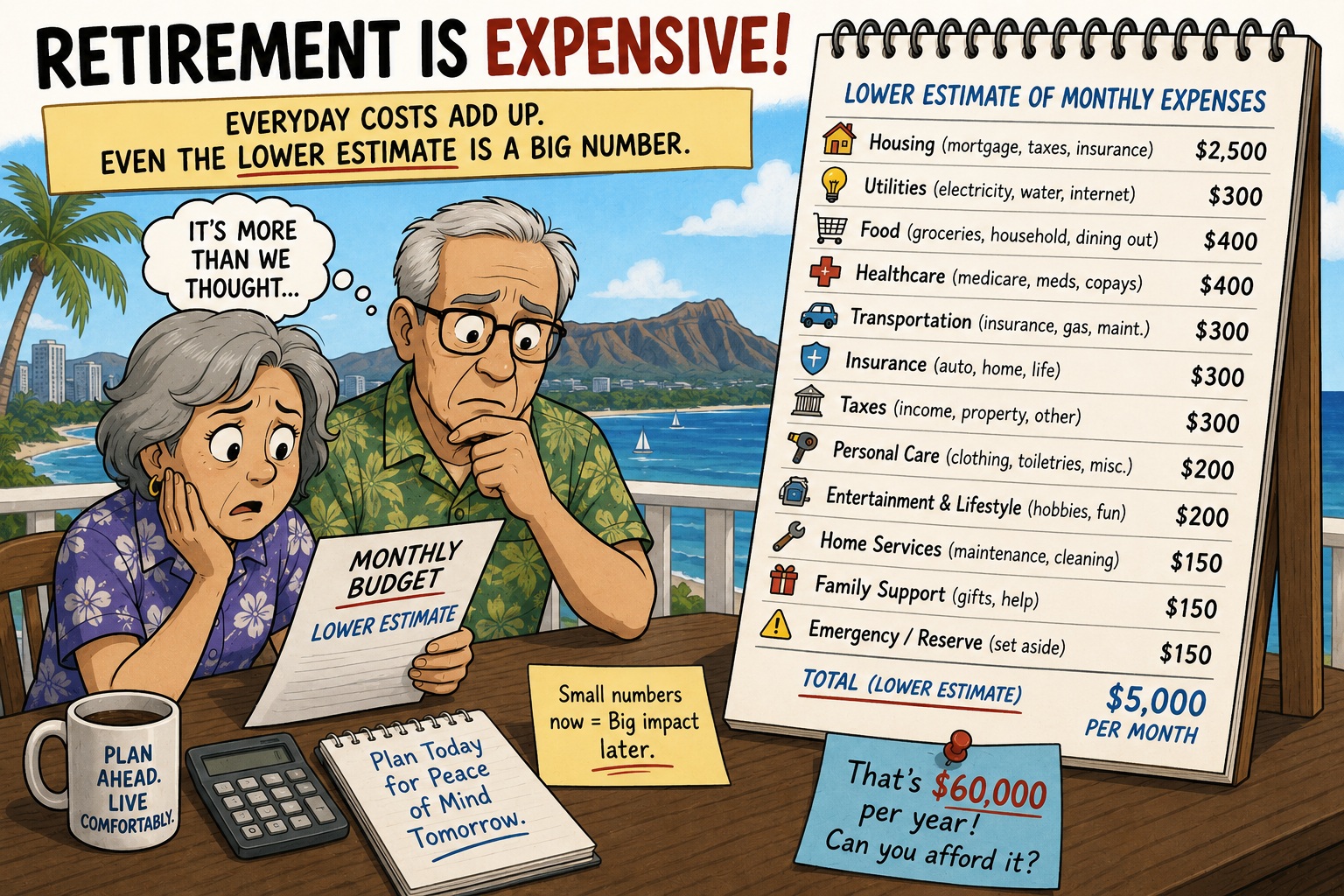

The formulas they used to determine how much money you would need to retire in each state were staggering, but flawed. But no matter the calculations this website used, it will cost you more to retire in Hawaii than any other state. That’s not a surprise to any of us, especially to the group of Hawaii retirees living in Las Vegas. I have never done the math for retirement before because I’m not ready to retire. I realize now that is foolish. I’ve always relied on working hard, saving money, and hopefully when I retire it will be enough. But after seeing that article I wondered how many of you have ever done any retirement budgeting. I thought that if I am going to suggest something for you to do, I better do it myself. Follow along. Take some notes. Don’t get discouraged at the end.

I first put together a list of common the common expenses retirees have. While many of the expenses don’t change throughout your life, there are some expenses specifically for seniors.

Category Common Monthly Expenses

Housing Mortgage or rent, property taxes, homeowners insurance, HOA/condo fees, maintenance, repairs

Utilities Electricity, water, sewer, gas, trash, internet, cell phone, cable/streaming

Food Groceries, household supplies, dining out, coffee/snacks

Healthcare Medicare premiums, Medicare supplement or Advantage plan premiums, prescription drugs, dental, vision, hearing, copays, out-of-pocket medical costs

Transportation Car payment, auto insurance, gas, maintenance, registration, parking, public transportation, rideshare

Insurance Life insurance, long-term care insurance, umbrella policy, homeowners/renters, auto

Debt Payments Credit cards, personal loans, student loans, HELOCs, medical debt

Taxes Federal/state income taxes, property taxes, taxes on Social Security, pension, IRA/401(k) withdrawals, capital gains

Personal Care Haircuts, clothing, toiletries, gym memberships, wellness services

Entertainment & Lifestyle Travel, hobbies, golf/tennis clubs, movies, events, restaurants, subscriptions

Family Support Gifts, helping children or grandchildren, education contributions, family travel

Home Services Landscaping, house cleaning, pest control, pool service, repairs, appliance replacement

Emergency/Reserve Costs Medical surprises, major home repairs, car replacement, family emergencies

Charitable Giving Church, nonprofits, community organizations, recurring donations

End-of-Life / Estate Costs Legal documents, trust updates, funeral planning, financial advisor fees

When you look at a list like this you start saying to yourself “…wow, that’s a lot of money.” Now before you dismiss the list above because you don’t foresee you having those expenses, the list can be broken down into three categories: Essential, Lifestyle, and Irregular.

Essential expenses

These are the “must-pay” items:

- Housing

- Utilities

- Food

- Healthcare

- Transportation

- Insurance

- Taxes

Lifestyle expenses

These determine comfort level:

- Travel

- Dining out

- Hobbies

- Clubs

- Entertainment

- Gifts

- Subscriptions

Irregular but predictable expenses

These are easy to forget but often create budget stress:

- Home repairs

- Car repairs or replacement

- Dental work

- Hearing aids

- Property tax increases

- Insurance premium increases

- Family help

- Major medical costs

For many retirees, the biggest wild cards are healthcare, housing, insurance, and long-term care. Food and utilities are easier to estimate. Travel and family support are more flexible, but they can quietly become large budget items.

For a Hawaii retiree, the categories that tend to bite hardest are usually housing, electricity, food, insurance, healthcare, and travel, because “quick trip to see the grandkids” often means “airfare, hotel, rental car, and suddenly this is a line item.”

Here’s an exercise I hope all of you try while reading this newsletter. Take the list above and estimate how much it will cost you for each of the categories from housing to estate expenses. I’m going to provide you with ranges of what I’ve been able to find, but no cheating! The exercise will be more educational if you plug your estimates in first.

Here’s the ranges for a typical retiree in Hawaii:

| Housing | $2,500 – $6,000+ |

| Utilities | $350 – $800 |

| Food | $800 – $1,800 |

| Healthcare | $600 – $1,800+ |

| Transportation | $500 – $1,500 |

| Insurance | $300 – $1,200+ |

| Debt Payments | $0 – $2,000+ |

| Taxes | $500 – $2,500+ |

| Personal Care | $150 – $600 |

| Entertainment & Lifestyle | $500 – $2,500+ |

If you take the minimum for each category, it’s still $6,200 per month. Sadly, the average Social Security benefit is $2,049 per month. For ease of calculations, let’s use $4,000 per month as what’s needed after any pension. If you retire at 65 and expect to live another 20 years to 85, you’ll have 240 months of $4,000 per month in expenses. That’s a staggering $960,000!

The good news is that $960,000 isn’t needed upfront. Since you’ll be drawing money while it earns a return, you can get away with much less. So how much would you need upfront at age 65 to retire on drawing $4,000 per month for 20 years? Let’s say your average rate of return on your investments is 5%. Luckily, we have computers to do that math. You’ll need $607,000 in your investment accounts. After the 240th check for $4,000 you will have $0.

For those that don’t have sufficient retirement funds saved, you’ll have to look at options you may not want to consider. Many people will be forced into generational living. Others will sell their home and move to the mainland where it is cheaper. One other option for those over 59 ½ and have equity in their home is a Reverse Mortgage. This isn’t a plug for reverse mortgages, but the reality is if you’re going to retire and don’t have the funds to retire, a reverse mortgage may be the only option if you wish to stay in your current home.

Again, no sales pitch. I just wanted to share what I found when being prompted by a poorly researched article I came across this week. Do your own research. Start with the expense list above and plug your own numbers in. Then subtract what income you’ll receive once you retire. Once you determine your monthly expense total, you can then honestly address how to live in retirement.

A Wonderful Message

You may have heard about it, but this is something you need to spend 14 minutes of your life watching. Last weekend country singer Eric Church delivered the commencement address at the University of North Carolina Chapel Hill.

Chruch’s address is one of the best messages I have ever heard on how one should live their life. While the speech was for graduates, the message holds true for everyone at any point in their life.

Take 14 minutes and have something resonate within your soul. That’s a tall order, but I think it delivers.

Here’s the link on YouTube:

https://youtu.be/pSYEDc7-Ah0?si=CoNu0hQxt9z5rrir

And now the week’s economic news…….

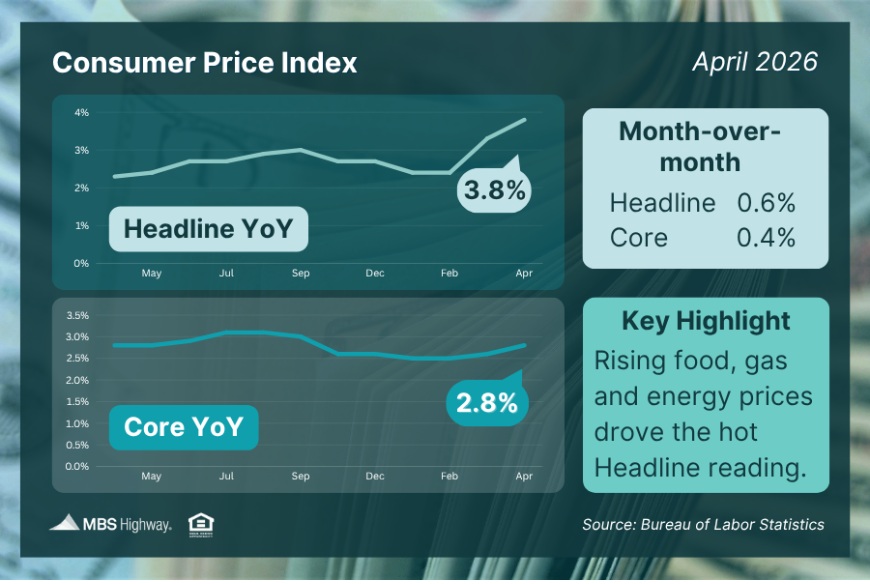

Higher Inflation

Rising oil prices were negative for mortgage markets this week, and the latest inflation reports reflected the impact of higher energy prices. As a result, mortgage rates climbed to their highest levels of the year.

The Consumer Price Index (CPI) is one of the most closely watched inflation indicators released each month, and investors were prepared for the effects of sharply higher oil prices. In April, CPI jumped 0.6% from March, matching expectations. CPI was 3.8% higher than a year ago, up substantially from an annual rate of 3.3% last month and the highest level since May 2023. Sensitive to fuel prices, airline fares were an enormous 21% higher than a year ago. Also notable, the annual increase in average hourly earnings in April was 3.6%, meaning that wage gains are no longer keeping up with the inflation rate.

The Consumer Price Index (CPI) is one of the most closely watched inflation indicators released each month, and investors were prepared for the effects of sharply higher oil prices. In April, CPI jumped 0.6% from March, matching expectations. CPI was 3.8% higher than a year ago, up substantially from an annual rate of 3.3% last month and the highest level since May 2023. Sensitive to fuel prices, airline fares were an enormous 21% higher than a year ago. Also notable, the annual increase in average hourly earnings in April was 3.6%, meaning that wage gains are no longer keeping up with the inflation rate.

To reduce short-term volatility and get a better sense of the underlying inflation trend, investors look at core CPI, which excludes food and energy. In April, Core CPI was 2.8% higher than a year ago, up from 2.6% last month and the highest level since September 2025. Shelter (housing) costs were up 3.3% on an annual basis and continue to be a primary reason why bringing inflation down to the 2% target of the Fed remains challenging.

A different inflation report released this week, which measures wholesale costs for producers, also reflected the rise in energy prices. The April Producer Price Index (PPI) rose a shocking 1.4% from March, far above the consensus forecast for an increase of 0.5% and the largest monthly gain since March 2022. PPI was 6.0% higher than a year ago, up sharply from an annual rate of 4.0% the prior month and the highest level since December 2022. Its impact was relatively minor, however, as investors tend to place a lot more weight each month on the Consumer Price Index report, which better reflects overall inflation levels in the economy.

Consumer spending accounts for over two-thirds of U.S. economic activity, so the monthly Retail Sales report is a key measure of the health of the economy. While economists had anticipated that larger than usual tax refunds would provide an extra boost again this month, they also had to factor in that the enormous rise in gas prices might drain some of that strength. The actual result was that retail sales in April rose a solid 0.5% from March, matching expectations, but a far cry from the massive increase of 1.6% last month. Strength was seen in appliances, electronics, sporting goods, and hobbies. Supported by powerful stock market gains, upper-income households continue to purchase at a rapid pace, while lower-income consumers are cutting back discretionary spending to focus on necessities.

Next Week

Looking ahead, attention will remain fixed on the conflict in the Middle East. Investors also will monitor comments from Fed officials about future monetary policy. The detailed minutes from the April 29 Fed meeting will come out on Wednesday. It will be a light week for economic data. Housing Starts will come out on Thursday.

Until next week….

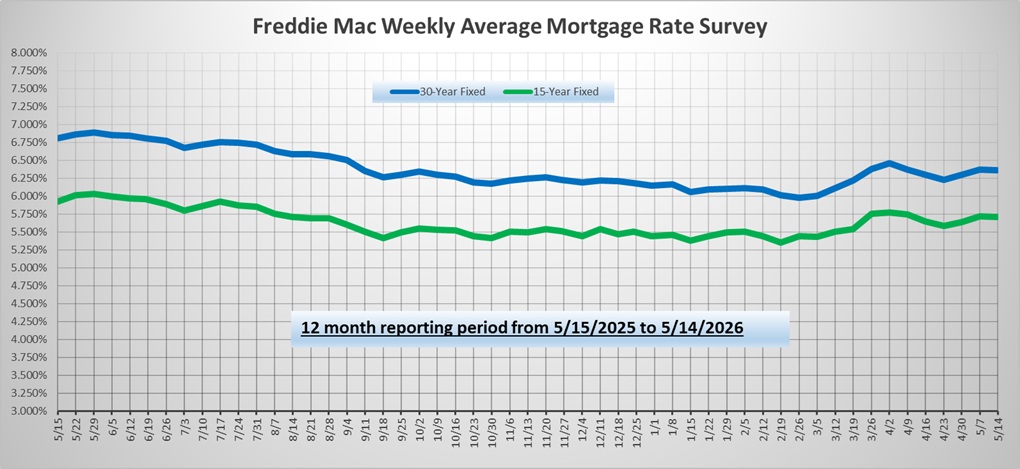

*** Please note that Freddie Mac publishes their weekly rate report on Wednesday mornings from data received Monday and Tuesday.

The graph above is intended to shown rate trends, and not “today’s current rate”. ***

Reviews From Our Past Clients

With every client, we promise to provide you with a comprehensive analysis of your mortgage needs, the best service possible, and the best rates we can find. We make it our mission to have every transaction close with our clients happy with the service we provided. Browse through the hundreds of reviews we’ve received from our clients posted on both Google and Zillow.com, and read what they thought of their experience using Hawaii Mortgage Company.

Google Link:

Hawaii Mortgage Company Review on Google.com

Zillow.com Link:

Hawaii Mortgage Company Reviews on Zillow.com

Our Rate Quote System is Available to You

Our automated rate quoting system is live. Now you can check rates and try different scenarios 24-hours a day. Remember, it’s just a computer. For non-standard rate quotes, such as construction, vacant land, and other specialty programs, you’ll still need to give a call.

Here’s the link: https://www.hawaiimortgage.net/todays-rates/

Do you think all lenders are the same?

There is a difference when you use Hawaii Mortgage Company for your financing. Here’s a short video telling you why:

Broker vs. Banker?

Click the link below to get a quick lesson on why working with a Mortgage Broker will benefit you on your next transaction.